Every month, mutual funds in India do something unusual for a financial product.

They tell you everything.

They are mandated by SEBI to disclose their full portfolios.

This means, investment in every stock, every sector and the exact percentage of allocation is published on their website, available to anyone for free.

This transparency also brings up an interesting thought that has likely crossed the minds of anyone who has spent time reading these disclosures.

If I can see exactly what the fund manager bought, why do I need the fund?

The manager’s entire portfolio is available. Updated every 30 days.

You could, in theory, replicate it yourself. You could buy the same stocks and use the same proportions. Invest directly, without middlemen or any fees.

Would it work? Would it give better returns than the fund? We decided to test it.

We chose the ICICI Prudential Focused Equity Fund and tracked it through January 2020 to December 2025.

We chose a focused fund for two main reasons. Many mutual funds hold 60, 70, or sometimes even 100 stocks. Replicating those portfolios is practically unmanageable for an individual investor.

Two, the fund stays almost fully invested in equities, typically around 98-99%. That makes the comparison much closer to directly investing in stocks.

With almost no cash on the side, what you see is essentially the same set of companies the fund is invested in.

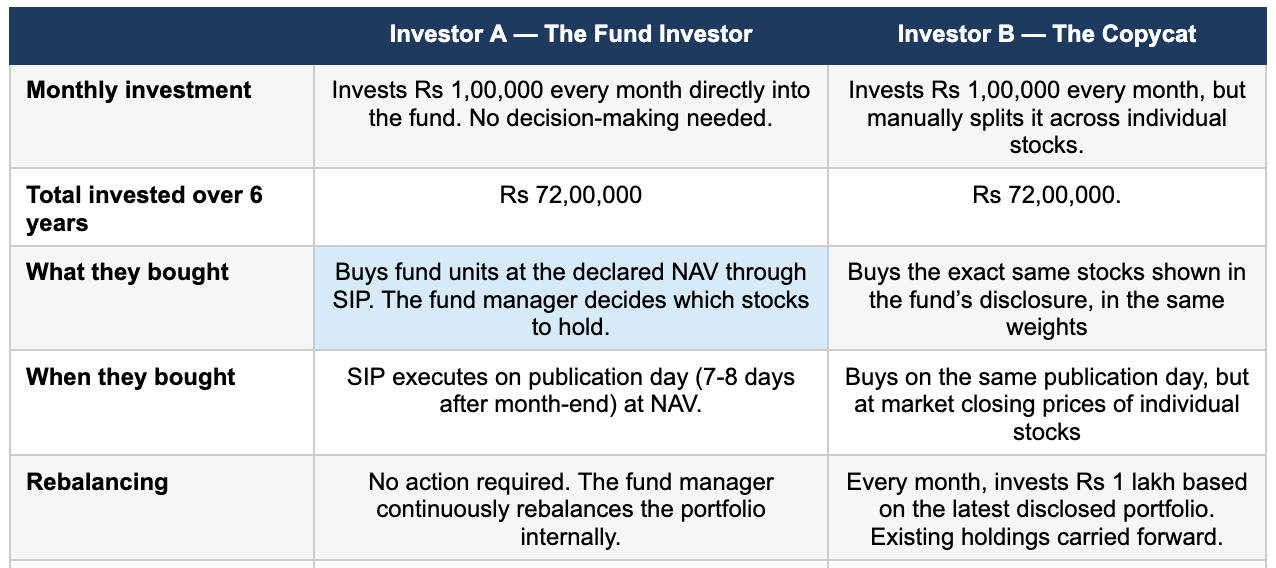

We considered two investors. Both of them invested Rs 1,00,000 every month. Both invested on the same day.

Investor A put their money in the mutual fund.

Investor B decided to copy the fund. So every month, whatever the fund disclosed, they adjusted their portfolio accordingly.

What you are always reading is last month’s decision

Before looking at any returns, there is one structural aspect of this strategy that needs to be understood.

Across all 72 months in this study, the ICICI Prudential Focused Equity Fund published data in 5 to 8 days after the month end.

