On 24 March 2023, something important happened for debt fund investors.

The Union Budget had already been presented almost two months earlier. Most investors assumed the major tax changes for the year were already known. But while Parliament was discussing the Finance Bill, one more amendment was introduced.

It changed how many debt mutual funds would be taxed.

Now, that may sound like a technical change. But for investors who compared debt funds with bank fixed deposits, it mattered a lot.

For years, one of the biggest reasons investors preferred debt mutual funds over FDs was not just returns. It was tax.

To really see why this mattered, we need to take a step back and look at how things used to work before 2023.

Suppose you have Rs 1 lakh to invest. You can either put it in a bank fixed deposit or invest it in a debt mutual fund.

At first glance, these look like very different products. An FD is a bank deposit. A debt fund is a mutual fund.

But if you zoom out, both are connected to lending. When you put money in an FD, the bank uses its pool of deposits to lend and invest. When you invest in a debt mutual fund, the fund buys debt securities issued by companies, banks, PSUs, or the government.

So in broad terms, both are trying to earn returns from debt.

But the tax treatment was very different.

In an FD, the interest is taxed at your income-tax slab. So if your FD earns Rs 80,000 in interest and you are in the 30% slab, that interest is taxed at 30%. In other words, every year, a portion of the interest your FD generates goes toward paying taxes, reducing your effective return.

Debt mutual funds worked differently under the old rules.

If an investor stayed invested for more than 3 years, the gains could qualify as long-term capital gains. And that came with an important tax benefit called indexation.

Now, indexation sounds like a complicated tax term, but the idea was actually quite simple.

Before calculating your tax, the government allowed you to increase your original purchase price to account for inflation using something called the Cost Inflation Index.

Why did that matter?

Because if your purchase price became higher, your taxable profit automatically became smaller. And if your taxable profit was smaller, you paid less tax.

For someone in the 20% or 30% tax bracket, it meaningfully improved the final after-tax return.

That is why the FD vs debt fund comparison was never only about returns. It was also about post-tax returns.

A debt fund did not always need to beat an FD by a huge margin before tax. For a higher-tax investor, the old tax treatment itself could improve the final result.

Then came the 2023 amendment.

For fresh investments made on or after 1 April 2023, the old indexation benefit was removed for most debt mutual funds. Instead, the gains would be taxed according to the investor’s income-tax slab.

So the obvious question was, if debt funds lost their tax advantage, did fixed deposits become better?

But to answer that properly, we cannot look only at the tax rule.

We also need to look at what actually happened to returns.

Because even after losing a tax benefit, a debt fund could still beat an FD if its return was high enough. And even with a tax benefit, a debt fund could still lose if its return were weak.

So we tested this using historical FD rates, debt fund NAVs, and post-tax returns.

The Experiment

We assumed an investor had Rs 1 lakh to invest on 1 April each year.

The investor had two choices:But we did not randomly choose funds.

For every 1 April investment date, the investor looked at the previous financial year’s best-performing fund in that category and invested in that fund.

So if the investment date was 1 April 2020, the fund was selected based on its performance from the previous financial year. Then the investor held it for the full comparison period.

This reflects a common investor behaviour: looking at last year’s return table and choosing the fund that performed best.

We then compared that selected fund with an SBI FD over the same holding period.

