In the late 1990s, a strange technology problem created one of the biggest turning points for India’s IT industry.

The problem was called Y2K.

Many old computer systems had stored years using only two digits. So 1998 was stored as 98, 1999 as 99, and the fear was that when the year changed to 2000, some systems might read 00 as 1900 instead of 2000.

For banks, airlines, governments and large companies, that was not a small software bug. It could affect payments, records, bookings and critical business systems.

Companies around the world suddenly needed programmers who could inspect old code, fix systems and make sure nothing broke when the calendar moved to 1 January 2000.

This became a huge opportunity for Indian IT companies.

Basically, Indian firms had the engineers and global companies had the problem.

These global clients paid Indian IT companies in US dollars. At the same time, Indian IT companies built large development centres in India, where much of the work could be done at a lower cost.

This created the business model that companies like Infosys, TCS, Wipro and HCLTech still follow today. They earn a large part of their revenue from clients in the US, Europe and other overseas markets, while many employee salaries and other operating costs are paid in rupees in India.

And this is where the weak-rupee story comes from.

Indian IT is one of India’s most export-driven industries. According to RBI’s software-services export survey, India’s software-services exports were estimated at $204.7 billion in 2024-25, up 7.3% from the previous year. The survey covered companies that together represented around 90% of India’s total software-services exports, so the data gives a broad view of the industry and is not based on a small sample.

The dollar link is also real. In 2024-25, the US was still the largest destination for India’s software exports, with a 52.9% share, and the US dollar was the main invoicing currency, making up 72% of India’s software exports.

So when people say Indian IT earns in dollars, they are not wrong.

A large part of the industry’s revenue comes from overseas clients. A large part of that is invoiced in dollars. And these companies finally report their financial results in Indian rupees.

That creates a simple accounting effect.

Imagine an Indian IT company earns $1 million from a client in the US.

If the exchange rate is Rs 70 per dollar, that revenue is worth Rs 7 crore.

But if the rupee weakens and the exchange rate moves to Rs 80 per dollar, the same $1 million is now worth Rs 8 crore.

Nothing has changed for the client.

They are still paying $1 million.

The company has not won a new contract. It has not done any extra work either. The only thing that has changed is the exchange rate.

But because the rupee has weakened, the same dollar revenue becomes more valuable in rupee terms. That is why investors often believe a weaker rupee benefits Indian IT companies.

This is where the business story turns into an investing belief: if the rupee weakens, IT stocks should benefit too.

The logic is not wrong. A weaker rupee can help Indian IT companies because dollar revenue converts into more rupees.

But the investing question is not whether the dollar matters to Indian IT companies.

It clearly does.

The question is whether this relationship was useful for investors.

If the rupee weakened and an investor bought IT stocks because of that, did it actually work?

We decided to test it.

What we did…

For this study, we used daily data from 1 January 2010 to 2 July 2026.

We used three series:

- USD/INR

- Nifty IT TRI

- Nifty 50 TRI

USD/INR tells us how the rupee moved against the dollar. If USD/INR rises, it means one dollar costs more rupees. So the rupee has weakened. If USD/INR falls, it means one dollar costs fewer rupees. So the rupee has strengthened.

Nifty IT TRI was used to represent the Indian IT sector. Nifty 50 TRI was used as the broader market benchmark.

This benchmark is important.

If Nifty IT rises by 8%, that sounds good. But if Nifty 50 rises by 15% in the same period, then IT did not really do well compared to the market. It went up, but it still lagged.

