Hard to imagine, but the US fought a civil war.

It lasted from 1861 to 1865.

One half of America fought the other half of the country.

It had only been a few decades since trains had come into existence. Their expansion had started in the UK and soon they arrived in the US.

Unlike the UK, the USA was a much more vast country.

Population density was lower, but so was the potential for growth.

Gradually, the railroads started getting built. They were mostly localized, built by companies operating them.

The Civil War brought their true role to the forefront. The trains proved their worth transporting troops and equipment.

Ultimately, the North won. Their railway network played a key role.

Railway Boom

During the war, the US government understood the value of having a superior rail network.

In 1862, they passed the Pacific Railway Act.

The act facilitated the first transcontinental railway line. The railway line that would start on the East Coast and run till the West Coast of the USA.

The US government had funded the Civil War using war bonds. The bonds were offered to investors by the government as an investment option. The bonds were backed by the US government.

It worked well.

Since a lot of money was being raised by the government for the war, lots of bonds were available. The Civil War bonds popularised the idea of investing in bonds among individual citizens much more.

In that backdrop, offering railroad bonds seemed like a great idea.

Building railroads required vast amounts of land, iron, and manpower. Lots of money was needed again.

Railroad bonds became mainstream — somewhat like Civil War bonds.

But there was one key difference. War bonds were offered by the government of the US. Railway bonds were offered by private railroad companies.

Bonds

Bonds are essentially loans.

The bond issuer = the loan taker

The bond buyer/investor = the loan giver

So, if you buy a bond, you are giving a loan to the person giving you a bond.

A bond is a certificate. On the certificate, the bond issuer says that they promise to pay you a certain amount of interest and will return the borrowed amount by a certain date.

Coupon rate = interest rate

Maturity date = when it will be paid back

Principal = amount they are borrowing

Schedule = schedule of payment of interest & principal

And of course, the bond mentions the issuer’s details. In the case of the government of the USA, the bond issuer is the government itself.

If the issuer is a private company, then its name is mentioned.

The coupon rate or the interest rate is a crucial factor in the case of bonds.

Bonds promise to pay back the money along with interest. Fixed interest, fixed returns.

But can you trust the bond issuer’s words? Will they not cheat?

Even if they are well-intentioned, can they still fail and shut down?

These questions always arise when buying bonds.

No doubt, some bond issuers are more likely to pay, while some are less likely.

This is why the interest rate offered is different.

Bond issuers who are less likely to pay back (for whatever reason) offer a higher interest rate to compensate for the risk.

More stable and secure bond issuers offer lower interest rates.

Companies can fail, or worse, cheat. Governments can fail too.

The US government bond rates are some of the lowest in the world (in present times). They are considered incredibly reliable and stable.

Other countries’ government bonds usually have higher rates but are still considered pretty stable. India’s government bonds are also considered very stable.

Very large and diversified companies are also considered very reliable (though still less reliable than governments).

So, in short, higher risk, higher return.

Which many take to mean, guaranteed higher returns. The “risk” part of this gets ignored.

Why?

Probably because the bond certificate clearly mentions the interest rate and payment schedule.

There’s one more detail. Bonds can also be sold.

Let’s say you own a bond certificate. You can sell the bond to your friend for a price you want. Once sold, the bond certificate is your friend’s. All pending interest and maturity amount belong to that friend.

Just like stocks can be bought and sold, bonds can also be bought and sold on the exchanges (till they mature).

Railway Bonds

So, private companies are being helped by the US government.

The government wants more railroads to be built in the country. So they offer grants, land, and other such schemes to railway companies to encourage them to build railroads.

Unfortunately, this attracts problems of its own.

Seeing railroad lines come up in various parts of the country, individual investors turn very bullish.

They noticed how once a railroad and stations are built, the economy of the region changes for the better.

Movement of people and goods becomes easier, faster, and more convenient.

When the initial few railroad bonds started maturing, early investors got the lucrative returns they were promised by the bonds.

Couple this observation with the recent success of government-issued war bonds, and bonds start seeming more and more irresistible.

Seeing success stories around them, more investors wanted to invest in railroad bonds.

And this is where more railroads started being built. Once companies ran out of routes to build on, they moved to less populated areas. The future traffic was assumed to be high.

Many of these assumptions were wrong.

But the funding was cyclical. Companies raised more money using bonds, to build more lines. But many of the lines were not profitable or lucrative.

