What if I stop investing in bad markets and restart when things improve — will my returns be better?

Let us break down the problem into smaller parts to understand it better.

The problem can be divided into 2 cases:

You are just pausing your SIP and not withdrawing the invested amount — you will resume the SIP at a later stage.

You are stopping/cancelling the SIP by withdrawing the investment amount — you will start a new SIP at a later stage.

What exactly tells us that the current market is ‘good’ or ‘bad’?

It is very subjective. Some might think that a fall of 5% in a month is a bad market period, while others might say that a fall of 12% in 3 months is bad.

The fall % and the time period considered for the fall can be different for different investors.

Even if you somehow answer this question by taking a standard, you have to decide the day/week on which you will pause your SIP — which is again subjective.

So if we broadly think about it, this ‘decision’ to pause/stop SIP and when to start heavily depends on the type of investor you are.

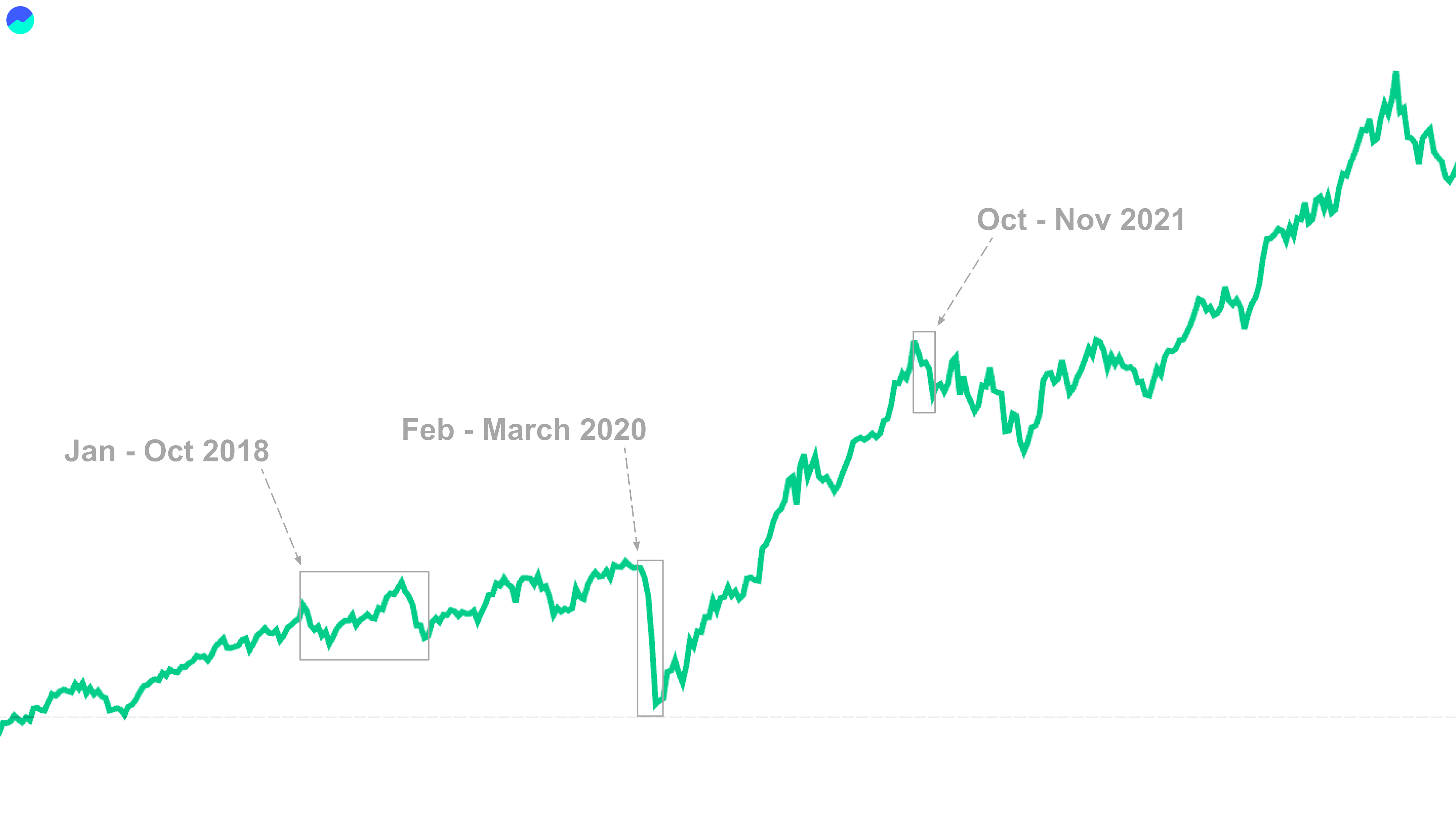

If we look at the past 10-year movement of Nifty 50 (i.e. from 1 Sept 2015 to 1 Sept 2025), there are a lot of rises and falls.

For example,

when the Covid-19 outbreak happened, Nifty 50 fell over 30% in just 2 months — Feb to March in 2020.

