For most investors, risk is a factor that always lies at the back of their mind.

The possibility that an investment won’t perform as expected, or worse, that it loses value is difficult to ignore.

No one wants to make the wrong decision. No one wants to watch a single sector or company decline sharply and drag their entire portfolio down with it.

This is where diversification comes in.

To manage risk, money is spread across different assets and categories such as stocks, debt, commodities, etc.

The idea is simple: different assets are expected to behave differently, different sectors behave differently, and even similar assets can behave differently.

When one struggles, another may hold steady or perform better. Together, they are meant to reduce the impact of any single poor outcome.

To reduce risk, diversification is important.

But as portfolios become more diversified, a different question starts to emerge.

Is there such a thing as too much diversification? Can it make your portfolio redundant?

Is there a point where it stops adding safety and only increases the number of moving parts in a portfolio?

To explore this, we tried to understand how diversification affected a portfolio by looking at 8 mutual funds over a 10-year period.

The Experiment

We looked at the historical NAV data of the following mutual funds (all Growth, Direct) for the last 10 years. The selection was intentionally diversified across fund types and AMCs to avoid concentration within a single category or style.

UTI Nifty 50 Index Fund(G)-Direct Plan

ICICI Pru Large Cap Fund(G)-Direct Plan

Parag Parikh Flexi Cap Fund(G)-Direct Plan

HDFC Mid Cap Fund (G) Direct Plan

Mirae Asset ELSS Tax Saver Fund(G)-Direct Plan

Nippon India Small Cap Fund(B)-Direct Plan

SBI Magnum Gilt Fund- Direct Growth

Kotak Gold Fund-Direct Growth

The goal was to see how the same amount of Rs 1 lakh would behave over the period from 2016 to 2026 when managed under different portfolios.

The experiment was structured in three parts: returns from each mutual fund individually, a fully diversified portfolio where the Rs 1 lakh was split equally across all 8 funds and a comparison with alternative outcomes.

Results

Individual Returns

Looking at each fund in isolation, the differences in outcomes are significant.

Over the 10-year period, returns ranged from around Rs 2.1 lakh at the lower end to over Rs 7.1 lakh at the higher end for the same investment.

Unsurprisingly, equity-heavy funds, particularly the small- and mid-cap funds, gave the highest returns, while the debt fund gave the lowest.

Granted, their goals are different, one is for rapid compounding, which comes with higher risk, and the other is for stability and safety.

Which is why holding just one fund, or only one type of fund, may not be the most efficient way to invest.

