For many Indians growing up in the 1980s, 1990s, and even early 2000s, insurance was not something you found online, compared on websites, or discussed with financial advisors.

Insurance came home.

Yes, and usually in the evening.

A familiar person would visit. Sometimes a neighbour, sometimes a distant relative, sometimes a friend of your father. They would sit in the living room, drink tea, open a brown folder, take out a few forms, and start talking about “policy”, “premium”, and “maturity”.

That’s LIC agent.

In those days, LIC was a synonym for insurance.

LIC was not a company name in people’s minds. It was basically a product itself.

It’s like how people say ‘Xerox’ instead of ‘photocopy’. LIC was that for insurance in India

Policies were not bought online. They were sold through trust. Through conversations. Through relationships. Through someone your family already knew.

One agent would sell policies to a few families in a neighbourhood. Those families would later recommend the same agent to relatives. Over time, the agent became the “insurance person”

And this network of LIC ended up making it one of the deepest and strongest distribution moats any financial institution has ever built in India.

But the story does not stop at distribution.

Over time, LIC started playing a much bigger role in the financial system itself.

When large IPOs needed a strong investor, LIC was often there. When markets were falling and foreign investors were selling, LIC was often buying. When the government wanted to sell stakes in public sector companies, LIC frequently became the anchor investor.

And when certain financial institutions got into trouble, LIC was sometimes asked to step in.

The IDBI Bank rescue in 2018 is one of the most well-known examples, where LIC bought a controlling stake when the bank was collapsing under bad loans and losses.

Situations like these slowly changed how LIC was viewed. It was no longer just an insurance company collecting premiums and paying claims. It had become a large financial institution that invested in markets, bought government bonds, supported disinvestment programs, and at times even helped stabilise parts of the financial system.

So LIC ended up sitting in a very unique position in India’s financial system.

Which brings us to the most important question.