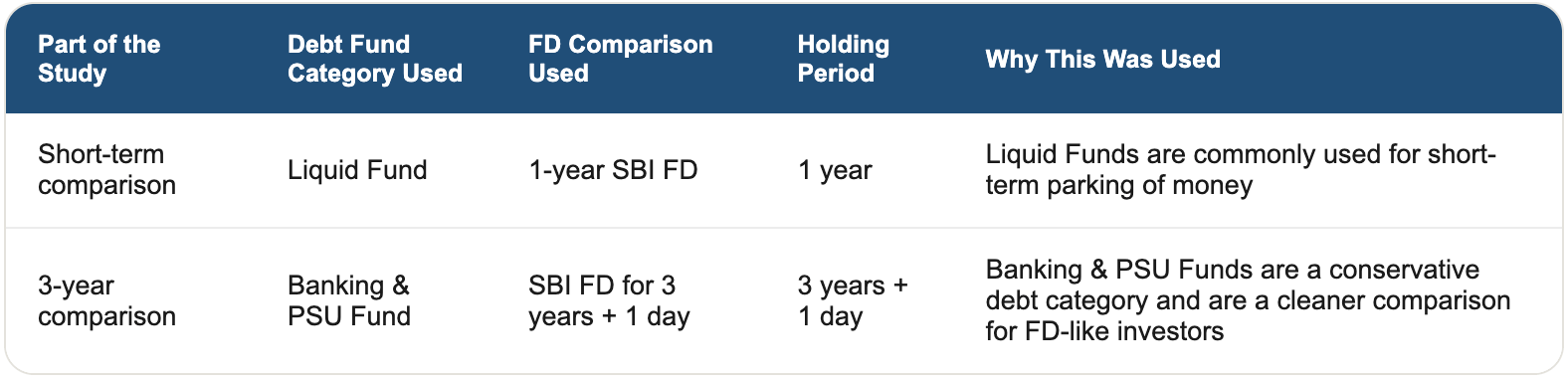

For the 1-year part, we used liquid funds because investors often use them to park money temporarily.

For the 3-year part, we used Banking & PSU Funds because they are one of the cleaner open-ended debt fund comparisons for a conservative FD investor.

They are still not FDs. The return is not fixed, and the NAV can move. But these funds mainly invest in debt issued by banks, PSUs, and public financial institutions, so they are more suitable for this comparison than funds like Credit Risk, Gilt, Dynamic Bond, or Medium Duration Funds.

We also kept the FD comparison clean.

There was no FD rollover. If the holding period was one year, the comparison ended after one year. If the holding period was 3 years + 1 day, it ended after 3 years + 1 day.

This way, we were not asking what happens if someone keeps renewing FDs for many years.

We were asking a simpler question:

If an investor knows they need the money after one year or after three years, would the selected debt fund leave them with more money than an SBI FD over the same period?

How tax was applied

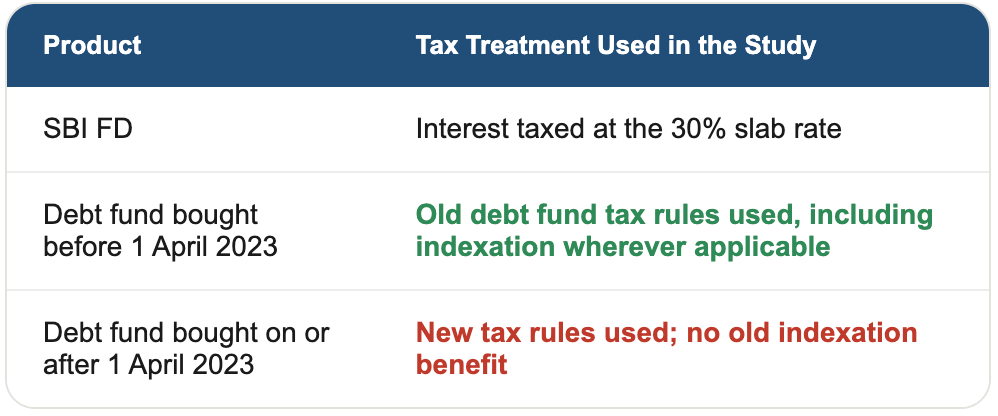

For this study, we focused on a 30% tax slab investor.

We chose this because the old debt fund tax advantage was most significant for higher-tax investors. Interest earned on fixed deposits (FDs) is taxed at the investor’s income-tax slab, so someone in the 30% slab pays much more tax on FD interest than someone in the 5% slab.

For debt funds, the tax rule depended on the investment date.

This is important because the 2023 tax change does not affect all parts of the study equally.

For Liquid Funds, the holding period was only one year, so indexation was not really relevant even under the old rules.

For Banking & PSU Funds, the holding period was 3 years + 1 day, so the old indexation benefit mattered for investments made before 1 April 2023.

That is why the study has two parts.

The Liquid Fund section checks whether a short-term debt fund meaningfully beat a 1-year FD.

The Banking & PSU section checks what changed when the old 3-year debt fund tax advantage was removed.

Result

What happened in the 1-year category?

Liquid Fund Vs FD

For the 1-year comparison, we focused only on Liquid Funds.