For example, if we take a look at the data from 2024, the fund’s portfolio as of 31 Jan was published on 8 Feb. This is a 7-day reporting lag after month-end.

In reality the lag could be even bigger. If the fund manager started buying a stock on, say, 5 Jan, an individual investor would only get to know about that on 8 Feb. This specific decision becomes visible after a 34-day gap.

This creates a clear mismatch between the two investors.

So Investor B, as the copycat, is reacting to data which has been disclosed with a delay. Investor A is investing in real time based on the fund manager’s decisions as they happen.

So the two investors are not actually buying the same stocks, in the same composition, at the same time.

Results

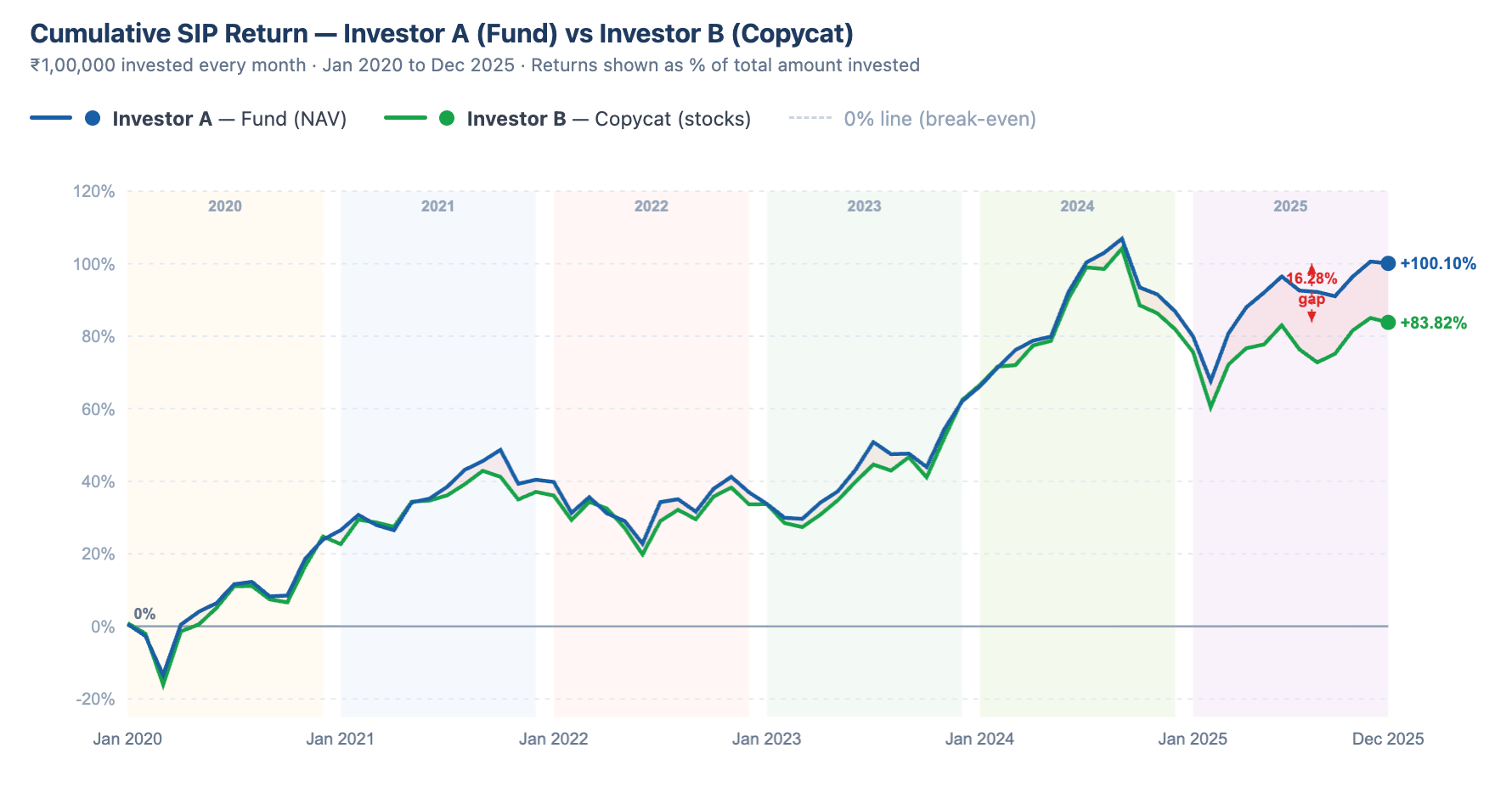

Both investors appeared to be doing the same thing on the surface. But over time, their outcomes began to diverge.