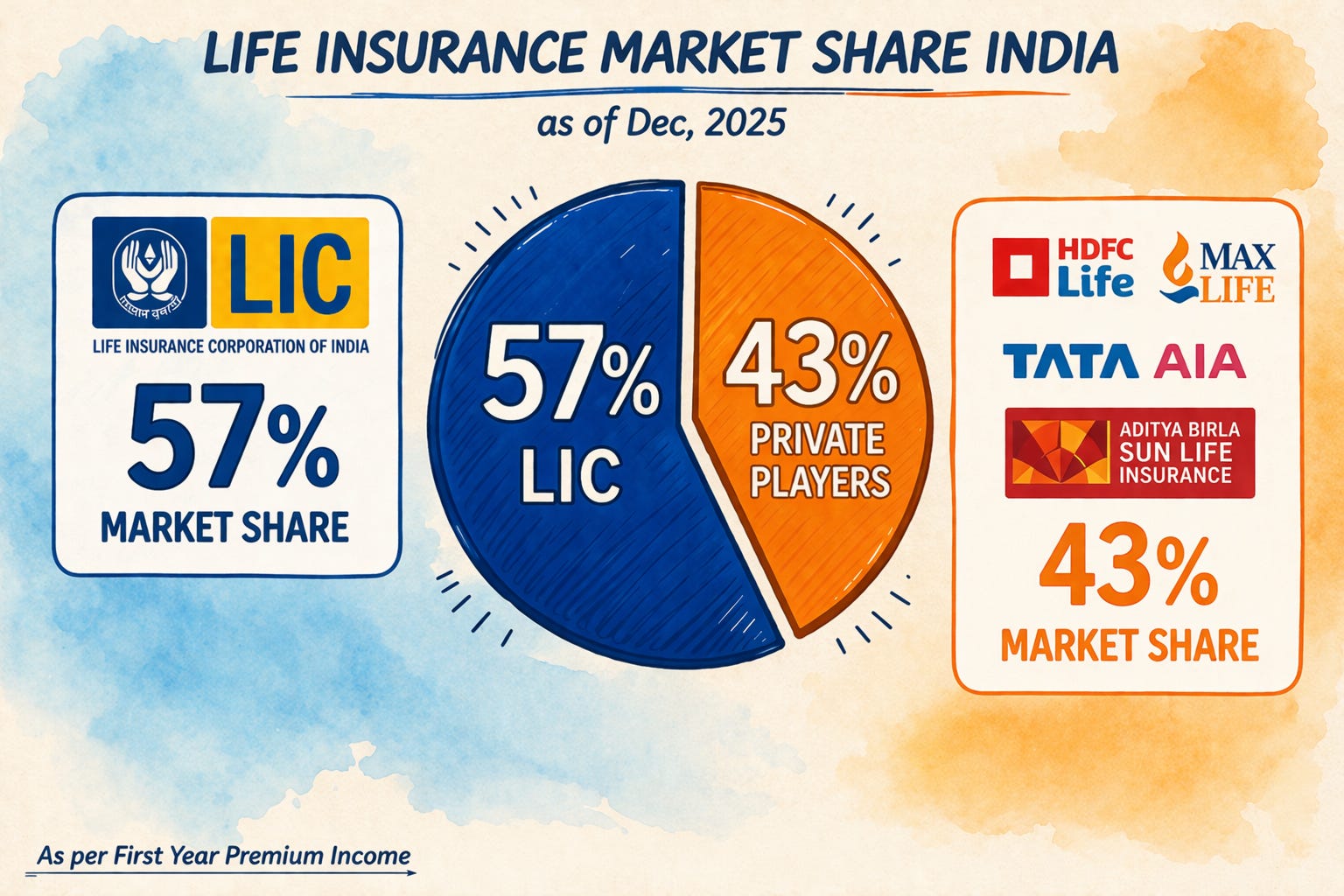

LIC is still the largest insurance company in India, even after private insurers, online platforms, and decades of competition.

So the real question is not just why LIC is big.

The real question is — how did LIC become so big that even after all this competition, its position is still so strong?

To understand that, we have to go back to the beginning.

We have to understand how LIC was created, how it built trust, how it built scale, and how over time all of this turned into one of the strongest moats in India’s financial sector.

How LIC’s Moat Really Began

To understand LIC’s moat, you have to go back to India in 1956. This is where the story really begins.

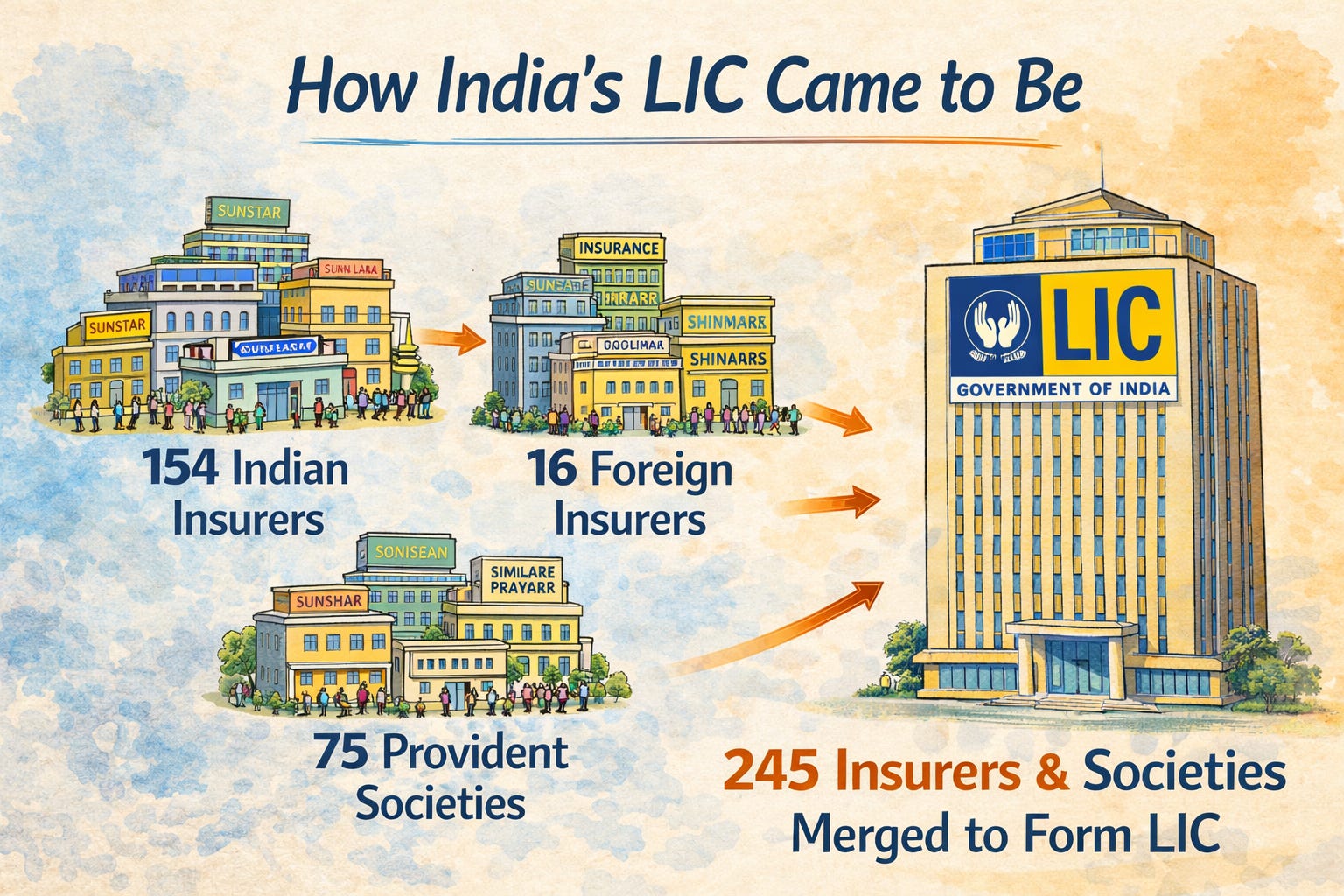

At that time, India did not have one large insurance company. Instead, the industry was made up of many small players: around 154 Indian insurance companies, 16 foreign insurers, and 75 provident societies. The industry was fragmented, loosely regulated, and in some cases mismanaged. Insurance involved people’s life savings, but the system itself was not always trustworthy.