So we checked two things:

1. Did Nifty IT rise during rupee moves?

2. Did Nifty IT beat Nifty 50 during those same moves?

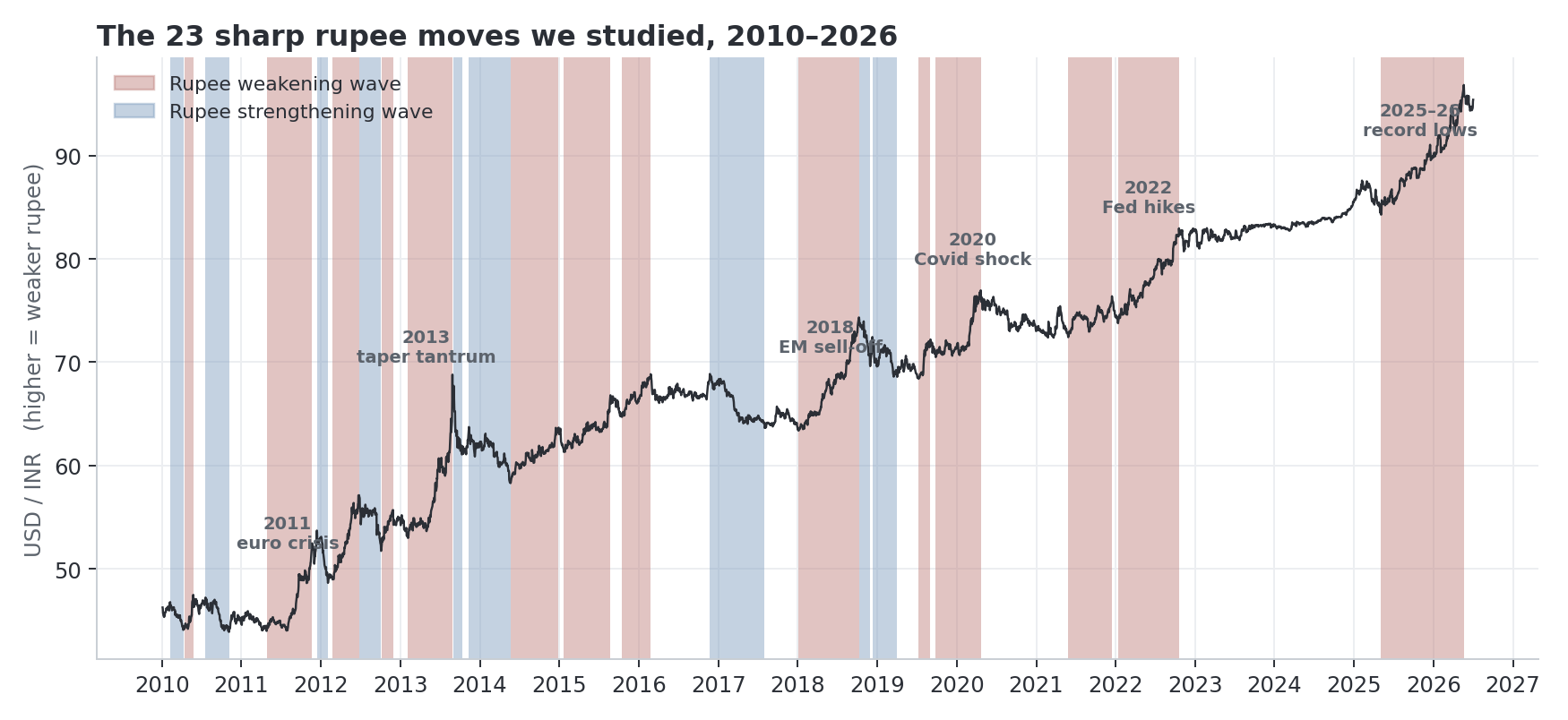

Now, we first identified every major period when the rupee either weakened or strengthened against the US dollar.

A rupee-weakening wave is a period when the USD/INR exchange rate rises from a low point to a later high point. A rupee-strengthening wave is the opposite; it is a period when the USD/INR exchange rate falls from a high point to a later low point.

We didn’t want to count every small day-to-day fluctuation as a meaningful currency move. So we only considered moves that met a few conditions.

A wave had to:

- move at least 5% in USD/INR

- last at least 30 calendar days

- end after a 3% reversal or a long stall, meaning the exchange rate stopped making fresh highs or lows for around 90 days

- avoid very slow multi-year drifts, which were separated from sharp visible moves

This gave us the set of moves investors would actually notice on a chart.

