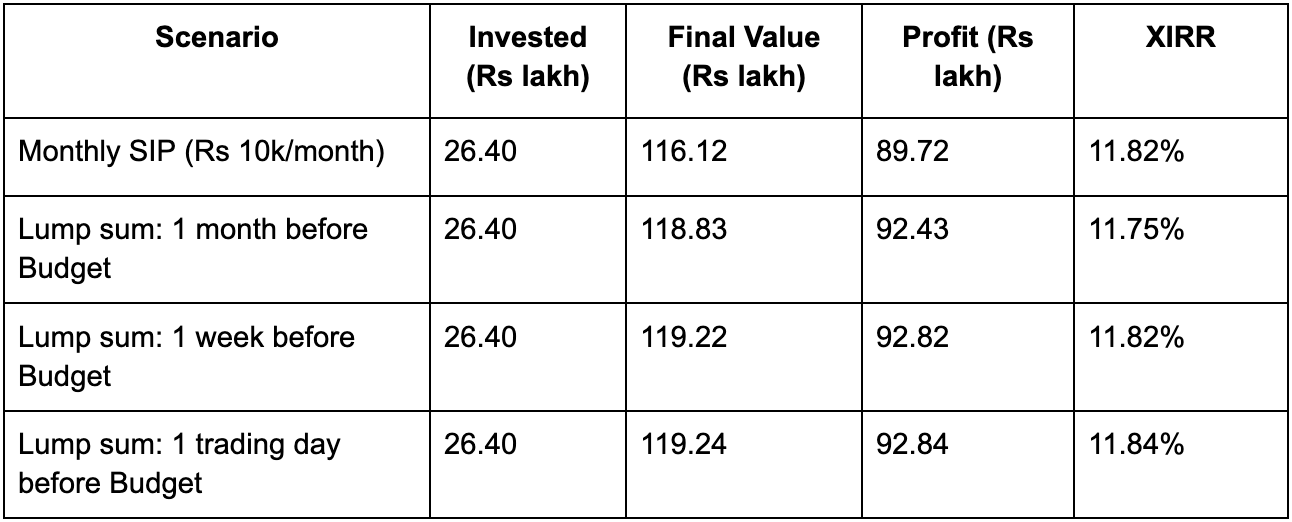

What if I invested just before the Union Budget is announced? Does investing only in high volatility market (VIX>20) help?

Whenever there is any major event coming up, which is very crucial for the overall economy, we wonder if it makes sense to take a chance at the stock markets just before the event takes place.

Events like general elections, a giant merger, the Union Budget announcement, Trump’s tariffs, an unscheduled speech from the Prime Minister, companies’ quarterly results, etc trigger big changes in the stock markets.

This is because such events have a direct impact on the functioning of the ease-of-doing businesses in the economy. When the result of such events is favourable, businesses thrive. And that might lead to higher earnings, which leads to higher shareholder value, which leads to wealth creation for both retail and institutional investors.

This triggers an instinct or thought that if only we had invested before the results at cheaper prices, we would be reaping the benefits.

And it raises a crucial problem: maybe SIPs are not the way to go; maybe a lump-sum investment (if you can) is the way to make wealth fast in the long-term.

We also scratched our heads wondering what the actual data would saysays, and whether we can settle this problem with evidence., and not just theory.

Now to do thisit, we picked the most recent major event that happened just yesterday (12 Feb).

The Union Budget 2026 was presented.

And to study if investing before budget announcements every year, we took a long period of time as reference: 2004 to 2025.

But how do you quantify the “just before this...” period?

We took 3 approaches where one invests a lump-sum amount:,

A day before the budget announcement (immediate previous trading day)

A week before the budget announcement (tradeable days)

A month before the budget announcement

And to compare these strategies, we also took a case where one invests through regular monthly SIPs in the 2004 to 2025 period.

We anchored all our investments in one of the long-standing index funds that tracks the Nifty 50: SBI Nifty 50 Index Fund.

A couple of pointers to not here:

For simplicity, we kept each month’s SIP amount to be Rs 10,000.

With that, our lump-sum for each year came out to be Rs 1.2 lakh (Rs 10,000 per month x 12 months)

For this study, we used the actual dates on which the Union Budget was announced, instead of assuming that it always happens on 1 Feb.

This is because the budget date has changed over time, and in some election years the main (full) budget was presented later in the year, while the February presentation was only an interim one.

For example, in 2014 and 2019, an interim budget was presented in Feb, but the full budget that markets focused on came later, in July.

There has also been a structural change in recent years: before 2017, budgets were usually presented at the end of February, whereas from 2017 onwards, the budget has been announced on 1 Feb.

By using the real announcement dates for each year, the “1 month, 1 week, or 1 day before the budget” investment timings always align with the actual event investors were reacting to, making the analysis more realistic and easier to interpret.

Here are the results of the simulation we ran:

Final results (as of 22 Jan 2026)

On the first look at the results, it seems that investing once a year around the Budget did slightly better than a regular monthly SIP, but the difference was small.

Over more than 20 years, the extra gain was only about Rs 2.7 lakh to Rs 3.1 lakh on a total investment of Rs 26.4 lakh.

Now before we talk about the reason behind these results, let us look at the Budget-based strategies:

Among the Budget-based strategies, investing just one trading day before the Budget gave the highest final value. However, it beat investing one week before by only about Rs 2,200 over 22 years, which is practically negligible.