Then a major scandal broke.

In 1956, parliamentarian Feroze Gandhi raised a case in Parliament involving misuse of funds by private insurance companies. Investigations followed, and one of India’s richest businessmen at the time, Seth Ramkrishna Dalmia, who controlled the Times of India group, was found guilty of financial misconduct involving insurance funds and was sent to prison. This scandal became the public trigger for a major government decision.

But the real reason was larger than just one scandal.

India in the 1950s was moving toward a socialist, state-led economic model. The government wanted control over key sectors and, more importantly, over long-term household savings. Jawaharlal Nehru even stated in Parliament that nationalising insurance was an important step toward building a socialist society.

So in January 1956, the government nationalised the entire life insurance industry.

And the way it happened was very direct. LIC did not slowly grow over time or compete and win market share. Instead, it absorbed 154 Indian insurers, 16 foreign insurers, and 75 provident societies (total 245 entities) along with their agents, branches, customers, and policies. All of this was merged into one government-owned corporation.

So LIC did not start like a normal company. It started with millions of policies, thousands of employees, a nationwide branch network, and the entire industry’s customer base already in its hands. At the time of the merger, the combined entities had assets of around Rs 4,110 million and more than five million policies already in force.

This is a very important point.

LIC did not build its early scale by competing. It inherited the entire industry in one move. That was the first foundation of LIC’s moat.

And then something even more powerful happened.

From 1956 to 2000, LIC was India’s only life insurance company. Anyone seeking life insurance had just one option. Over these 44 years, LIC built deep family relationships, expanded a vast agent network, earned multi-generational trust, and accumulated one of the country’s largest pools of long-term household savings.

By the time private insurers entered in 2000, LIC had already established unmatched scale, distribution, and trust. New companies were entering the market, but LIC had already become part of people’s financial lives.

The Sovereign Guarantee

One of LIC’s biggest advantages was not built through distribution, pricing, or investment performance. It was created by law in 1956, when LIC was formed.

Under Section 37 of the LIC Act, 1956, the Government of India guarantees all LIC policies. In simple terms, if LIC is ever unable to pay policyholders, the Government of India will step in and pay them. Every LIC policy is effectively backed by the sovereign.

This is an extremely powerful advantage. LIC policies are not just insurance contracts from a company; they carry something very close to a government guarantee, similar to government bonds. The promise is not only from LIC but also indirectly from the Government of India itself.

Private insurance companies in India do not have this advantage. They are regulated by IRDAI and must maintain solvency and follow strict rules, but there is no government guarantee behind private insurers. If a private insurer fails, there is no law that says the Government of India will repay policyholders.

This difference is especially important in a country like India, where trust plays a very large role in financial decisions. For many households, particularly first-generation savers and people in smaller towns and rural areas, the difference between “government-backed” and “private company” is often the entire decision.

In many ways, LIC agents were not just selling insurance policies. They were selling the backing of the government of India. That is a very different product from what private insurers were offering.

There is another legal provision that makes LIC even more unique.

Under Section 38 of the LIC Act, normal laws related to liquidation or winding up do not apply to LIC.

LIC cannot be liquidated like a normal company unless the central government itself decides to do so. In simple terms, a private insurance company can fail and be shut down under commercial law. LIC, by law, cannot go bankrupt in the normal way.