Visual: USD/INR daily waves used in the study. Red areas are weakening waves; blue areas are strengthening waves.

When did the rupee make its biggest moves?

Using this method, we found 23 sharp USD/INR waves.

Out of these:

- 14 were rupee-weakening waves

- 9 were rupee-strengthening waves

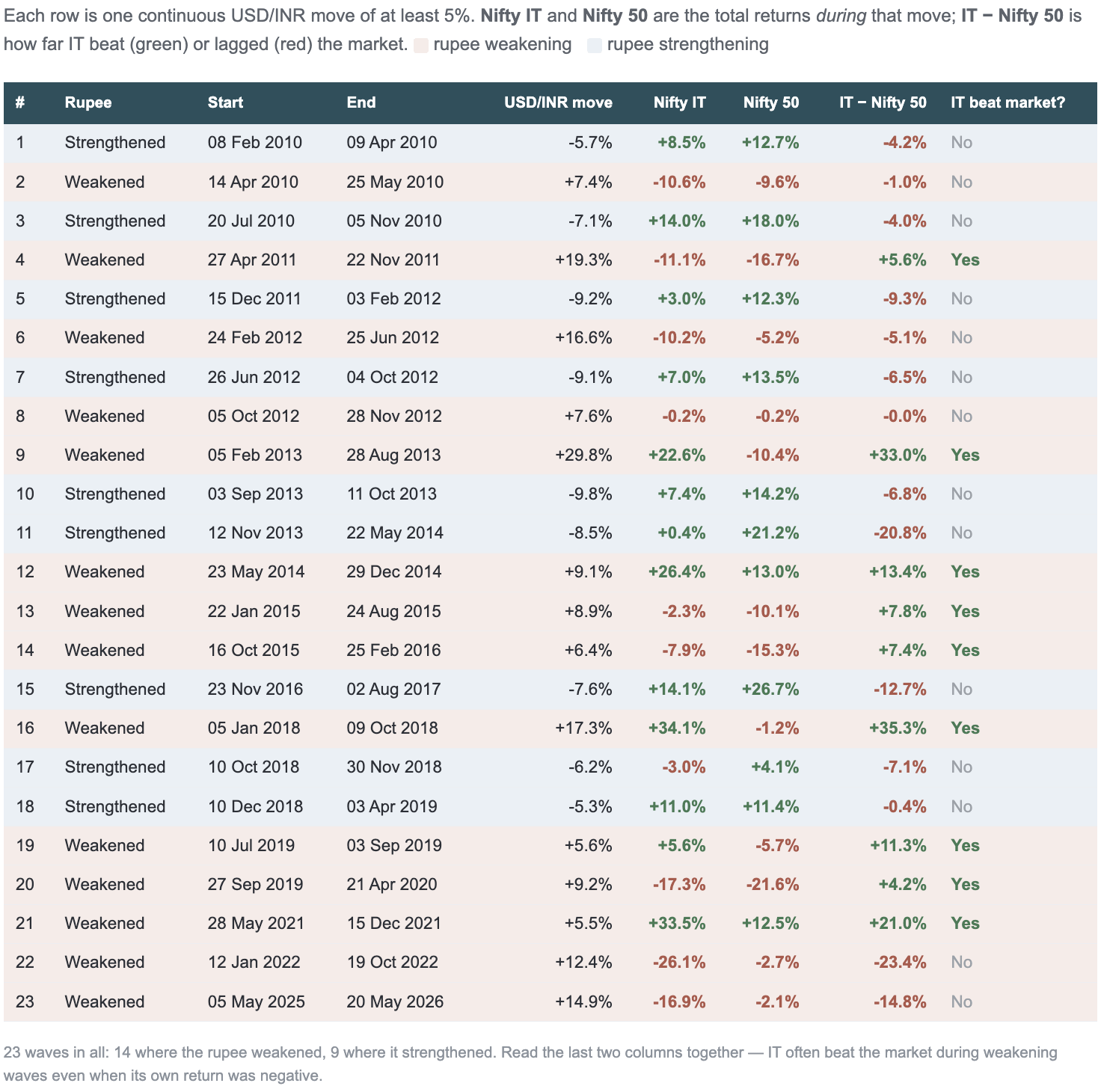

