The Hunt brothers were accused of cornering the silver market.

In the 1970s, inflation was rising.

One classic way to fight inflation is to hedge it.

You have to invest in assets whose price will go up. This way, even if things are more expensive, you will have more money.

That way, your buying power will remain the same – or even go up.

The Hunt brothers believed that, due to inflation, everyone would try to buy silver to hedge. This would cause the price of silver to rise.

So they determined silver would make an excellent investment.

Towards the end of the 1970s, they started buying silver aggressively. The two brothers came from a very wealthy family, so they had enough money to buy silver.

Soon, their accumulated silver grew to massive amounts. So massive that they had a fraction of the total silver in the world!

They were still bullish on the metal. They wanted to buy even more silver before its price went up.

They started buying futures contracts – with margins.

Futures & Margin

Futures Contract:

Those who trade using F&O would know this well. But still, we will explain briefly.

Futures contracts are contracts to buy an asset in the future – at a fixed price.

Let’s say you buy a futures contract that says you will buy a share at Rs 100 after 2 weeks.

2 weeks later, the price is Rs 120. Since you have a futures contract at Rs 100, you will pay Rs 100, not the current price of Rs 120.

This can go the opposite way too.

If the share price falls to Rs 80, you will still have to pay Rs 100. And you cannot refuse. It is a contract you have to honour.

Margin:

Investing using borrowed money – that’s called margin.

When an investor opens a margin account, they are able to borrow money and invest. Usually, it is determined using the amount invested.

Example: let’s say you bought shares worth Rs 20,000. The broker might offer you a margin of Rs 20,000 more.

So you will be able to buy Rs 40,000 worth of shares using only Rs 20,000.

It’s a loan. And the collateral is the shares you bought.

Going forward, the broker will ask you to keep a certain amount of money/shares in the account for the margin – to maintain the value of the collateral.

Margin Call Explained

Margin sounds good when the share price is going up.

But what if the share price goes down?

Well, in that case, things get a bit tricky.

The broker has lent money keeping the shares you bought as collateral. But if the value of those shares reduce, the collateral is no longer a proper collateral.

So in this case, the collateral needs to be increased.

Let’s say you had put in Rs 20,000 and the margin given to you was Rs 20,000 more. So you bought shares worth a total of Rs 40,000.

But then, the share price fell, and now the total value is down to Rs 36,000.

This is Rs 4,000 less than what it used to be.

But the margin given to you was for Rs 20,000, not Rs 16,000. There’s a difference of Rs 4,000.

You will get a margin call.

Margin call: the broker will ask you to add Rs 4,000 more to your account or buy shares worth Rs 4,000 more – to ensure that the value of the collateral is equal to the value of the margin taken by you.

If you do not want to buy more shares or add more cash, you can sell some of your shares and pay back the margin.

If the share’s price falls further, you will get more margin calls.

What happens if the share price continues to fall and you do not add more money or buy more shares?

In such a case, the broker will be forced to sell assets to recover the margin given.

This is an extremely simpified version.

In reality, there’s something called the maintainance margin requirement.

It is usually between 30% and 40%.

This means that the value of your purchased shares should be greater than a certain percentage of the total value.

Let’s take the same example mentione above.

So, the total value of your shares is Rs 36,000 right now. And after reducing Rs 4,000, you are left with Rs 16,000.

Let’s say the margin maintaince requirement is 40%.

So now we calculate:

(16,000 ÷ 36,000) x 100 = 44%

This is higher than 40%. No margin call is required.

When will there be a margin call?

Let’s say the share price falls even further. The total value is now Rs 32,000 (from an earlier value of Rs 40,000).

So, we remove the margin amount from the total value.

Rs 32,000 - Rs 20,000 = Rs 12,000

Is this below the margin maintaince requirement of 40%?

(12,000 ÷ 32,000) x 100 = 37.5%

Yes. Since 37.5% is lower than the margin maintaince requirement of 40%, the investor will get a margin call.