This is not the same as an FD. In an FD, the bank promises a fixed return. In a Liquid Fund, the fund invests in very short-term debt and money market instruments, and the return comes through NAV movement. So the return is not fixed.

But for short-term parking, Liquid Funds are one of the closest debt fund comparisons because investors often use them when they want to keep money for a short period without taking equity-like risk.

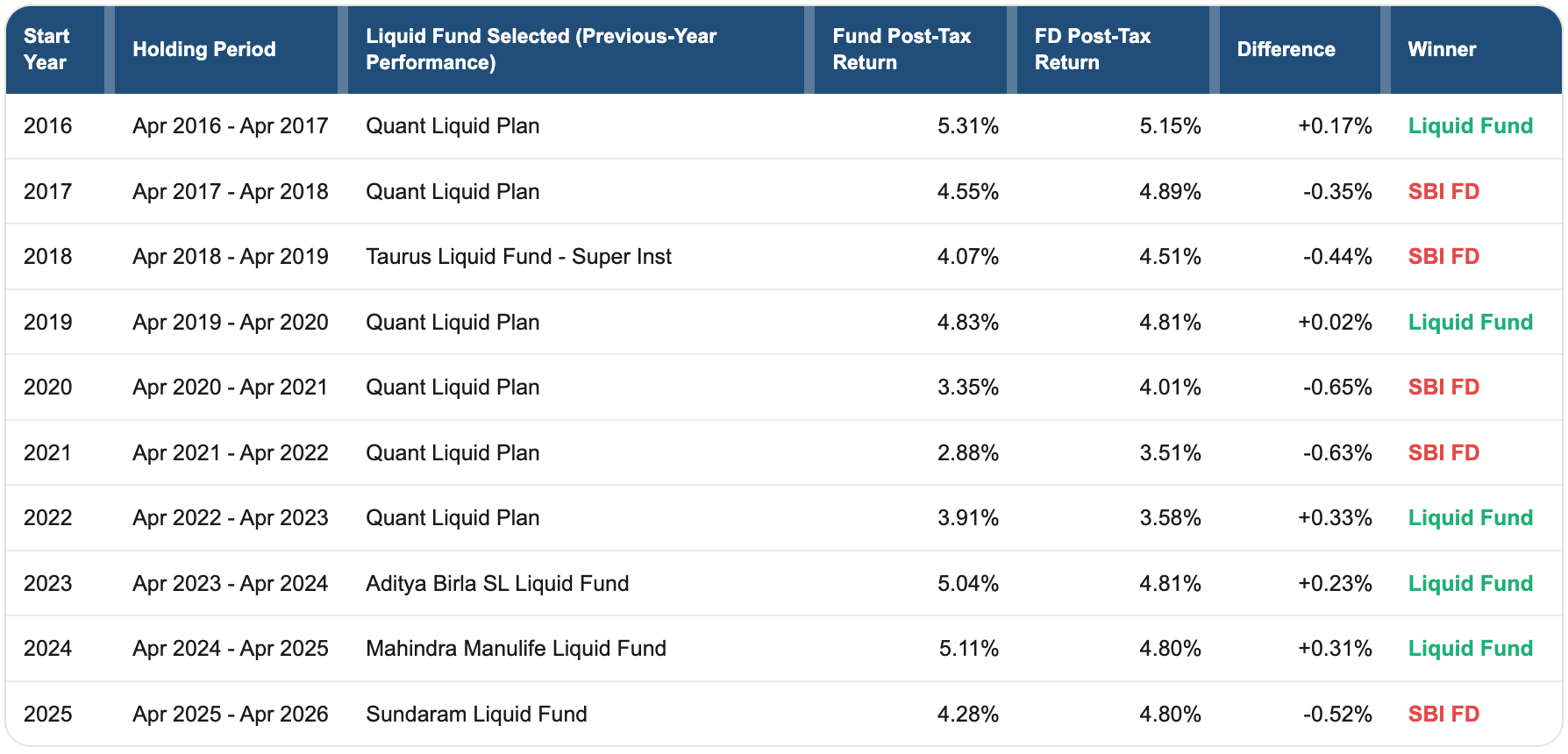

Here, the investor picked the previous financial year’s best-performing Liquid Fund on every 1 April and held it for one year. The same ₹1,00,000 was also invested in a 1-year SBI FD.