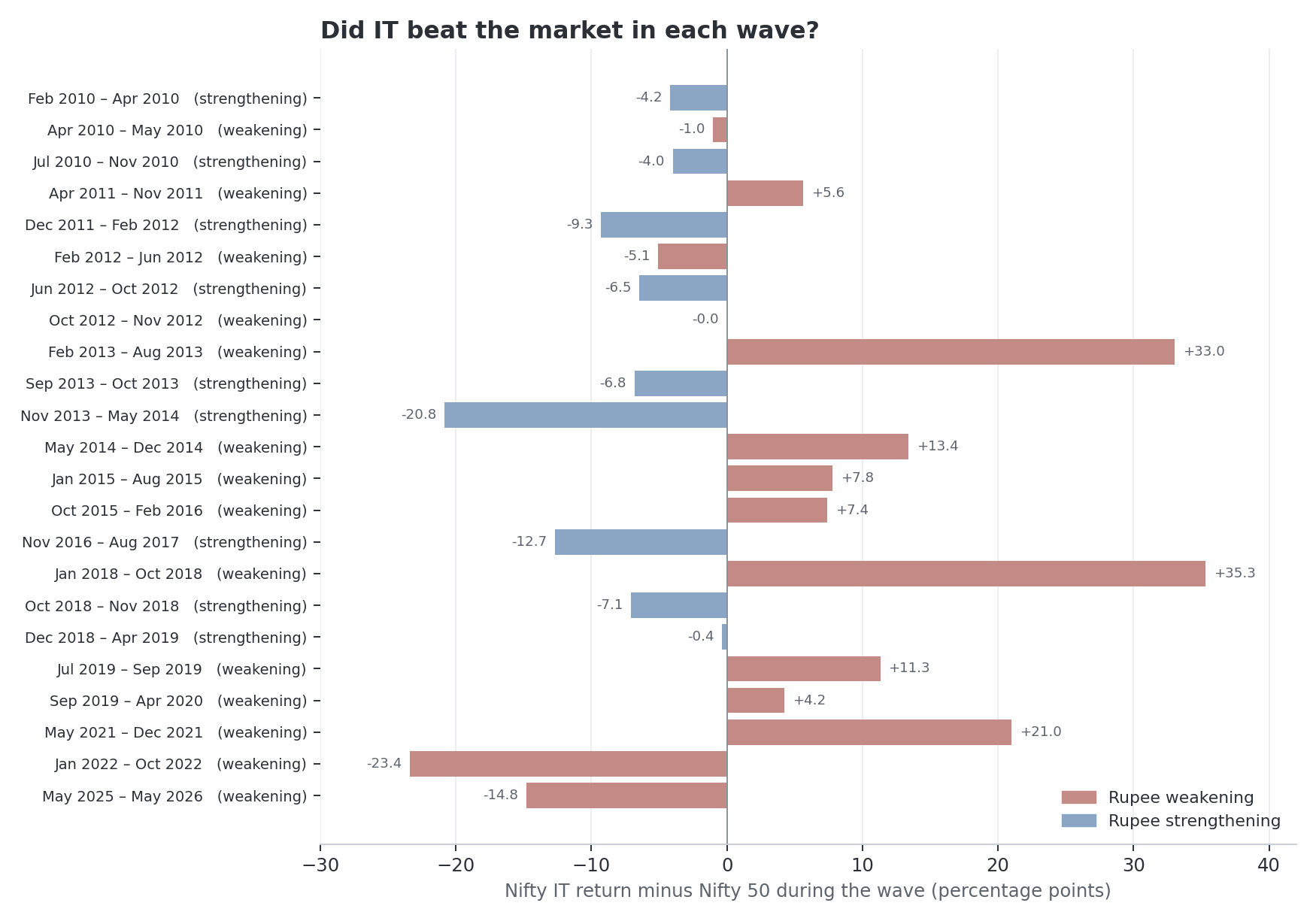

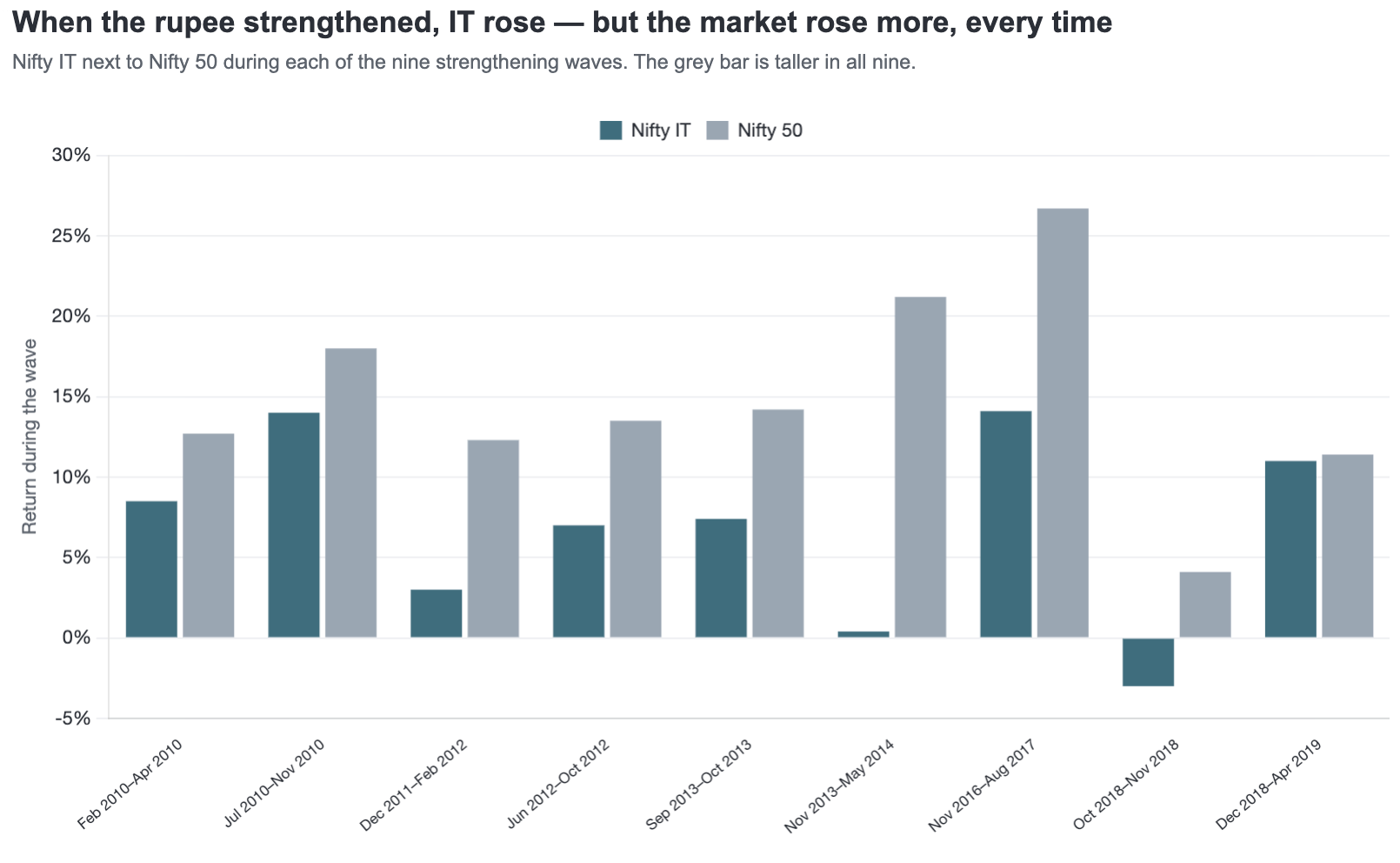

Visual: Nifty IT minus Nifty 50 during every sharp rupee wave.