Hunt Brothers’ Silver: Aftermath

In the case of the silver futures contract, the Hunt brothers chose to take delivery of the silver when the contract expired.

F&O investors usually don’t take delivery. They square it off by selling at the market rate.

The Hunt brothers had accumulated 100 million ounces of silver — over 2,800 tons!

According to some rumours, this was around 1/3rd of the total supply of silver in the world.

They kept on buying on margin.

This seemed like a case of trying to corner the market. This is a form of manipulation of the markets.

How?

If you reduce the quantity of silver available to trade, the price starts shooting up or down faster.

Think about it. If there are many sellers and buyers, the chances of share prices remaining similar to the last trading price are higher – there are more sellers and buyers so competition is higher. It is hard to dictate the price.

But if the number of buyers and sellers is low, and/or, the number of shares on sale is low, the sellers can easily influence the prices.

In the 1980s, this is what was being feared.

So, the exchanges decided to make changes to the rules on margin.

This made it difficult for the Hunt brothers to buy more using margin. They were sitting with large quantities of silver.

The word got out. Everybody started talking about it. And they felt that the Hunt brothers had manipulated the price of silver to rise up.

They feared the price would crash.

So they started selling.

And with that, the price of silver started falling.

As the price fell, more investors panicked and sold their silver. The price started to fall even faster.

The Hunt brothers started getting margin calls.

They tried to sell their silver. But that heavy selling crashed the price even more – they just had that much silver with them!

So, now, as the price is falling even harder, they started receiving even more margin calls.

They eventually declared bankruptcy.

They were charged with trying to corner the price of silver – by buying a lot of it and reducing the supply of silver in the markets.