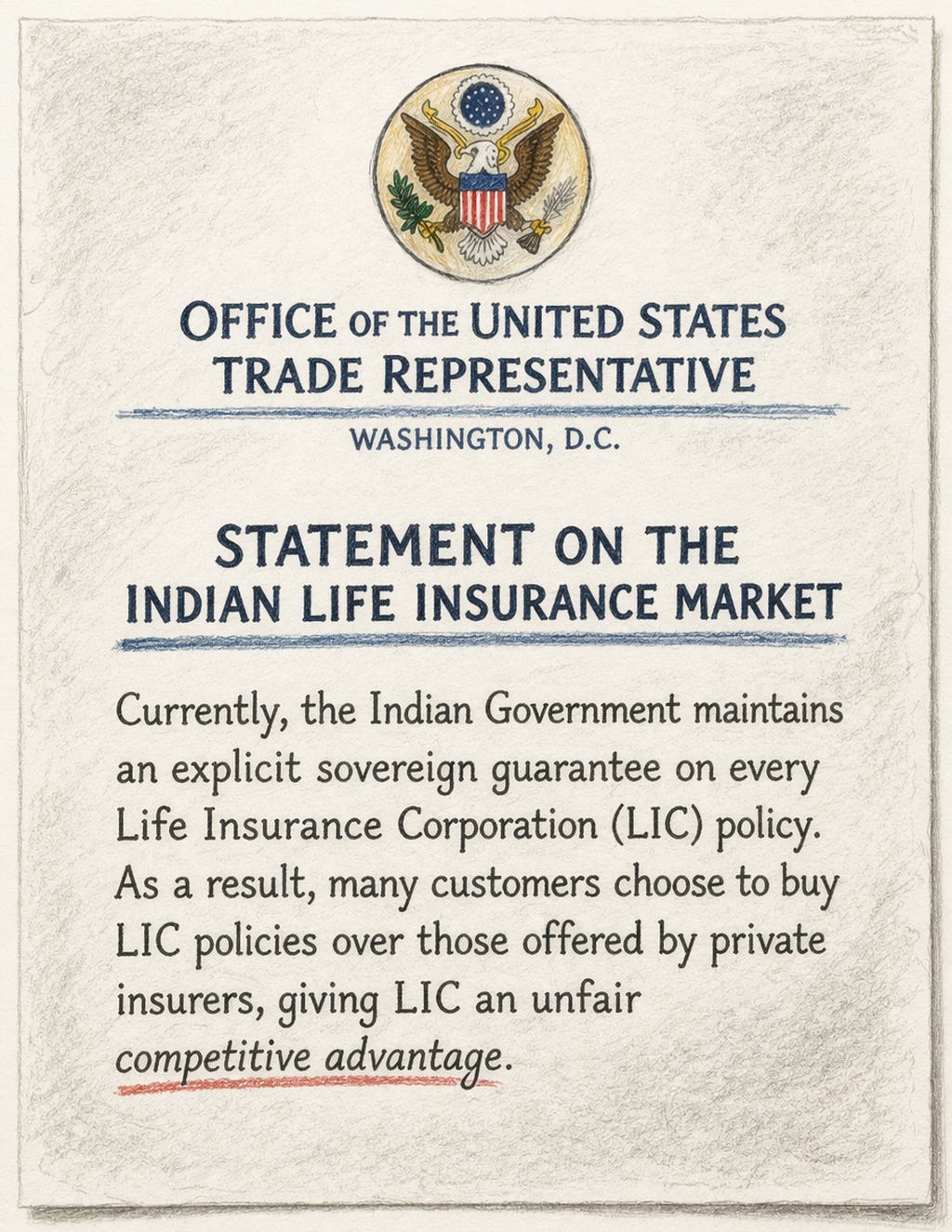

Even internationally, this advantage has been noticed. The Office of the United States Trade Representative has mentioned in its reports that India provides LIC with an uneven playing field because every LIC policy carries an explicit sovereign guarantee. Their argument is that many customers choose LIC over private insurers because of this government backing, which gives LIC a structural advantage.

LIC officially says that the guarantee does not materially affect competition. But from a behavioural point of view, the impact is obvious. If someone is choosing between two similar insurance policies, but one is backed by the Government of India and the other is backed by a private company, most people, especially for a product that may pay out decades later, might choose the government-backed option.

And that is why the sovereign guarantee is probably LIC’s most unique moat.

It is not a marketing or pricing or technology advantage.

It is a legal advantage that no private competitor can replicate.

The Distribution Network

If the sovereign guarantee is LIC’s legal moat, then its distribution network is its operating moat. This is where LIC’s everyday strength actually comes from.

LIC’s agent network was not built quickly. It was built slowly over decades, during a period when there were no private competitors in the life insurance industry.