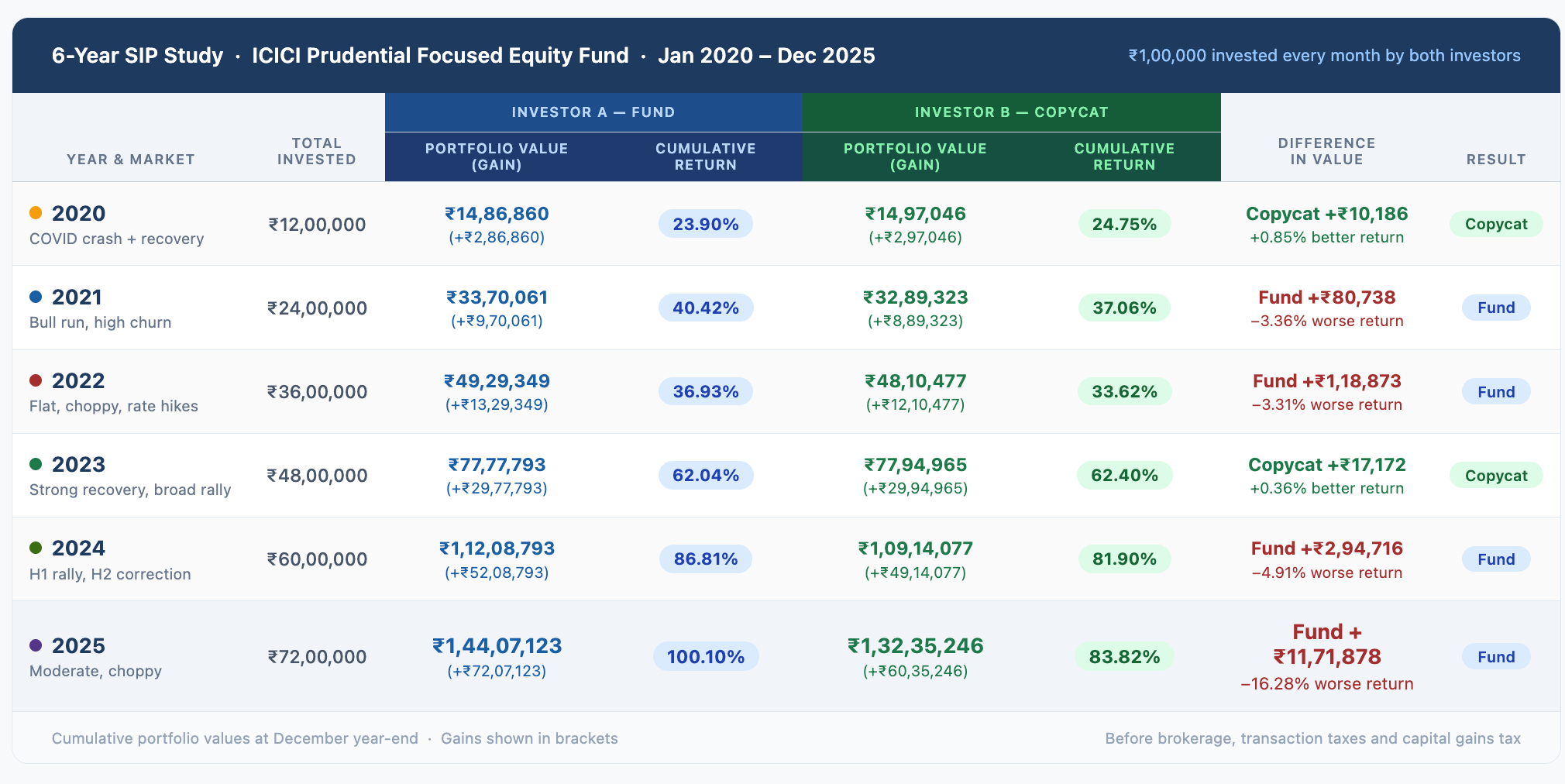

At the end of 6 years, the mutual fund investor ended up with Rs 1.44 crore.