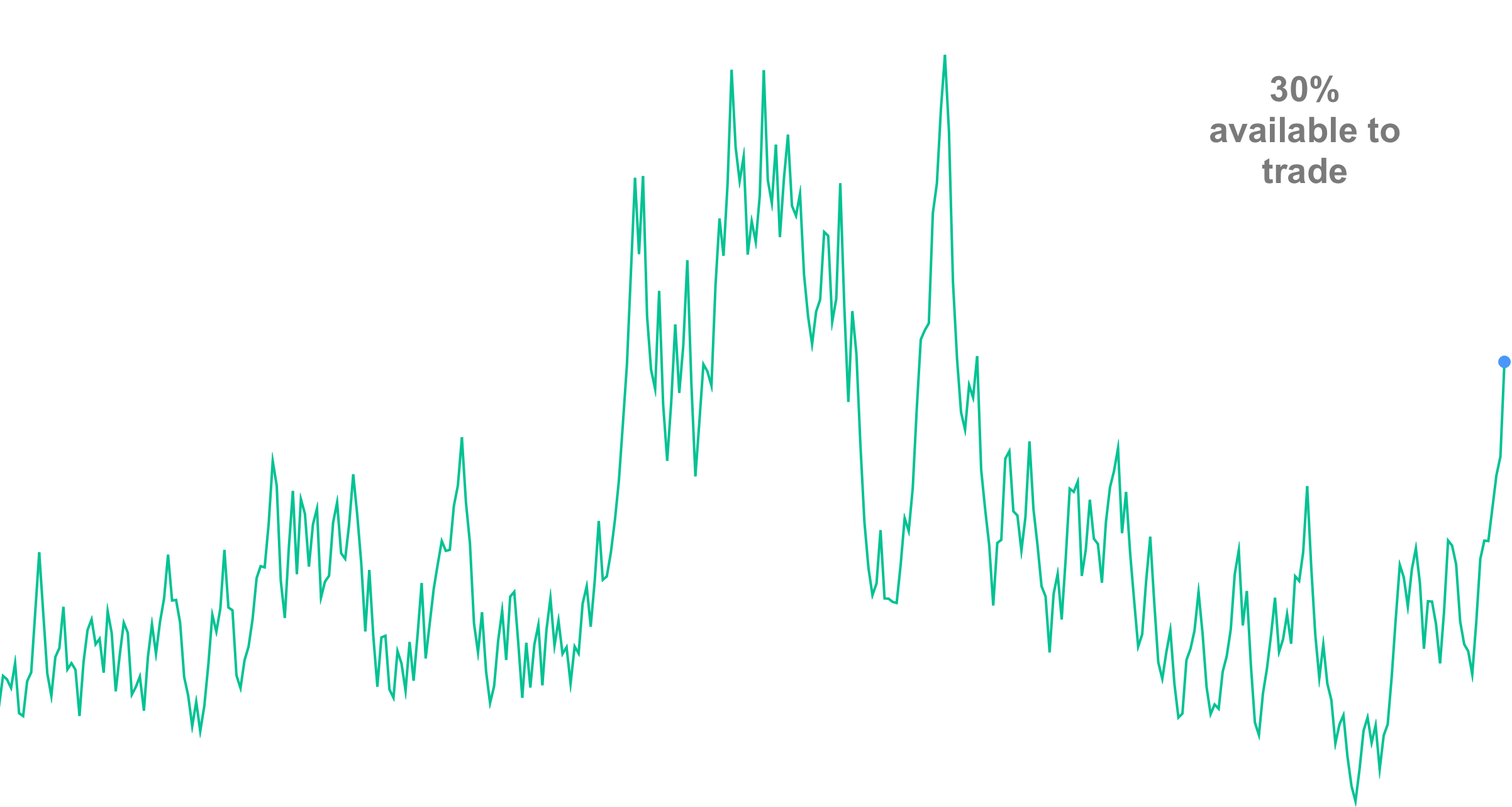

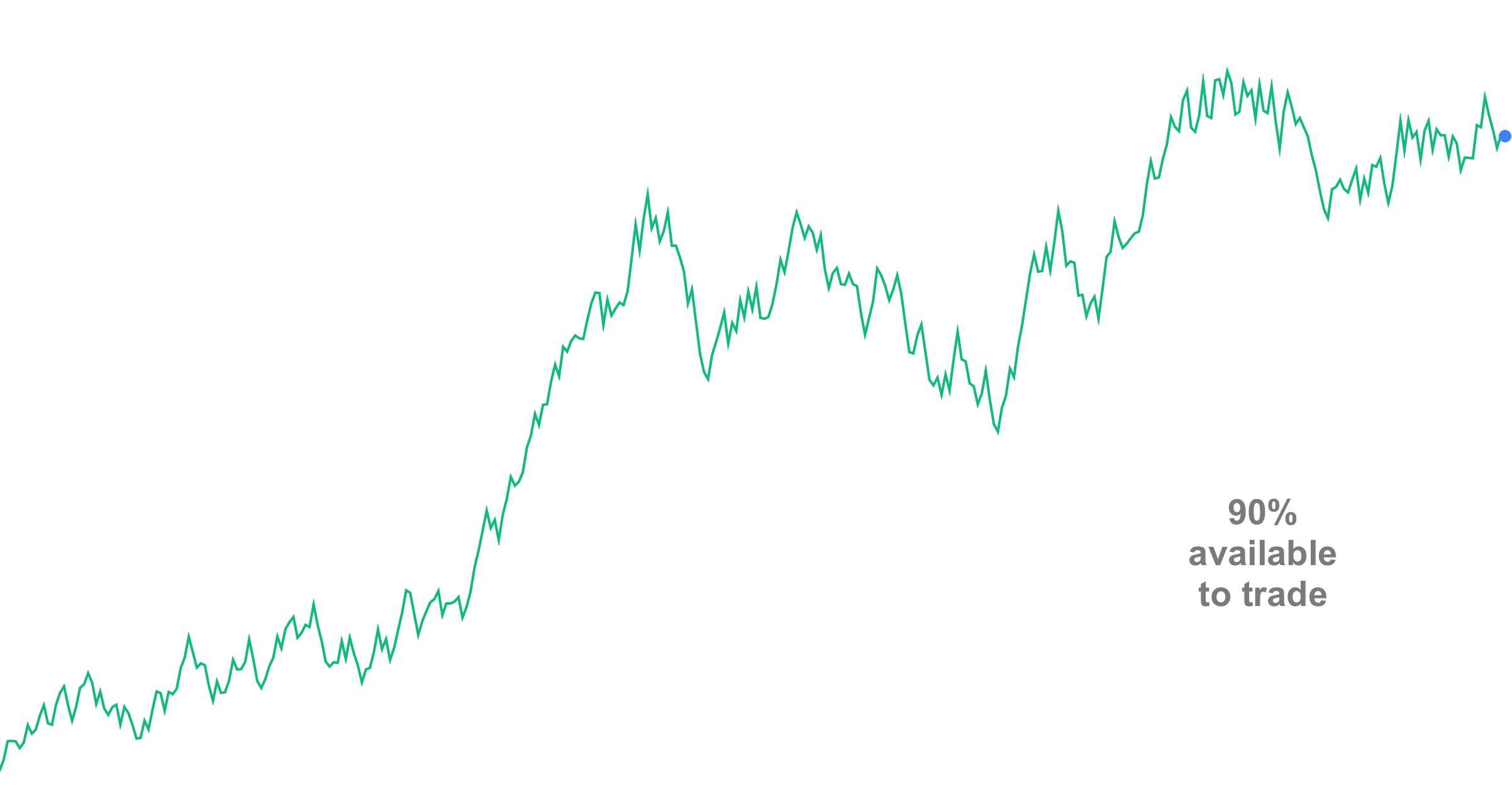

We ran two small simulations.

We made a bunch of investors trade randomly.

In the first simulation, we kept only 30% of the total shares in the markets. The rest were not available to trade.

In the second simulation, we kept 90% of the total shares in the markets. The rest were not available to trade.

We see that when a smaller number of the total shares are available in the markets, the prices can swing wildly – up and down.

So whoever has more shares can cause the markets to crash by selling.

When there are more shares, the ups and downs are gentler.

The Hunt brothers were accused of trying to corner the markets by accumulating a huge amount of silver.

They defended themselves saying they were just trying to hedge against inflation.

The case was eventually settled with them losing their money.

Crash

The price of silver in the early 1970s was around $2 for one ounce (about 32 grams).

That’s when the Hunt brothers had started buying it. As the buying continued, it rose to $6 in 1979.

By the end of that same year, it had touched $25.

When the new year started, the price had crossed a massive $50.

This is when the exchanges and regulators brought in the regulations.

When the word got out, the price started falling sharply.

On March 27, 1980, the Hunt brothers’ major margin call default triggered a massive crash in silver prices. It fell by over 50% in a single day.

Some time later, it crashed further, only to settle around $11.

That day – March 27, 1980 – came to be known as Silver Thursday.

‘Margin call’ is one of the scariest phrases in the trading world.

Could something like this happen again?

No, not in this manner. Whenever something like this happens, regulators jump in to analyse and see what went wrong.

Such events lead to the creation of rules and regulations to prevent something like this from happening again.

Still, there can be newer ways in which a crash comes about.

The Hunt brothers’ example is a perfect demonstration of how margin can be an excellent tool when things go right – but can backfire horribly when overdone.

Movie

There is a movie called ‘Margin Call’ released in 2011.

It is not about the Hunt brothers.

But it is a fantastic story on margin call; of how an investment company realises that they had taken margins exceeding the value of their company.

If the prices went down, they would not be able to honor their margin calls and would go bankrupt.

The story goes on to show how, over one night, they made plans to deal with this problem – and how they dealt with it the moment the markets opened the next day.

Did they succeed in saving the company?

The movie’s tone is thrilling but lacking in action. It concentrates on being realistic with an amazing portrayal of dialogues and the underlying seriousness of the situation.

We won’t spoil the story.

Watch the movie – you’ll understand margin calls extremely well.