Diversified Portfolio

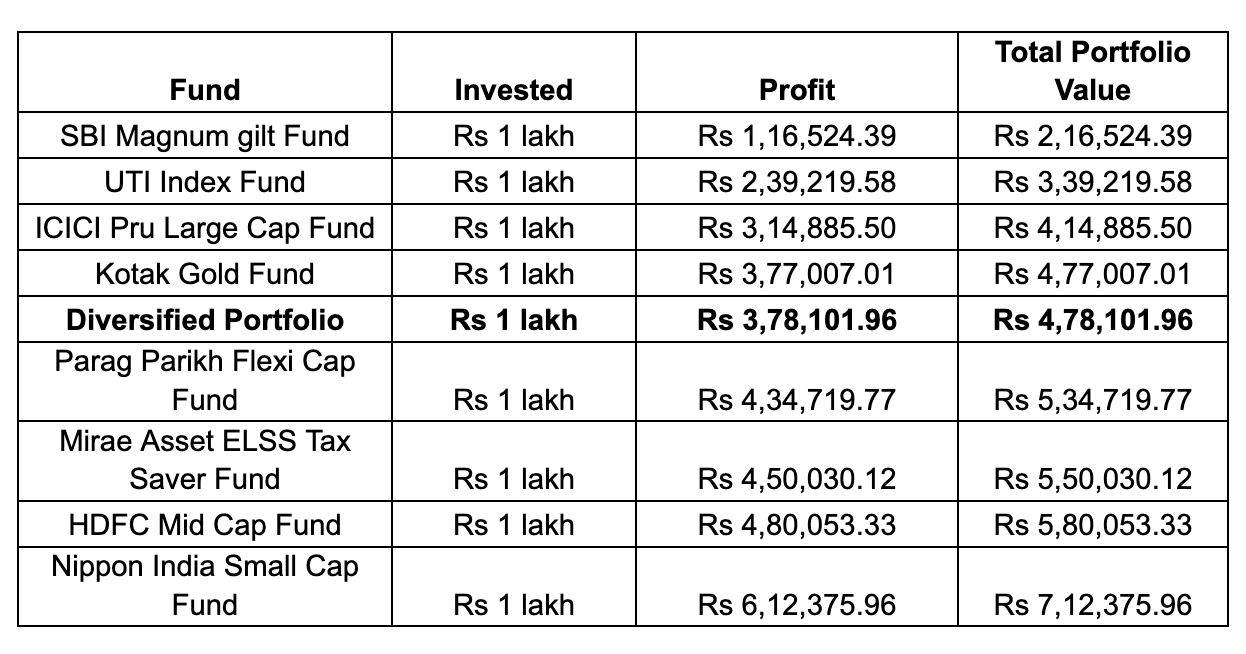

Now, we look at a portfolio with all 8 mutual funds. The Rs 1 lakh is divided equally between the funds, Rs 12,500 in each fund.

Remember, diversification can be done in different ways. This is our interpretation and to make matters simple.

Here is how the portfolio looks at the end of 10 years.

Amount invested: Rs 1 lakh (Rs 12,500 per fund) lumpsum

Total Portfolio Value: Rs 4.78 lakh

Profit: Rs 3.78 lakh

Compared to the individual funds, the diversified portfolio sat exactly in the middle in terms of returns.

It delivered better performance than gold and debt funds and also outperformed the index fund and large-cap fund in isolation.

At the same time, it lagged behind the other equity funds.

In this portfolio too, the small-cap, mid-cap, ELSS fund and the flexi-cap fund pulled the most weight by having the most share in profits.

The other 4 funds, while giving not as many returns, kept the portfolio safe and stable.

In simple terms, diversification smoothed the extremes. It avoided the weakest outcomes but also diluted exposure and consequently risk to the strongest ones.