The returns below are total post-tax returns over the full 1-year holding period, not annualised comparisons beyond that period.

The result is mixed.

The selected Liquid Fund beat the FD in 5 out of 10 years. The FD beat the selected Liquid Fund in the other 5 years.

More importantly, the difference was usually small. In 2019, Quant Liquid Plan beat the FD by just 0.02 percentage points. That is barely a meaningful gap. In 2025, Sundaram Liquid Fund was selected because it was the previous year’s best-performing Liquid Fund, but it still lost to the FD by around 0.52 percentage points.

So this does not show one clear winner.

It shows that for 1-year money, picking last year’s best Liquid Fund did not reliably beat a 1-year SBI FD. Sometimes it worked. Sometimes it did not. And most of the time, the gap was not very large.

The tax-change angle is also different here.

Because this was only a 1-year holding period, indexation was not really relevant even under the old debt fund tax rules. So the 2023 tax change does not explain much in the Liquid Fund result.

The takeaway is that over a 1-year horizon, choosing the previous year’s best-performing Liquid Fund did not provide a reliable advantage over an FD. The winner varied from year to year, and the return gap was usually too small to be decisive.

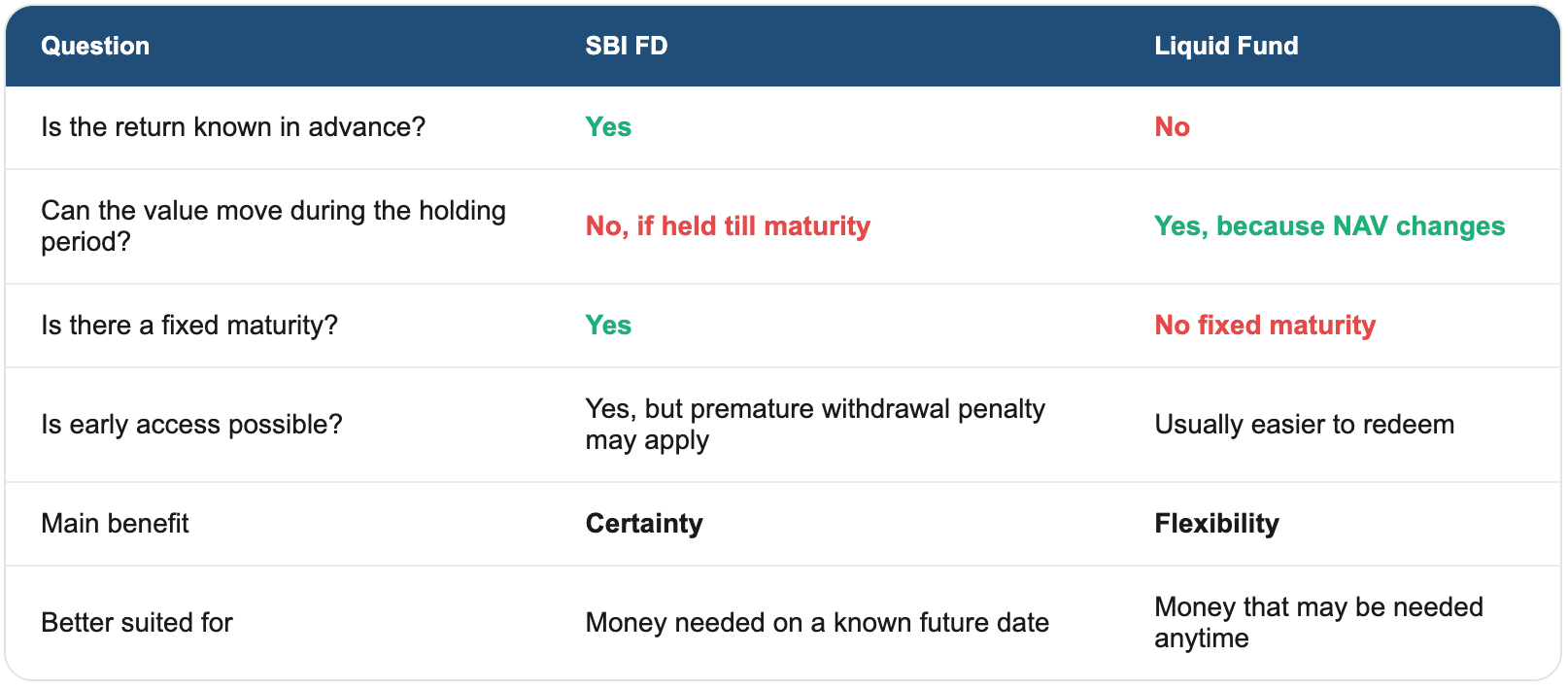

If Liquid Funds are more flexible, why use an FD at all?