Quick Takes

+ India’s annual retail inflation rate fell to 2.10% in June (vs 2.82% in May). Wholesale inflation fell to -0.13% (vs 0.39% in May). Negative inflation means items actually got cheaper.

+ NSE has launched its monthly electricity futures today. It recorded more than 4,000 lots of contracts as of 2 pm.

+ Jane Street deposited Rs 4,843 crore in compliance with SEBI to resume trading in India.

+ India’s trade deficit stood at $18.78 billion in June (vs $21.88 billion in May). Merchandise exports showed a marginal decline of 0.06% year-on-year while merchandise imports fell 3.7%.

+ The USA's retail inflation rate rose to 2.7% year-on-year in June (vs 2.4% in May). Core inflation (excluding food and energy) rose to 2.9%.

+ China’s GDP grew 5.2% year-on-year in the April-June quarter (vs 5.4% in Jan-March quarter).

+ India’s passenger vehicle sales stood at 3.13 lakh units in June, a fall of 7.3% year-on-year.

+ India’s unemployment rate stayed constant at 5.6% in June. Urban unemployment rate rose to 7.1% in June (vs 6.9% in May).

+ The central government authorised NTPC to invest up to Rs 20,000 crore (up from Rs 7,500 crore earlier) in NTPC Green and other JVs/subsidiaries to achieve 60 GW renewable energy capacity by 2032. It also said that India now has over 50% of its installed power coming from non-fossil fuel sources (5 years ahead of its 2030 Paris Agreement target).

+ The UK's inflation rate rose to 3.6% year-on-year in June (vs 3.4% in May). Core inflation (excluding volatile items like food and fuel) stood at 3.7% (vs 3.5% in May).

+ Anthem Biosciences IPO was subscribed 63.86 times. Retail subscription: 5.64 times. IPO closed for subscription.

+ Smartworks Coworking IPO got listed on the stock exchanges at a 6.88% premium over its issue price and closed 9.35% up.

+ Euro Area’s inflation rose to 2% year-on-year in June (vs 1.9% in May). Core inflation stayed constant at 2.3%.

+ Japan’s exports declined 0.5% year-on-year in June (vs a fall of 1.7% in May), while imports rose 0.2% (vs a fall of 7.7% in May).

+ SEBI proposed to standardize the valuation of gold and silver ETFs by using domestic commodity exchange benchmark prices instead of international benchmarks like the LBMA (London Bullion Market Association).

+ Japan’s inflation rate fell to 3.5% year-on-year in June (vs 3.7% in May). Core inflation also fell to 3.3% (vs 3.7% in May).

+ The European Union imposed sanctions on a Russian owned oil refinery in India and lowered the oil price cap. This move aims to limit Russia’s war funding.

+ India’s foreign exchange reserves fell by $3.06 billion to $696.67 billion in the week that ended on 11 July.

+ India’s first indigenously designed and constructed diving support vessel, INS Nistar, was inducted in the Indian Navy. The vessel is designed for deep sea diving and rescue operations.

6-Day-Course

Theme of the week: understanding MF returns

Question 1:

Why is it not practical to invest only in the top mutual fund?

-High risk

-Keeps changing

-Low returns

Question 2:

What is a better approach to handle changing mutual fund returns?

-Frequent adjustments

-Timing markets

-Long-term investing

Question 3:

Short-term mutual fund returns can be heavily influenced by the sectors a fund is invested in.

-True

-False

Question 4:

Why shouldn't mutual funds be judged based on short-term returns?

-High taxes on returns

-Fund fees are higher

-Volatility is high in the short-term

Question 5:

Mutual fund returns can vary depending on the start and end dates used for measurement.

-True

-False

Answers:

Q1: Keeps changing

Q2: Long-term investing

Q3: True

Q4: Volatility is high in the short term

Q5: True

The information contained in this Groww Digest is purely for knowledge. This Groww Digest does not contain any recommendations or advice.

Team Groww Digest