In 2021, when markets were trying to recover on a broader scale, it fell over 8% during Oct-Nov.

Before Covid-19, the markets fell over 8% during Jan-Oct 2018. But it also fell over 13% in just Sept-Oct 2018.

The point is that it is difficult to quantify what actually is a ‘bad’ market.

To give you a recent example, take a look at the period between the later half of 2024 and the first half of 2025.

Nifty 50 fell over 8% in Sept-Nov 2024 period.

But if you had thought to invest a lump sum in Nov 2024, you would see an overall fall of over 14% from Sept 2024 to March 2025.

See the challenge?

And the same goes for deciding what is a ‘good market’.

The right time to resume/start the SIP during the market rises is also subjective.

Capturing the ‘trend’

Now let’s say you take a chance to time the markets.

You try to decide when the exact day to pause your SIP during bad market conditions.

Let’s say you are in the beginning of Jan 2025 and somehow manage to correctly predict that the market is going to go further down in the month. And let’s assume that you pause your SIP somewhere in the middle till the end of the month.

Now say that you see that the market starts to recover during the starting days of February and you resume your SIP in the between 27 Jan to 4 Feb (see below).

But shortly after you had resumed the SIP, the markets started falling heavily till 4 March (see below).

Now because of your careful watch, you managed to dodge a falling period but as soon as you resumed investing during a market rise, the markets again fell, resulting in even bigger losses because you bought the MF units at rising prices or NAV.

This kind of a situation happens all the time in the stock markets. Even if you pay attention to all the news and trends surrounding the market, it is still very difficult to judge how the larger investor base will react to those developments.

Hence, even if you succeed a couple of times, the chances of experiencing a heavy loss due to buying at peak will still be high.

Unless you are a very skilled trader or investor who has spent a substantial period of their life studying all about stock markets, the success rate for you correctly predicting a market trend would be less than 10% (which is also generous to say).

Hindsight Bias

Now this is all readily available information on the internet. There are countless articles, research papers, interviews, etc out there on ‘timing the market’.

So why do investors still feel that they can avoid the dips and benefit from the rises?

This is because of a very fundamental psychological concept known as the ‘hindsight bias’.

