Everyone loves the idea of doing something smarter with their money.

But what if the smartest move is actually to keep things simple?

We asked a simple question: how much of a difference would it make if you increase your investments a little every year, instead of keeping them constant?

Most SIP calculators assume one thing: you invest the same amount every month, year after year.

But real life rarely works that way. Salaries rise, an occasional bonus comes in, and over time, people gradually gain confidence and commit more money to investing.

So the question is: does stepping up your SIP every year actually make a meaningful difference to your money?

To find out, we ran a simple experiment.

The Experiment

We used historical data from the UTI Nifty Index Fund and simulated SIP investing over a 10-year period.

We chose an index fund because it keeps things simple. There’s no fund manager skill, no sector bets, and no style bias. The performance reflects the market benchmark — the Nifty 50.

This allows us to isolate the impact of the investor’s behaviour, without other factors influencing the results.

But it’s important to note that an index fund is not a perfect mirror of all investing scenarios. It does not capture individual fund strategies that active funds might employ. We took it as a neutral baseline to study the effect of our experiment.

We compared four strategies over 10 years:

Normal SIP: Flat Rs 10,000/month each year

5% Annual Step-Up: Increase SIP amount by 5% each year

7.5% Annual Step-Up: Increase SIP amount by 7.5% each year

10% Annual Step-Up: Increase SIP amount by 10% each year

Everything else remained the same. The same fund and same time period.

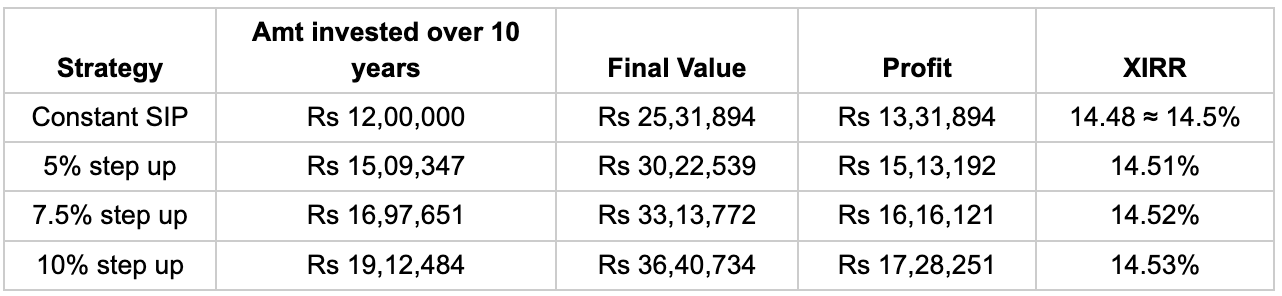

Results: 10 year investments

What Happened Over 10 Years

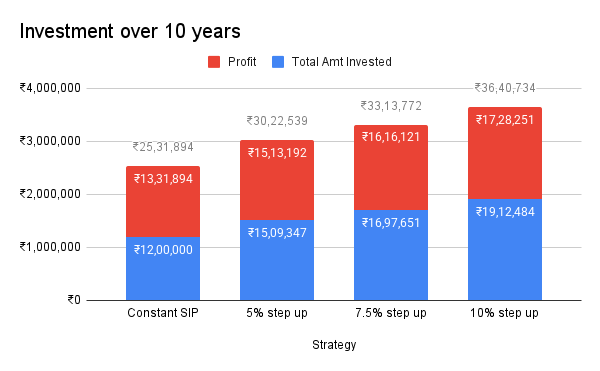

With a normal SIP, the investor put in Rs 12 lakh over 10 years. That grew to Rs 25.3 lakh, generating a profit of Rs 13.3 lakh. This alone highlights the power of consistency and staying invested.

Higher step-ups led to a larger portfolio value. Even the modest 5% annual step-up made a noticeable difference. The final value was almost Rs 5 lakh higher than the constant SIP. The absolute profit made was higher too, though not significantly.

But here’s the key: step-ups did not increase percentage returns.

The takeaway is clear: higher step-ups lead to a larger final corpus, not necessarily higher percentage returns.