The copycat investor ended up with Rs 1.32 crore.

Both made good money. Both nearly doubled what they started with. But there was still a gap of Rs 11.7 lakh between them.

How did this happen?

In 2020, almost nothing changed in the portfolio. Hardly any stocks were bought or sold. When the COVID crash came, both investors faced similar losses. And when the market recovered, both went up. During this period, the delay did not have much impact.

The same pattern repeated in 2023. The drivers of returns were already part of the portfolio, so the copycat simply held on and participated in the move.

In both years, the copycat finished with slightly better returns.

In 2021, the fund manager made a lot of moves. By the time the copycat entered or exited, prices had already moved. Those delays accumulated quickly and erased its earlier lead within a short period. A similar pattern played out in 2024, where a larger reshuffling widened the gap again, and it never fully recovered.

Basically, in years where the fund didn’t change much, the copycat stayed close. Sometimes they even did slightly better. But in years where the fund was more active, buying new stocks or selling old ones, the copycat started falling behind.

When the portfolio is stable, the copycat stays close. When activity increases, the lag starts to matter. This is because the fund manager acts first. The copycat reacts later, which often means entering at slightly higher prices and exiting at slightly lower ones. Each difference is small, but they add up over time.

Fees and Charges

For the study, everything was calculated as gross returns. This means no brokerage fees, no government taxes, no execution costs.

But copying a fund means buying and selling constantly.

Every month, Investor B deployed fresh Rs 1 lakh by splitting it across every stock the fund currently held, between 20 and 30 stocks depending on the month. Each stock was a separate buy order. On top of that, every time the fund removed a stock from its portfolio, Investor B had to sell it too.

Over six years, that added up to 1,981 buy orders and 92 forced sell transactions, 2,073 trades in total. Investor A made 72. One per month.

Every single one of those 2,073 trades attracted brokerage and Securities Transaction Tax. On any individual trade, these costs feel small. But across 2,073 transactions over six years, they accumulate into a real and unavoidable drag on returns.

Then there is the tax on gains. Each of those 92 forced sells was a taxable event. Most of those stocks were held for less than a year, because the fund added them and removed them within months. Any profit made on a position held under 12 months is taxed at 20% as Short Term Capital Gains. So every time the fund rotated out of a stock and Investor B followed, money went to the government.

Investor A did not face any of this. Mutual funds buy and sell internally without triggering a tax event for the investor. You only pay tax when you personally sell your units. And if you held them for more than a year, the applicable rate is 12.5%, not 20%.

So in reality, the difference of Rs 11.7 lakh turns out to be superficial. The real gap, after brokerage, STT, and short-term capital gains tax, is likely between Rs 14 lakh and Rs 15.4 lakh on the total Rs 72 lakh invested.

The Real Takeaway

The copycat strategy is not broken in theory. It just does not work in practice. Because by the time you saw it, acted on it, paid for it, and got taxed on it, the advantage had already gone.

This is what the data actually says. Investing in the fund directly was simpler, cheaper, and more effective. One transaction a month.

Copying the fund looked clever but was not. Same stocks, more effort, worse outcome. The fee you were trying to save turned out to be the smallest cost in the entire process.

The real cost was the delay. Not the 0.59% expense ratio, but the gap between when the fund manager acted and when you found out. That lag changed everything. By the time you reacted, the opportunity had already moved.

So the conclusion is simple.

If you believe in the fund manager’s process, invest in the fund. Trying to replicate their decisions from a monthly disclosure is not a shortcut. It is a slower and more expensive way to get to a worse result.

A mutual fund does not just give you a list of stocks. It gives you timing, execution, tax efficiency, and judgement.

All of that comes bundled into a single transaction every month.