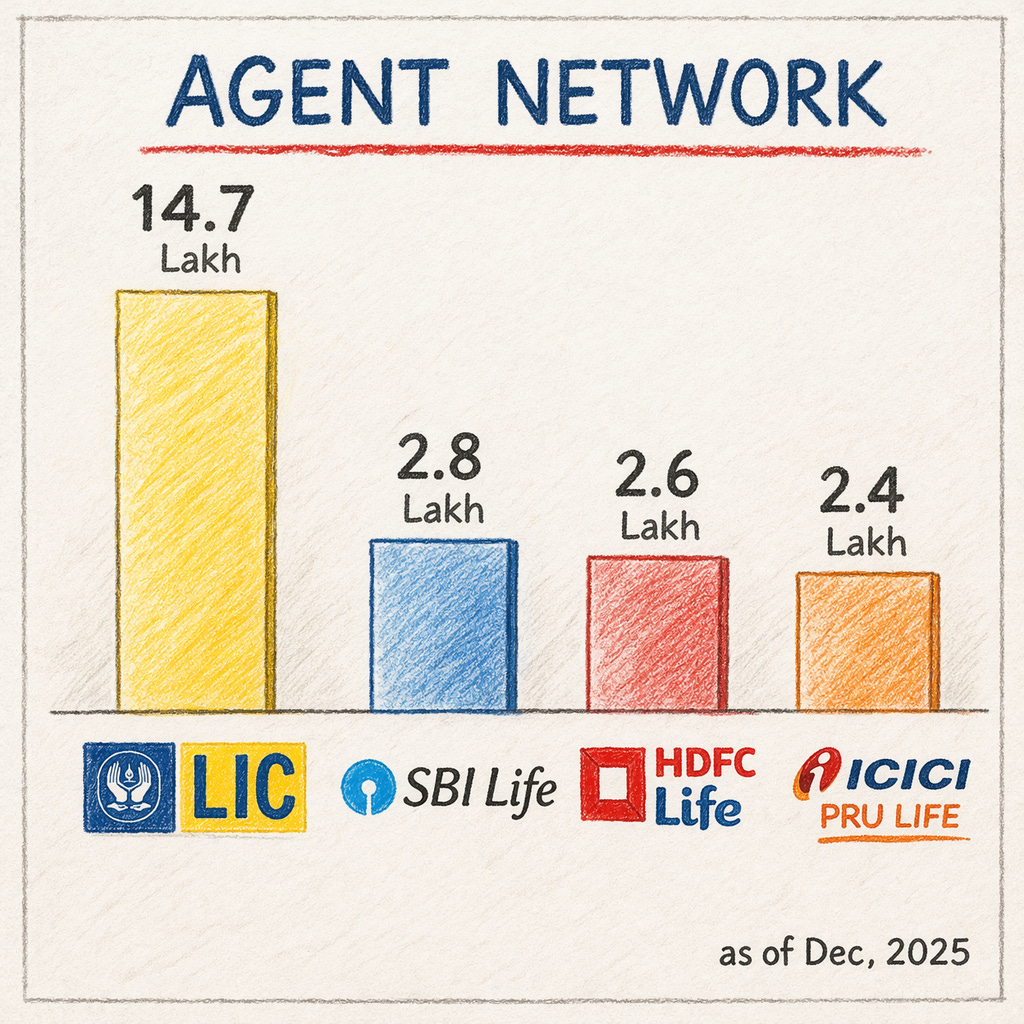

As of December 31, 2025, LIC had around 14.7 lakh agents. That is about 45% of all insurance agents in India and about 5 times the number of agents of the second largest life insurer.

This alone gives LIC a very large distribution advantage.

But the story is not just about the number of agents. It is also about how productive those agents are.

In Fiscal 2021, LIC agents generated an average individual new business premium of about Rs 4,13,000 per agent. For the top private insurers, this ranged from about Rs 1,02,000 to Rs 2,30,000 per agent. LIC agents also sold about 15.3 individual policies per agent on average, while agents of the top private insurers sold far fewer policies, about 3.9 for SBI Life, 1.3 for HDFC Life, and 0.9 for ICICI Prudential.

This gap exists because LIC agents are selling a brand that people already trust. The sovereign backing reduces customer hesitation, and LIC’s brand recognition answers the most important question customers usually have — whether the company will still exist and pay the policy decades later.

The geographic reach makes this advantage even stronger. LIC has thousands of offices across India, including a large presence in semi-urban and rural areas. LIC accounts for about 41% of the life insurance office network in India, with 5,004 offices across the country. Most of these offices are in smaller towns and rural regions where private insurers historically did not expand aggressively because the economics were difficult. Insurance in these markets depends more on long-term relationships and local presence than on advertising or digital platforms.

There is another important part of LIC’s advantage — renewal premiums. Life insurance is not a one-time sale. People pay premiums every year for many years. LIC has built a very large base of customers over decades, and millions of them continue paying every year. In FY2025, LIC collected about Rs 2,56,541 crore from these ongoing payments, compared to about Rs 62,495 crore from new policies. This means most of LIC’s money comes from existing customers, giving it steady and predictable income without having to sell new policies every time.

This steady flow of renewal premiums is closely tied to how LIC built its distribution network. Over time, LIC’s network became more than just a sales channel. In many towns and villages, the LIC agent is someone the family already knows — a neighbour, a relative, or a local professional who has handled insurance for the same households for many years, sometimes across generations. This created a relationship-based distribution system that is very difficult to replicate.

Private insurers can hire agents and open branches, but building millions of trusted relationships across the country takes decades. LIC had 44 years of monopoly between 1956 and 2000 to build this network before private insurers were allowed to enter the market.”