The difference in wealth comes simply from investing more money over time. Early contributions get more time to compound, while later step-ups still add meaningful gains

The 10-year results show how step-ups can significantly increase your final wealth over a long horizon. But what if you’re a new investor, or you’re looking at a shorter time frame?

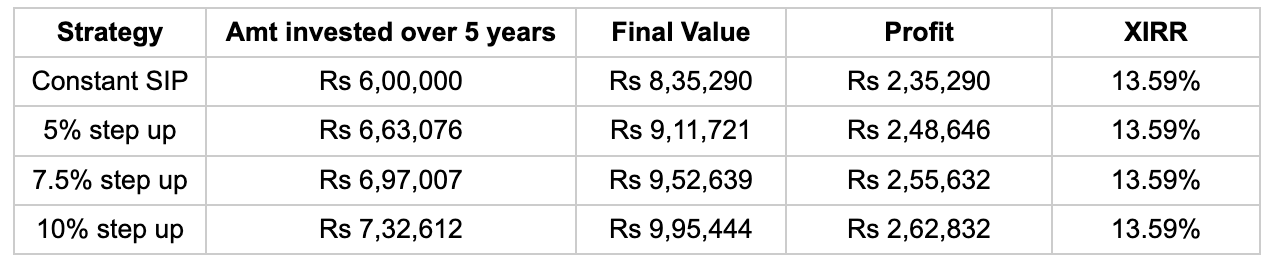

How much difference does a step-up SIP make over 5 years instead of 10?

5 year investments

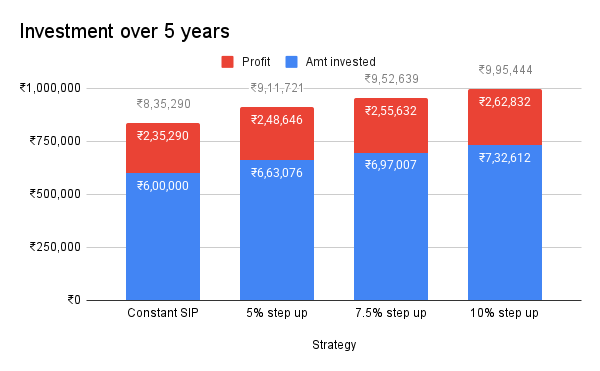

Even over 5 years, step-ups create a noticeable difference in absolute wealth. The higher the step-up, the more money you put to work, resulting in a slightly larger portfolio.

But just like in the 10-year scenario, percentage returns remain more or less similar across all strategies.

The shorter horizon means later step-ups have had less time to compound, so the absolute advantage is smaller than over a decade.

The Takeaway

Stepping up your SIP is not a shortcut to higher percentage returns. What it does is increase the total money you put to work over time, giving compounding more material to generate wealth.

Since you cannot go back in time to start investing earlier, the only way to reach your goals faster is to invest more today and increase contributions as your capacity to invest grows.

This experiment confirms this. A 10% annual step-up over 10 years resulted in a final portfolio nearly 44% larger than a constant SIP. And for a time period larger than 10 years, the difference would be even higher.

The extra wealth didn’t come from better fund selection or market timing. It came from the discipline of investing more as the investment capacity grew.

Also, stepping up also helps protect your investments against inflation. A Rupee today is worth more than a Rupee 10 years from now, so gradually increasing your SIP preserves the real value of your investments.

In the end, any investment is better than no investment.

But if we are talking about smarter investing, a disciplined, step-up SIP can turn consistency into meaningful wealth over time.

Limitations of the Experiment

Historical Data Bias: The experiment uses past performance of the UTI Nifty Index Fund which is no guarantee of future returns.

Fund Limitation: The results are specific to the Nifty 50 and do not reflect mid-cap, small-cap, or active fund volatility and returns.

Perfect Discipline: Assumes zero missed SIPs, no emergency withdrawals, and full patience during market ups and downs.

Costs & Taxes: Exit loads, changing expense ratios, and other taxes are not taken into consideration here.

Market Timing: Returns could change depending on when bull or bear markets occur and on the time period.