The industry came to depend more on money raised via bonds, and less on its profits from operating railroads.

It became a vicious cycle.

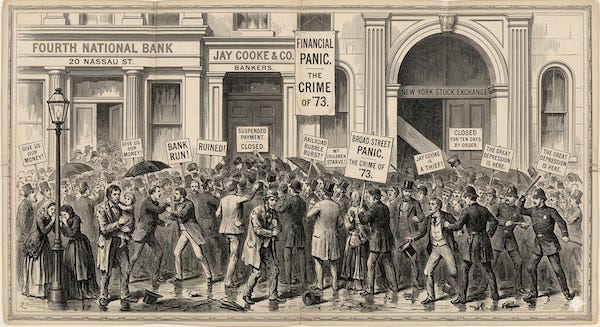

The domino crashed when one of the biggest sellers of railroad bonds, Jay Cooke & Co, was unable to sell more railroad bonds in 1873.

Seeing this, panic set in. Investors rushed to sell off their railway bonds. This sell-off crashed the bond prices.

Since the bonds were not wanted anymore, railroad companies struggled to raise more money. They did not have enough money to pay interest. They started defaulting, and going bankrupt.

The contagion spread.

Banks started experiencing bank runs. Railroad companies started collapsing. The economy started stuttering. The impact was on all parts of the economy.

The impact was so massive, the US economy entered a depression that lasted about 6 years. It came to be known as the Panic of 1873.

Eventually, the economy of the US picked up again. Some of the earlier built railroads started to make money.

More lines started being built. Investors gradually started trusting railroad companies again — and slowly, they started buying railroad bonds again.

The period between 1850 and 1900 is called the Gilded Age. Most of America’s railways were built in this era.

Boom & Bust

Once something of this scale happens, one would imagine it would not repeat.

Unfortunately, history is filled with examples of this exact cycle repeating again and again.

A crisis happens.

Investors become cautious.

Bonds start giving reliable returns.

More investors flock to invest in bonds.

More bond issuers flock to issue bonds.

Caution is relaxed.

Bad quality bonds start being offered.

This builds.

Eventually, the bubble bursts.

And, a crisis happens.

The Panic of 1873 was not the first. There were many before it. There were many after it.

Some of the biggest financial crises across the world exhibit this trait.

Argentine Bond Crisis AKA Baring Crisis (1890)

Great Depression (1929)

Asian Financial Crisis (1997)

Global Financial Crisis (2008)

These are some of the most talked about examples.

But these are not the only ones. There are many many more such examples on much smaller scales (thankfully).

It appears that investors tend to assume that all bond issuers are the same; that promised returns will always be paid.

It almost seems like investors don’t differentiate between bonds issued by the likes of the US government and those that are issued by companies with questionable track records.

The past cycles show us the same repeating pattern.

Whenever investors lowered their caution to chase after higher returns, things have not worked well for long.

Quick Takes

+ India’s composite PMI (manufacturing + services) fell to 57 in March (vs 58.9 in Feb). Services PMI fell to 57.5 (vs 58.1 in Feb). This means overall economic activity grew more in Feb than in March.

+ The government doubled the daily allocation of 5 kg Free Trade LPG cylinders for migrant labourers in each state beyond the earlier 20% limit, based on demand. Natural gas supply to industrial and commercial sector networks has been increased by 10% to meet rising demand.

+ Zepto received in-principle approval from SEBI for an IPO: as per media sources.

+ The US and Iran agreed to a 2-week ceasefire after more than a month of military conflict.

+ The RBI kept the repo rate unchanged at 5.25%.

+ The government approved Rs 26,069.50 crore for construction of Kamala hydro electric project in Kamle, Kra Daadi & Kurung Kumey districts of Arunachal Pradesh. It also approved Rs 14,105 crore for a 1200 MW Kalai-II hydro electric project in the state’s Anjaw district.

+ An Indian delegation will visit the US capital later in the month to discuss the trade deal which was put on hold due to the US-Iran conflict. India also announced the launch of the India-USA Trade Facilitation Portal to boost ties between the countries.

+ The government announced relief measures for domestic airlines, including a 25% cut in landing and parking charges for three months to reduce operational costs amid global disruptions.

+ India’s forex reserves rose by $9.06 billion to $697.12 billion in the week that ended on 3 April.

The information contained in this Groww Digest is purely for knowledge. This Groww Digest does not contain any recommendations or advice.

Team Groww Digest