By the time competition arrived, LIC already had agents, customers, renewal premiums, and relationships across the country. New companies were trying to enter the market, but LIC was already deeply embedded in it.

That is why LIC’s distribution network is one of its strongest moats. Not just because it is large, but because it has been built and reinforced over several decades and continues to generate both new business and renewal business every year.

The Investment Flywheel

One of LIC’s most powerful advantages is not just that it sells insurance, but what it does with the money after collecting premiums. This is where LIC’s scale starts creating a self-reinforcing advantage that private players simply cannot match.

LIC collects enormous premiums every year. That money does not sit idle. It gets invested in government bonds, stocks, infrastructure projects, and large companies across the country. Over time, this has made LIC not just India’s largest life insurer, but also one of the largest institutional investors in India.

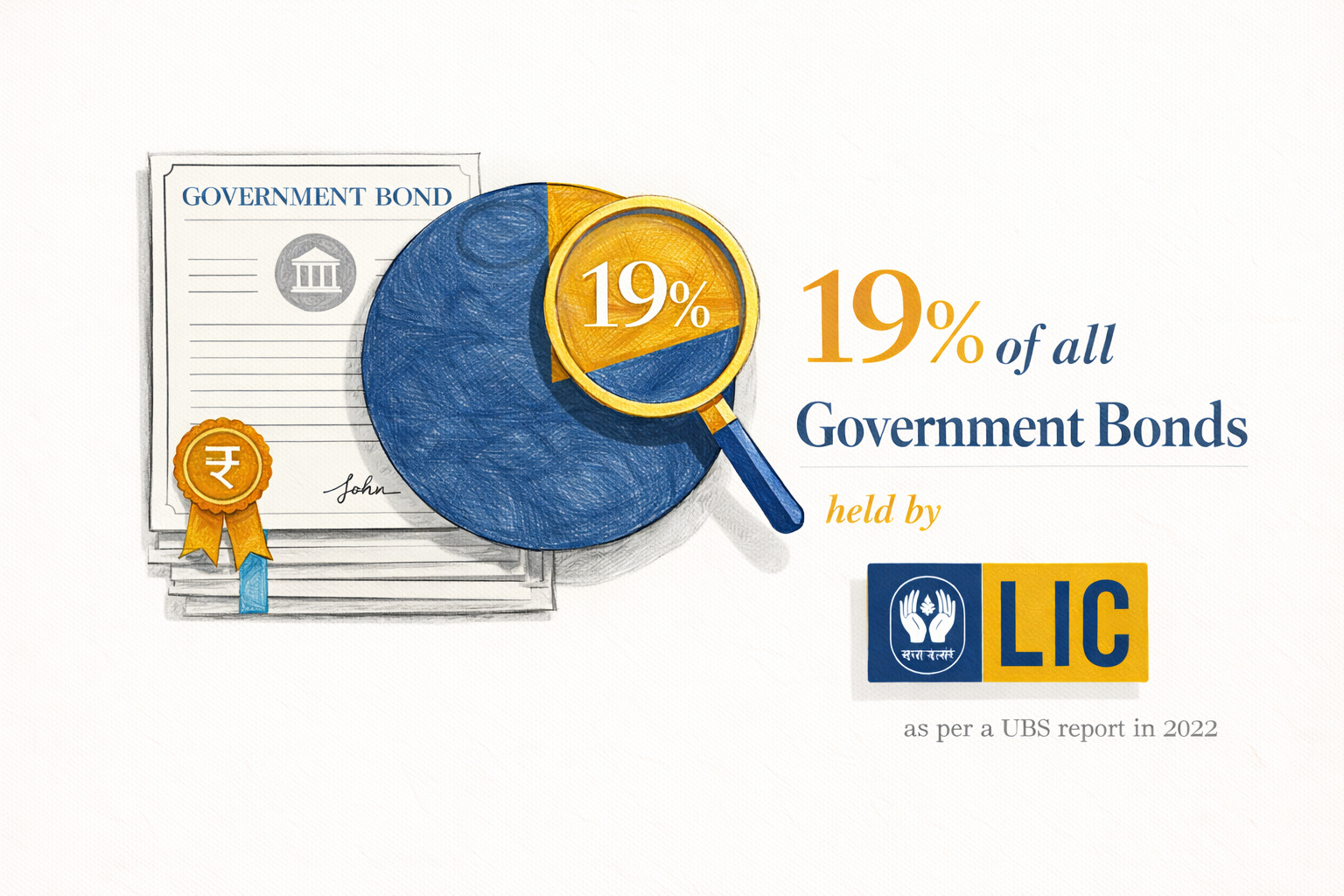

As per a UBS report from 2022, LIC was among the largest lenders to the central and state governments of India, as 19% of all government bonds were held by LIC alone.