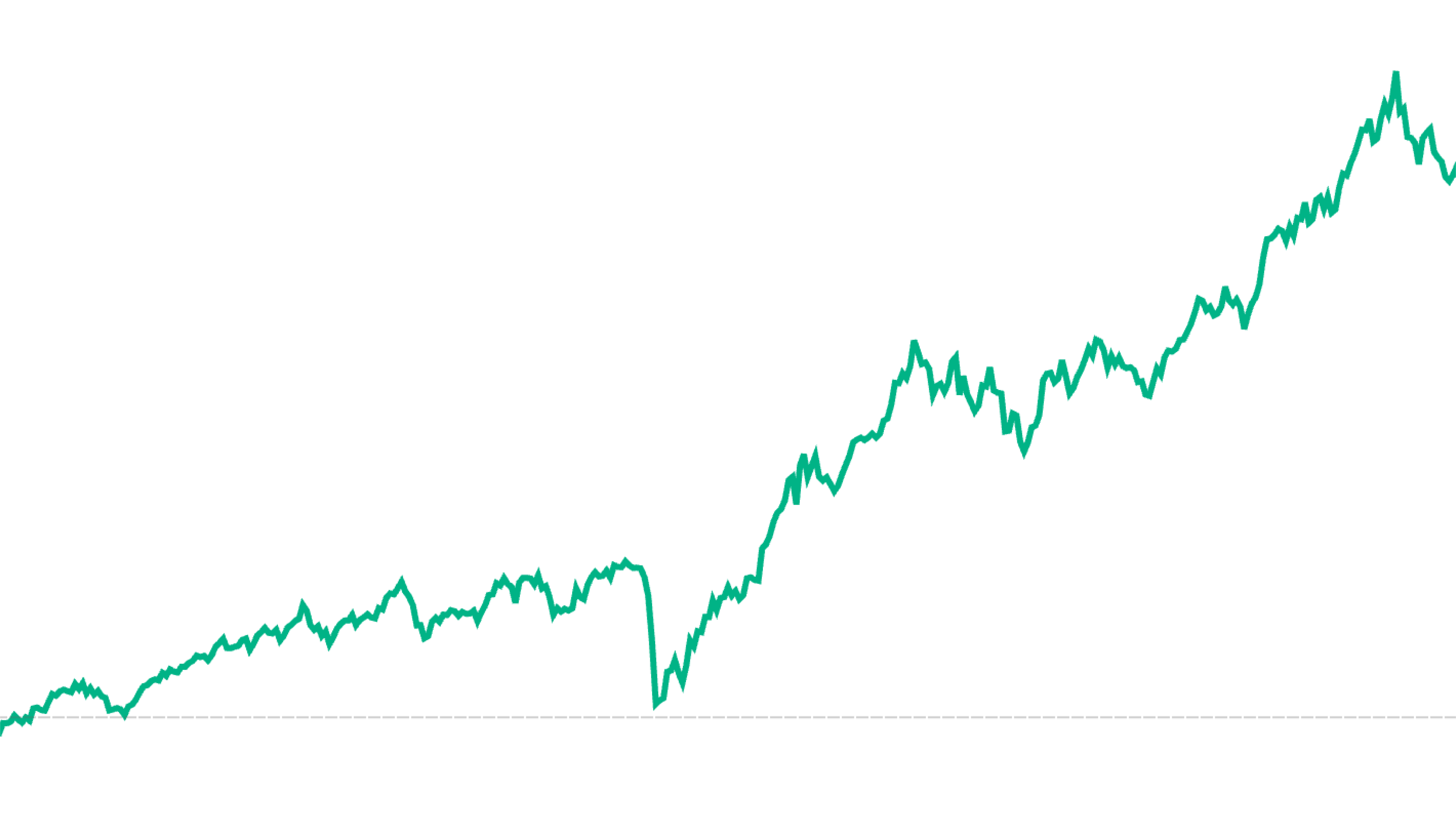

Look at the chart below showing Nifty 50 movement from Sept 2015 to Sept 2025:

By seeing this, you might think that “Oh, I can look at this or even more historical data on all ups and downs, and then extrapolate that for the upcoming year.”

Many investors have tried doing so in the past and have failed miserably as the markets are changing every year.

Who predicted that Covid-19 would happen?

Who predicted that the US would suddenly put sanctions on Indian imports when it was initially not-so-hostile in this tariff war?

Who predicted that X company will post losses because of a very distant issue in the global supply chain?

So, it is said that when we have an abundance of historical information about an event (and it can be anything), we tend to be confident that we will be able to ‘predict’ that specific event the next time it happens.

And this confidence may not turn out to be ‘true’ in the future. Life is filled with unknowns and uncertainties. The same thing applies to the stock markets, even more so than other fields.

This high uncertainty is due to factors like:

People or humans — unpredictable.

Global natural events — unpredictable.

Man-made events — unpredictable.

Country-wide economical and political shifts — unpredictable.

And much more.

Taxation

Remember the 2 cases of pausing or cancelling the SIP that we talked about in the beginning of this article?

For the sake of the argument, let’s say that you somehow manage to successfully time the market and avoid periods of losses or market falls.

Now if you are cancelling or stopping the SIP and withdrawing your invested money, to invest during the market rises, you might lose a lot to taxes.

There is rarely a case where markets continuously fall in the entire year, unless something like COVID happens.

Let’s say you start investing today and after 3 months, you see a period of fall and you withdraw your money.

At this point, you will attract a tax of 20%.

This is known as STCG tax or Short Term Capital Gains Tax, which is tax applicable on your profits when you withdraw your investment before a period of 12 months.

Now this can happen a few more times in a year where you time the market and keep withdrawing and reinvesting. This can lead to a higher tax liability which can reduce your effective profits.

Now if you manage to stay invested over a period of 12 months and then withdraw during a market fall, it still attracts a 12.5% tax which is known as LTCG tax, or Long Term Capital Gains Tax.

The caveat here is that LTCG tax is only applicable if your total profit is more than Rs 1.25 lakhs.

The lesson here is that you have to pay more tax (STCG) if you keep withdrawing time and again in a year only due to temporary falls.

Missed Opportunities

One of the biggest drawbacks of stopping or canceling your SIP during market falls is that you miss the opportunity to accumulate more units at lower prices.

SIPs are designed to work on the principle of averaging the buying cost — you buy more units when the market is down and fewer when it is high, which averages out your overall buying cost over time.

By skipping investments during a market fall, you are essentially giving up the chance to lower your average buying cost.

Let’s take a simple example. Suppose you are investing Rs 10,000 every month in a mutual fund.

In Month 1, the NAV is Rs 100 — you buy 100 units.

In Month 2, the NAV falls to Rs 80 — you buy 125 units.

In Month 3, the NAV recovers to Rs 120 — you buy 83.3 units.

If you stayed invested, by the end of 3 months you would hold 308.3 units of that mutual fund at an average cost of approx Rs 97 per unit.

But if you paused your SIP in Month 2 (thinking the market is ‘bad’) and resumed only in Month 3:

Month 1: 100 units

Month 2: 0 units (skipped)

Month 3: 83.3 units

Now you only have 183.3 units at an average cost of approx Rs 109 per unit.

This shows that missing even a single low-cost buying opportunity not only reduces the number of units you accumulate but also raises your overall cost of investment.

The thing to note here: you might wonder if stopping your investments in a down market frees up cash to "time the market" later, potentially earning better returns.

However, as we discussed earlier, timing the market is rarely successful, and your capital is precious.

So, the real question is, "Should I continue my current SIP investments, or should I attempt the complex technical analysis required to successfully time the markets later?"

Over years, such missed opportunities can create a huge gap in wealth creation. compared to someone who stayed disciplined with their SIPs.

Very informative