Alternate Options

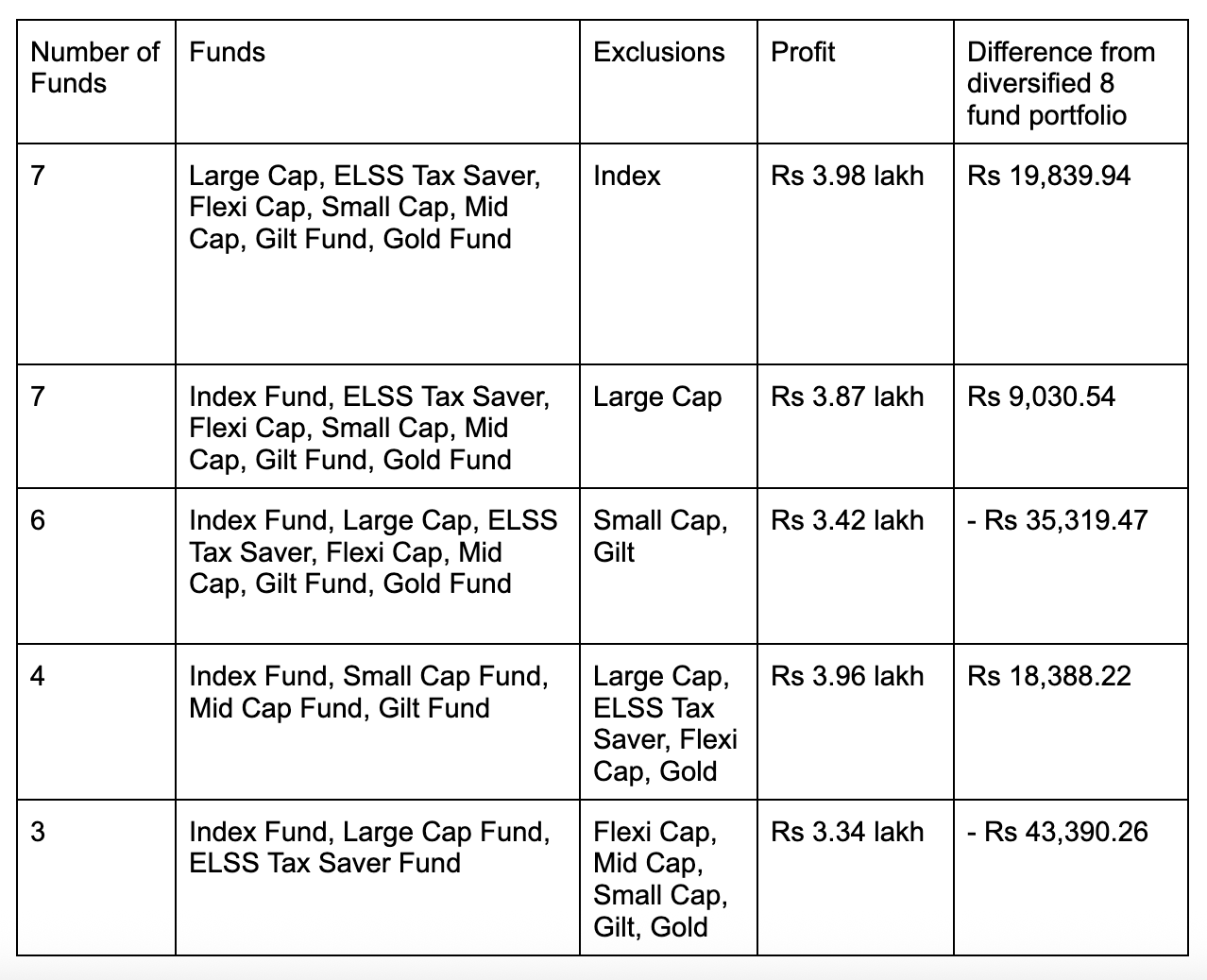

The next question we asked is what happens when the structure of diversification is changed.

The idea was simple: if too many funds can dilute returns, then a smaller set should consistently perform better than a fully diversified portfolio

The question explored was whether a smaller combination of funds (fewer than 8) could have delivered different outcomes compared to a fully diversified portfolio.

To test this, multiple combinations were created by gradually reducing the number of funds while keeping allocations equal.

(Note: These variations are not meant to suggest better or worse approaches. They are simply different ways of observing the same idea from different angles).

What was observed was that the outcomes did not follow a linear pattern.

Here are some examples:

In some combinations, removing lower-returning or defensive assets such as debt or index exposure slightly improved returns. In others, the same removal led to weaker performance.

Even the all-equity fund of 3 conservative funds could not beat the diversified portfolio.

Other than the portfolios with both small-cap and mid-cap funds and higher weightage (which increases risk), no other single configuration consistently outperformed the fully diversified portfolio. Their returns were higher, but that also means they were more susceptible to volatility.

Overlapping funds (funds with similar composition) did not seem to add value. Whether this is a structural truth or specific to the funds chosen in this dataset is something that would need further testing.

This leads to one clear observation: The outcome of diversification is not determined by the number of funds alone, but by the composition of those funds.

Conclusion

It ultimately comes down to one simple fact. There is no single right way to invest.

Risk appetite differs from investor to investor, and even for the same investor, it can change over time depending on goals, market conditions, and experience.

What this experiment highlights is a set of patterns rather than fixed rules.

Reducing diversification does not automatically improve returns.

In fact, certain combinations (such as when large-cap, index, and ELSS funds were grouped together) showed that maintaining similar risk exposure (all equity) while reducing the number of funds did not necessarily lead to better outcomes.

At the same time, increasing diversification does not automatically reduce returns either.

However, diversification without structure or awareness of overlap can dilute performance without meaningfully improving stability.

The bottom line is diversification is not a bad strategy. It keeps the investor safe. But depending on how it is constructed, it may not always be the most effective way to push returns beyond a certain threshold if that’s what the aim is.

Limitations of the Experiment

Fixed time period: The analysis is based on a single 10-year window (2016–2026). Different market cycles could produce different outcomes.

Limited fund universe: Only 8 mutual funds were selected. Results may vary with a different set of funds within the same categories.

Equal allocation assumption: Each fund was given the same weight. In reality, investors often adjust allocations based on risk appetite, performance, or market conditions.

No cost adjustments: Taxes, expense ratios over time, and transaction costs were not factored into the calculations, which can impact real-world returns.

Return-focused analysis: The study focuses primarily on returns. Risk-adjusted measures like volatility, drawdowns, or Sharpe ratios were not explicitly evaluated.

Simplified portfolio behaviour: The experiment does not account for investor actions such as rebalancing, entry/exit timing, or behavioural decisions.

Wonderful analysis thanks.