LIC holds investments in hundreds of listed companies, and its investment portfolio runs into many lakh crores. It holds significant stakes in some of India’s largest companies like Reliance Industries, ITC, State Bank of India, Infosys, and HDFC Bank. In many companies, LIC is one of the largest shareholders. LIC also has nominee directors on the boards of several companies, including PSU banks. Over time, this has created a web of influence, access, and relationships across the Indian corporate and financial system that no new insurance company could realistically build from scratch.

This creates what can be called an investment flywheel.

The cycle works like this. LIC collects premiums from policyholders. It invests that money at a very large scale. Those investments generate returns. LIC then declares bonuses to policyholders. Those bonuses make LIC policies more attractive. More people buy LIC policies. That brings more premiums. More premiums mean more money to invest. And the cycle continues.

Each cycle reinforces the next.

Scale matters a lot in investing. When an institution manages very large amounts of money, it gets access to IPO allocations, large debt issuances, government securities, infrastructure financing, and investment opportunities that smaller institutions may not easily get access to. Because of its size alone, LIC has a seat at almost every major financial table in India.

Over time, this has created another moat. LIC is not just competing with private insurers on insurance products. It is competing with the scale of its investment engine — and that scale keeps compounding year after year.

This is why LIC is not just an insurance company that invests money. It is an investment institution that is funded by insurance premiums. And once an institution reaches that level of scale, the advantage starts reinforcing itself.

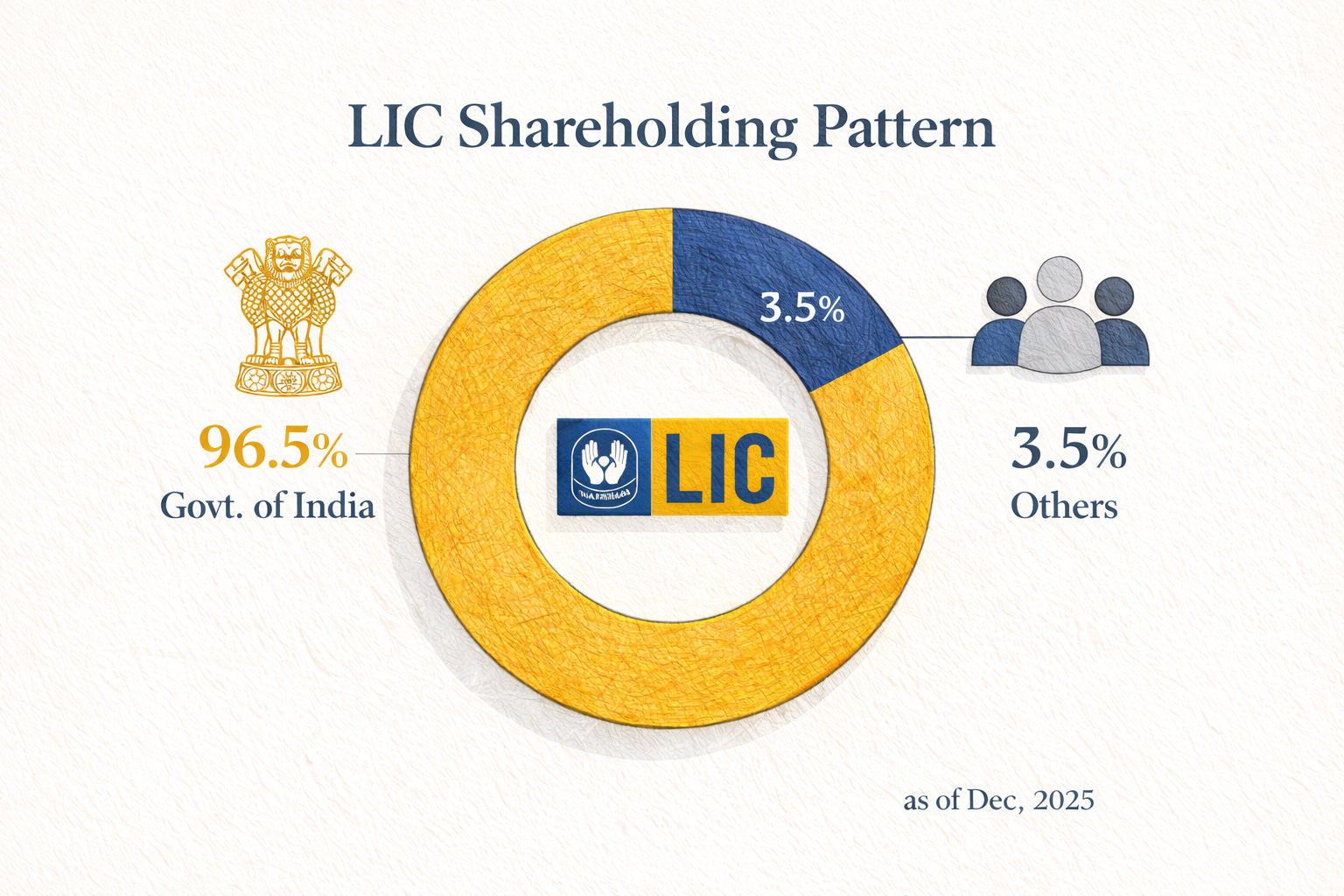

Government Ownership

Another very important moat for LIC comes from the fact that it is still overwhelmingly owned by the Government of India.