The detailed table and chart above show that the relationship was clearly mixed. In some rupee-weakening periods, such as 2013, 2014, 2018 and 2021, Nifty IT performed strongly. In others, such as 2012, 2022 and 2025, it underperformed sharply. So the simple statement, weak rupee means IT stocks rise, does not hold every time.

We needed to count this more carefully.

Did the fall in rupee actually benefit IT stocks?

We identified 14 rupee-weakening waves.

During these periods, Nifty IT rose in only 5 waves and was flat or negative in the remaining 9.

So if the question is, ‘Did IT stocks usually rise when the rupee weakened?’

The answer is no.

This is the first key finding. While a weaker rupee can benefit IT companies by increasing the rupee value of their dollar earnings, IT stocks didn’t consistently move higher during periods of rupee weakness.

But that’s only half the story.

Many of these rupee-weakening periods also coincided with broader market declines. So looking only at whether IT stocks went up can be misleading.

A better question is: Did IT perform better than the broader market?

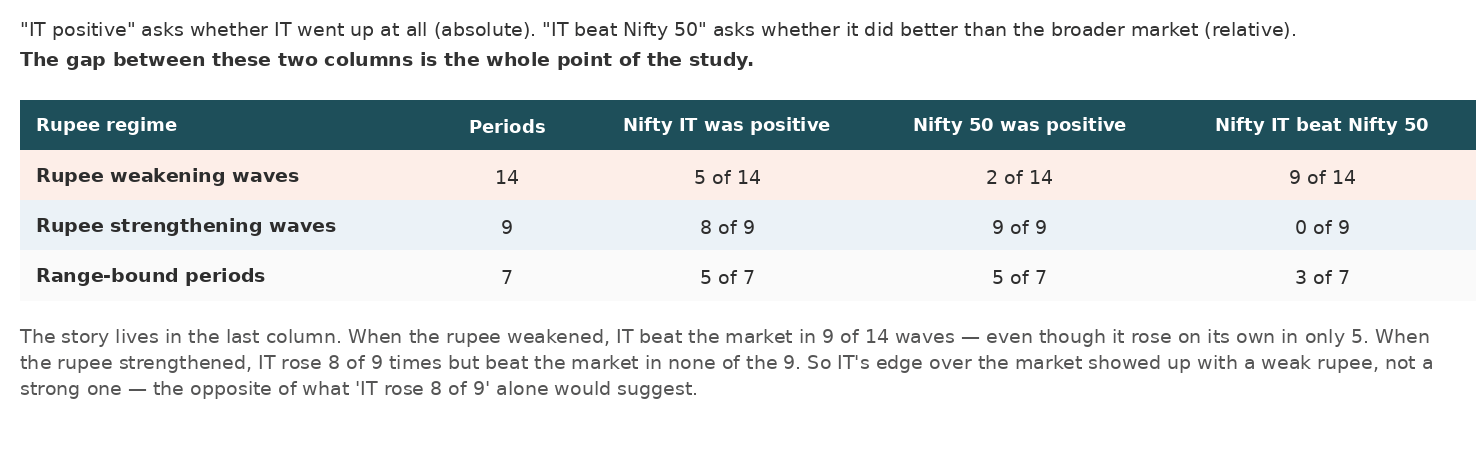

To answer that, we compared Nifty IT with Nifty 50 across all three currency environments.

When we put the three regimes side by side, the difference becomes clear.

At first, the numbers look a little confusing.

When the rupee weakened, Nifty IT went up only 5 out of 14 times. So a weak rupee didn’t automatically mean IT stocks would rise.

But here’s the interesting part. Even though IT didn’t always go up, it still performed better than Nifty 50 in 9 of those 14 periods. In other words, IT often held up better than the broader market when the rupee was under pressure.

Now look at the rupee-strengthening periods. Nifty IT went up 8 out of 9 times. At first glance, that seems to contradict the common belief that a weaker rupee benefits IT stocks.