This is the natural question.

If the difference in returns is usually small and liquid funds offer greater flexibility, why would anyone still choose a fixed deposit?

Because the products solve different problems.An FD exists because many investors want certainty. They know the rate before investing, they know the maturity date, and they know what they will receive if they hold till maturity. For someone who needs money exactly after one year and does not want NAV movement, an FD is simpler.

A liquid fund exists for a different reason. It is useful when the investor wants to park money but is not sure exactly when it will be needed. The money may be required in a few days, a few weeks, or a few months. In that case, flexibility matters more than locking into a fixed maturity.

So the choice is not just about return.

If the investor wants a known return and a fixed date, the FD fits better.

If the investor wants flexible parking and can accept small NAV movement, the Liquid Fund fits better.

That is why both products exist.

In our data, the selected Liquid Fund beat the FD in 5 out of 10 years and lost in the other 5. The gap was usually small. So the result does not prove that one product is clearly better. It only shows that, for 1-year money, the return difference was not strong enough to make the decision purely about returns.

What happened in the 3-year ?

Banking & PSU fund Vs FD

For the 3-year comparison, we focused on banking & PSU funds.

This is not the same as an FD. In an FD, you are lending money to the bank, and the bank promises a fixed return. In a Banking & PSU Fund, the fund buys debt issued mainly by banks, public sector companies, and public financial institutions. The return is not fixed because the fund’s NAV keeps moving.

But for a conservative FD investor, this is still one of the cleaner debt fund comparisons because the broad exposure is to relatively stable borrowers, not to credit-risk funds, gilt funds, or long-duration interest-rate bets.