Even after the 2022 IPO, only a small portion of LIC is publicly owned, while the large majority is still held by the government. This makes LIC very different from private insurance companies.

Government ownership creates several structural advantages for LIC. One of them is what can be called mandated or natural business flows. Many large group insurance schemes related to government employees, social insurance schemes like PMJJBY, and insurance coverage for defence personnel often flow through LIC either by design or by preference of governments.

This creates a steady institutional pipeline of business that private insurers cannot easily access.

Another advantage is the capital backstop. Private insurance companies have to constantly maintain capital ratios, and, if they face losses or bad years, they may need to raise money from investors or markets. LIC, on the other hand, has the Government of India behind it. Its capital base is effectively supported by the government, which reduces the risk of capital stress in difficult years.

There is also the regulatory and political alignment advantage. For decades, LIC operated in an environment where it was effectively the only insurer in the country, and even after the insurance sector opened up and the regulator was formed, LIC continued to have deep knowledge of the regulatory system and strong relationships across government institutions and ministries. LIC is not just a financial company; it has often been used as a tool of national financial policy.

Over the years, governments have used LIC in multiple situations — sometimes to support falling stock markets, sometimes to buy stakes in companies, sometimes to support disinvestment programs, and sometimes to step in when financial institutions were in trouble. This relationship between LIC and the government is a double-edged sword, but it also shows something very important.

LIC is structurally embedded in India’s financial system in a way that no private insurer can replicate.

And that itself becomes a moat.

The Annuity and Rural Moat

After distribution, investments, and government ownership, there are two more areas where LIC has a structural advantage.

Annuities and rural markets are very different businesses, but both depend on the same things: trust, scale, and long time periods.

The Annuity Moat

LIC dominates the annuity and pension segment in India by a very large margin. As of March 31, 2025, LIC manages approximately Rs 13.68 lakh crore in annuity and pension assets — roughly 85% of the entire industry’s annuity AUM of Rs 16.10 lakh crore. The nearest competitor, SBI Life, manages around Rs 72,000 crore, making LIC’s annuity book approximately 19 times larger.

An annuity is a retirement income product where a person gives a lump sum and receives income for the rest of their life. This means customers are trusting the insurer to still exist and keep paying money 20 or 30 years in the future, so safety and trust matter more than returns. LIC has an advantage here because its policies are backed by the Government of India under the LIC Act, which private insurers cannot offer.

Scale also matters in annuities. Pricing depends on predicting how long people will live. The larger the annuity customer base, the better the data and pricing models. LIC’s large annuity book gives it better pricing and risk modelling, which attracts more customers and increases scale further.

There is also a long-term structural trend supporting this business. India ranked last among 48 countries in the Mercer CFA Global Pension Index 2024. Pension assets are only about 17% of GDP, only about 12% of the workforce has pension security, and more than 85% of the labour force is in the informal sector. India’s old-age dependency ratio is expected to reach about 20% by 2050. This means the annuity market is likely to grow significantly in the coming decades, and LIC is already the largest player.

Under the National Pension System, retirees must use at least 40% of their retirement corpus to purchase an annuity from approved providers, and LIC is one of the approved annuity providers, which further supports LIC’s annuity business.

The Rural Moat

The second advantage comes from LIC’s rural presence. Rural markets account for about 55% of LIC policies, and LIC maintains about 14.7 lakh agents across India, ensuring presence across rural, semi-urban, urban, and metro areas. Only about 20% of rural households currently have life insurance, which means there is still a large untapped market.

LIC has also been expanding this rural network through government-backed programs like the LIC Women Agent Scheme launched in December 2024, under which about Rs 62.36 crore was disbursed as stipend in FY 2024–25 to support rural women agents.

The rural advantage comes from relationships and long-term presence. In many villages, LIC agents are known to families and have served the same households for many years. This kind of trust-based distribution is difficult to replicate quickly through digital platforms or bank partnerships.

However, rural markets are changing. As of March 2024, India had about 398 million rural internet subscribers, and about 95% of villages had 3G or 4G connectivity. This means digital insurance distribution in rural India is becoming more viable, and private insurers are investing in these channels.

So the rural moat is not that competitors cannot enter rural markets. It is that LIC has a multi-decade lead in trust, distribution, and presence that will take competitors many years and large investments to catch up.

Good research article.

But too much lengthy.

Good information