The answer is that stock prices are influenced by much more than just the currency.

During those same nine periods, Nifty 50 was positive in all nine and outperformed Nifty IT every single time. So IT wasn’t leading the market, it was simply rising along with a strong broader market while other sectors performed even better.

Visual: During rupee-strengthening waves, IT often rose but still lagged Nifty 50.

This doesn’t prove that a stronger rupee caused IT to underperform. But it does show that the currency story didn’t disappear. A stronger rupee didn’t stop IT stocks from going up, it simply coincided with the broader market delivering even stronger returns.

That isn’t entirely surprising.

Rupee-strengthening periods often occur during calmer or stronger economic conditions. In such environments, domestic sectors like banks, autos, industrials and other cyclicals tend to perform well. IT stocks can still generate positive returns, but they may not keep pace with the rest of the market.

This is why comparing IT with Nifty 50 is so important. Looking only at IT’s returns might suggest that IT performs well when the rupee strengthens. But once we compare it with the broader market, the picture becomes much clearer: IT stocks often went up, but they lagged the broader market every single time.

Could investors have actually used the falling rupee as a signal?

There is one practical problem with studying a rupee fall from its beginning to its end: the starting point is only obvious in hindsight.

An investor watching the market in real time would notice the move only after the rupee had already weakened significantly.

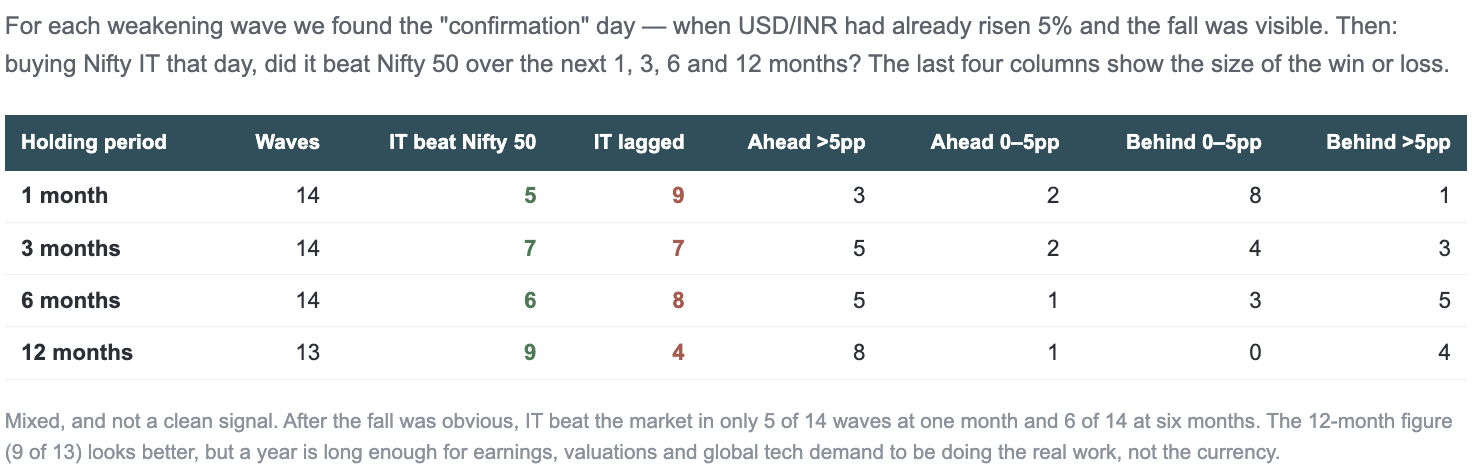

So, for every rupee-weakening wave, we identified the date when USD/INR had risen by 5% from the start of the move. We called this the confirmation date, the point when the fall had become large enough for an investor to notice.

We then asked, If an investor bought Nifty IT on the confirmation date, did it beat Nifty 50 over the next 1, 3, 6 and 12 months?

The table also shows how much IT beat or lagged Nifty 50.