The annual return (XIRR) across all strategies including SIPs, one month before, one week before, or one day before the Budget, was almost the same. The difference was less than 0.1% per year, which is too small to matter in real life.

This means that timing investments very close to the Budget does not meaningfully improve long-term returns.

And even if it did in “week-before” and “day-before” cases, most of the small advantage seen comes from investing a full year’s money at once (annual lump sum) rather than spreading it out monthly.

The difference in returns is not from the Budget event itself. Because if there was a substantial effect of the event, it would show itself through a higher difference.

Looks like SIPs are indeed the way to go without breaking your bank balance!

But if you have the money, do a lump-sum. It will give more room for it to compound because of the time advantage.

Take time, perform due diligence and decide the route you want to take.

Stock markets can seem a potentially high-return asset during times of high volatility.

Just like we saw with the Union Budget experiment.

But even then, the experiment was single event-based. And there is another interesting question that we ask ourselves.

And this question was asked by many of you after our last “What if?” study on Nifty VIX.

What if you only invest during times of high volatility?

How does it compare with the study we did on stable (or low volatility) markets?

Let me frame this question more technically:

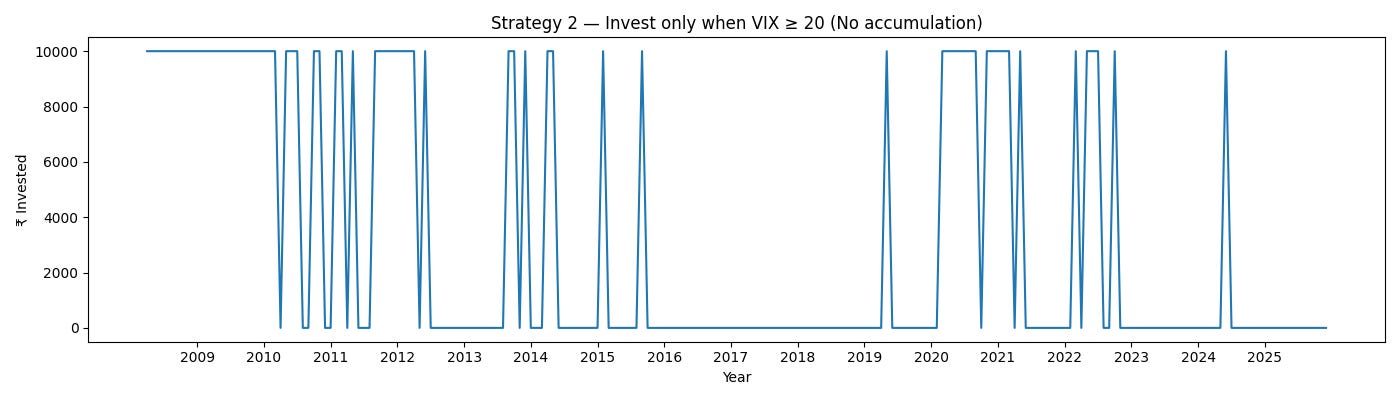

“What if you only invest when VIX is above 20?”

To understand this, we took a time period: April 2008 to December 2025

- Total SIP months: 213 months

- Total trading days: 4,351 days

- High-fear trading days (VIX ≥ 20): 1,468 days

So roughly one-third of the market’s life was spent in a high-volatility state (VIX ≥ 20)

Strategy 1 — Regular SIP (Ignore fear)

The investor invested Rs 10,000 every month for 213 months, without reacting to volatility. Money entered the market during calm phases, crisis phases, and recoveries.

Because investing never stopped, the investor kept buying units at all kinds of prices.

This strategy produced the highest absolute wealth because it maximised time in the market, not because it avoided risk. Volatility hurt temporarily, but compounding had enough time to overpower it.

Strategy 2 — Invest only when VIX ≥ 20

The investor invested only during fear. Over 17 years, this meant investing in just 68 out of 213 months. In the remaining months, no money entered the market at all.

Here, the investor participated in only 34% of trading days. Missed long recovery phases, Looks brilliant in % terms, But never allowed capital to grow meaningfully.

As you can see, the investor who invested only when VIX was above 20 earned a higher percentage return.

Why did this happen?

In the high-volatility strategy, money entered the market mostly during fearful periods, when prices were lower. This allows the investor to buy at lower prices. When volatility later cools down and VIX drops, markets tend to recover. So, on paper, this strategy looks smart. It appears as if the investor is consistently buying low and benefiting when prices rise.

But percentage returns do not show the full picture.

The important thing to look at is how much money actually got invested. By investing only during high-VIX periods, the investor was in the market for only about 35% of the total time. Even though the returns during those periods were high, most of the money stayed outside the market for long stretches. That left very little time for the investment to grow into meaningful wealth.

The investor who ignored fear and invested regularly stayed invested through every fall and every recovery. Money went into the market even when prices were down. Over many years, this steady approach helped build the highest long-term wealth.

The investor who invested only during fear looked cautious and disciplined. But by staying out of the market most of the time, the growth opportunity was limited. The returns looked impressive in percentage terms, but the actual wealth created was much lower.

One clear pattern emerges.

The more an investor reacted to fear, the weaker the long-term result became.

I see usual discussions around the theme before budget.I mean to say folks are not interested in the whole market but few themes like railway,defense etc how that would that change in returns just curious

While comparing with SIP, you have to make same parameter like the monthly accumulated money in the period VIX below 20, shall invest in the first month in which vix crosses 20