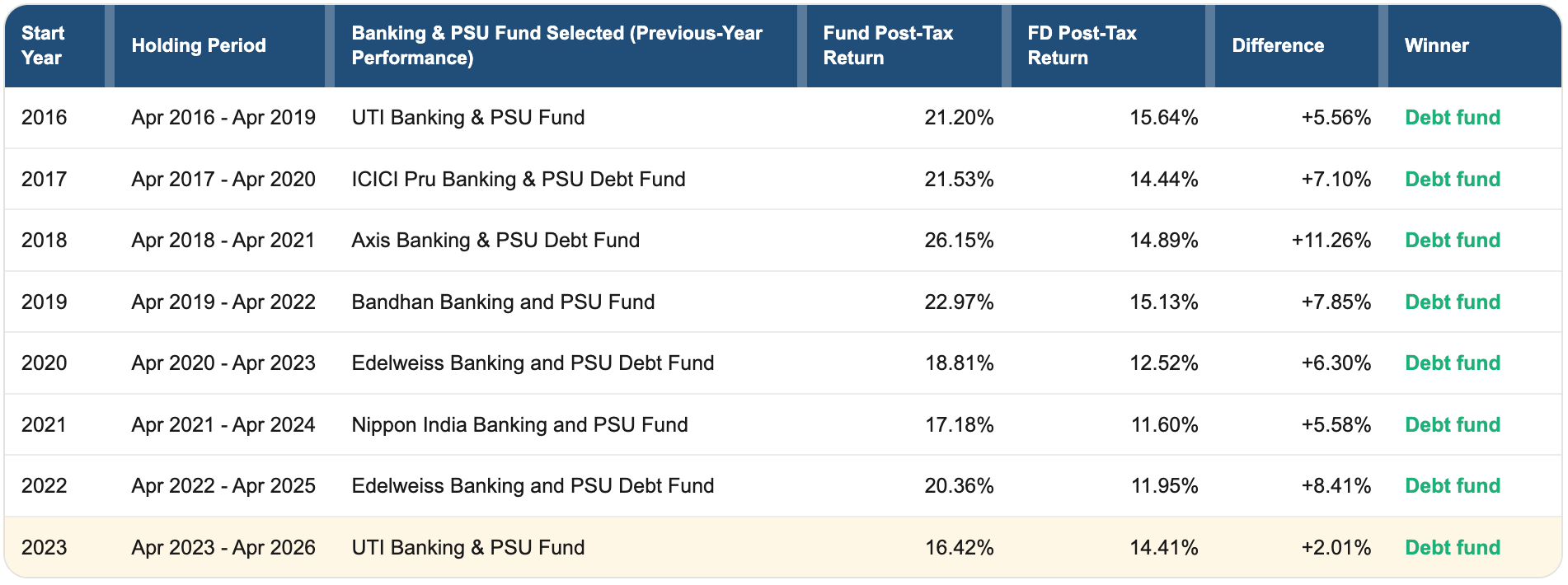

Here, the investor picked the previous financial year’s best-performing Banking & PSU Fund on every 1 April and held it for 3 years + 1 day. The same Rs 1,00,000 was also invested in a matching SBI FD for the same period.

The returns below are total post-tax returns over the full holding period, not annual returns.

This result is much cleaner than the 1-year liquid results.

In every completed 3-year period from 2016 to 2023, the selected Banking & PSU Fund beat the matching SBI FD after tax for a 30% taxpayer.

But the important part is not just who won. It is why the fund won.

For the 2016 to 2022 start years, the investment was made before the 2023 tax change. So the fund had two things working for it: the actual return of the fund and the old indexation benefit.

The 2023 row is different.

That investment was made after 1 April 2023. So the old indexation benefit was not available. Under Section 50AA, gains from specified mutual funds acquired on or after 1 April 2023 are taxed at the investor’s applicable slab rate, even if they were held for more than three years.

So UTI Banking & PSU Fund still beat the FD in the 2023 window, but the gap was smaller. The fund gave 16.42% after tax over the full holding period, while the FD gave 14.41%. That is a difference of only 2.01 percentage points.