For example, if Nifty IT returned 12% and Nifty 50 returned 7%, IT was ahead by 5 percentage points. Similarly, if Nifty IT returned 3% and Nifty 50 returned 8%, IT was behind by 5 percentage points.

The results were mixed.

After one month, IT beat Nifty 50 in 5 of 14 cases. After three months, it did so in 7 of 14 cases. At six months, the result weakened, with IT outperforming in only 6 of 14 cases.

The 12-month result looked stronger, with IT beating Nifty 50 in 9 of 13 cases. But one year is a long period, and by then several other factors (such as earnings, valuations, US technology spending and overall market conditions) could have influenced returns.

So the signal was not clean. If investors waited until the rupee fall became visible and then bought IT, the outcome depended heavily on the holding period.

There is also one technical limitation.

Some rupee waves only moved slightly more than 5%. In those cases, the confirmation date came very close to the end of the currency move. By the time the investor noticed the fall, most of the move had already happened.

That is why we did not treat the return from the confirmation date to the end of the wave as the main evidence.

Instead, the cleaner test was to measure Nifty IT’s performance against Nifty 50 over fixed 1-, 3-, 6- and 12-month periods after confirmation.

The takeaway is simple: a visible fall in the rupee was not a reliable signal to buy IT stocks.

What happened when the rupee stayed range-bound?

We also looked at periods when USD/INR was not moving strongly in either direction.

These were range-bound periods, when the rupee was neither weakening sharply nor strengthening sharply.

There were seven such periods.

During them:

Nifty IT was positive in 5 of 7 cases.

Nifty 50 was also positive in 5 of 7 cases.

Nifty IT beat Nifty 50 in only 3 of 7 cases.

This comparison is useful because it shows that IT stocks do not need a falling rupee to rise.

IT may perform well because company earnings are improving. It may benefit from strong technology spending by global clients. It may rise because valuations are increasing or because the broader market is doing well.

At the same time, the fact that IT beat Nifty 50 in only 3 of the 7 range-bound periods suggests that a stable rupee did not give the sector any clear advantage either.

Taken together, the results tell us that currency is only one of many forces affecting IT stocks.

A falling rupee can help IT companies at the earnings level, but it was not a reliable signal for investors to buy IT stocks. And IT could still rise even when the rupee was not weakening.

The rupee matters, but it does not decide the entire outcome.

What did we actually learn?

The popular belief is partly correct.

A weaker rupee can help Indian IT companies because a large share of their revenue comes from overseas clients and is often billed in foreign currency. When those dollars are converted back into rupees, reported revenue and margins can receive a boost.

That is the business effect.

But the share-price effect is different.

Stocks do not move only because accounting numbers improve. They move based on expectations. Also, many IT companies hedge part of their foreign-exchange exposure using forwards, options and other derivatives. That can smooth or delay the benefit of a weaker rupee. If investors are worried about US client spending, weak deal conversion, margin pressure, AI disruption, or high valuations, then the currency benefit may not be enough.

That is exactly what the data showed.

During the 14 sharp rupee-weakening waves in our study, Nifty IT was positive only 5 times. So a falling rupee did not automatically mean IT stocks made money.

But Nifty IT still beat Nifty 50 in 9 of those 14 periods. So the weak rupee did seem to offer some relative support. IT often held up better than the broader market, even when it did not rise in absolute terms.

This means the rupee effect worked more like a relative advantage than a direct buy signal.

It helped the sector’s position compared to the market.

It did not guarantee that investors would earn positive returns.

The signal also became less reliable once the rupee fall became obvious. By the time investors saw the currency move clearly, part of the benefit may already have been priced in. At that point, other forces started mattering more: demand, valuations, margins, global tech sentiment, US client budgets, and the broader market cycle.

So the final answer is that a weak rupee can support IT earnings. It can make reported rupee numbers look better. It can sometimes help Nifty IT outperform the broader market.

But it is not enough, on its own, to justify buying IT stocks. The rupee is a tailwind, not a magic switch.