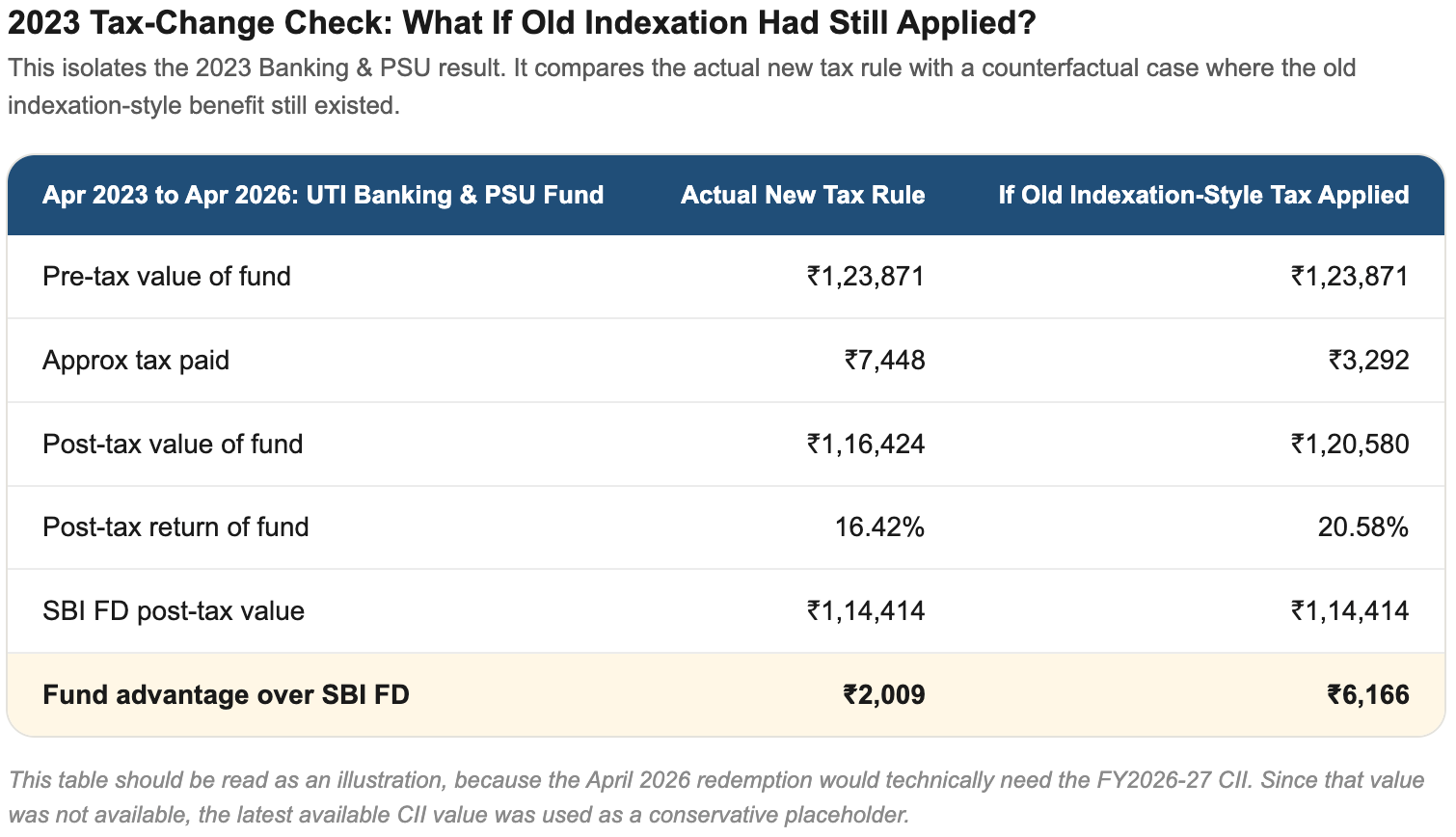

Now, to see what the tax change actually did, we can run one counterfactual.

What if the old tax benefit had still applied in 2023?

This is only an illustration, because the Apr 2026 redemption would technically need the FY2026-27 CII, and the official CII table currently lists values only up to FY2025-26, where the CII is 376.

So using the latest available CII value as a conservative placeholder, the picture would have looked like this:This is the tax change in one table.

Under the actual post-2023 rule, the selected fund still beat the FD. But it beat it by around Rs 2,009 on a Rs 1 lakh investment.

If the old indexation-style benefit had still been available, the same fund would have beaten the FD by roughly Rs 6,166 using the conservative CII placeholder.

So the 2023 tax change did not flip the winner in this case. The Banking & PSU Fund still came out ahead.

But it clearly reduced the advantage.

That is the real point.

Before 2023, a good 3-year debt fund could beat an FD through both return and tax treatment. After 2023, the same kind of fund has to rely much more on actual performance.

The fund can still win.

But tax is doing much less of the work.

Conclusion

So, what did we actually learn?

The biggest takeaway is that the FD versus debt fund debate was never just about taxes.

Before 2023, the tax rules gave debt mutual funds a meaningful advantage, especially for investors in higher tax brackets. That made it easier for a debt fund to come out ahead of a fixed deposit on an after-tax basis.

The 2023 tax change removed a large part of that advantage.

But that does not automatically mean fixed deposits became the better choice.

In this study, the selected debt fund could still beat the FD in several comparisons. The difference is that the advantage became smaller once the old indexation benefit disappeared.

In other words, the rules of the game changed.

Earlier, a debt fund had two ways to beat an FD. It could earn a higher return, and it could benefit from more favourable tax treatment.

Today, one of those advantages is largely gone. So if a debt fund is going to justify its place against an FD, it has to do so more through actual performance.

That also makes the choice between the two products clearer.

If the priority is certainty, a fixed deposit still does exactly what it always has. The investor knows the interest rate, the maturity date, and the amount they should receive if they hold it till the end.

A debt mutual fund is different. Its return is not guaranteed, but it offers flexibility and the possibility of earning more if the underlying portfolio performs well.

So the question investors should ask today is not just:

“Is a debt fund more tax-efficient than an FD?”

It is this:

“After applying the tax rules that exist today, did the debt fund earn enough to beat the FD over the same period?”

That is the comparison that matters now.

And as this analysis shows, the answer depends on the debt fund category, the holding period, and the return the fund actually delivers.