Food delivery apps have become deeply ingrained in the life of urban Indians.

Platforms like Zomato and Swiggy are popular because they make the entire ordering process convenient. They offer a choice of menus to choose from all in a single place, and customers can pay digitally and track their order in real-time, turning a multi-step chore into a three-click experience.

They handle the entire logistical headache without having to contact anyone.

But these platforms are not the only way to order food. Many restaurants also accept direct orders. A lot of the time, such orders can turn out to be cheaper for the customer.

The meal itself remains exactly the same.

The food is prepared by the same chefs, in the same kitchen, using the same ingredients. It is packaged in the same container and delivered to the same customer. Nothing about the product has changed.

The only difference is the channel through which the order was placed.

So why does the price differ?

The answer is simple. Food delivery platforms provide a service. They help customers discover restaurants, process payments, and manage logistics. In return, they charge fees for that convenience.

The customer is not paying for a different meal.

They are paying for a different route to get the same meal.

Direct and Regular mutual funds operate on a surprisingly similar principle.

Understanding Direct vs Regular Plans

Direct and Regular Plans are not different mutual funds. They are simply two different ways of investing in the same mutual fund.

When an investor chooses a Regular Plan, the investment is made through an intermediary such as a distributor, broker, bank, or financial advisor. In return for distribution and advisory services, the mutual fund pays a commission to the intermediary.

This cost is built into the fund’s expense ratio and is ultimately borne by the investor.

When an investor chooses a Direct Plan, they invest directly with the mutual fund company or through a platform that does not charge distribution commissions. The research and investment decisions are made entirely by the investor.

As a result, Direct Plans have lower expense ratios than their regular counterparts.

Because there is no middleman commission built into a Direct Plan, its cost is lower. But just like ordering food, the underlying product is identical.

Both plans track the exact same stocks, managed by the exact same fund manager, inside the exact same portfolio.

This raises an obvious question: do direct and Regular Plans differ in terms of returns?

The Experiment

We wanted to understand whether the choice between a direct and Regular Plan actually makes a meaningful difference to investor returns.

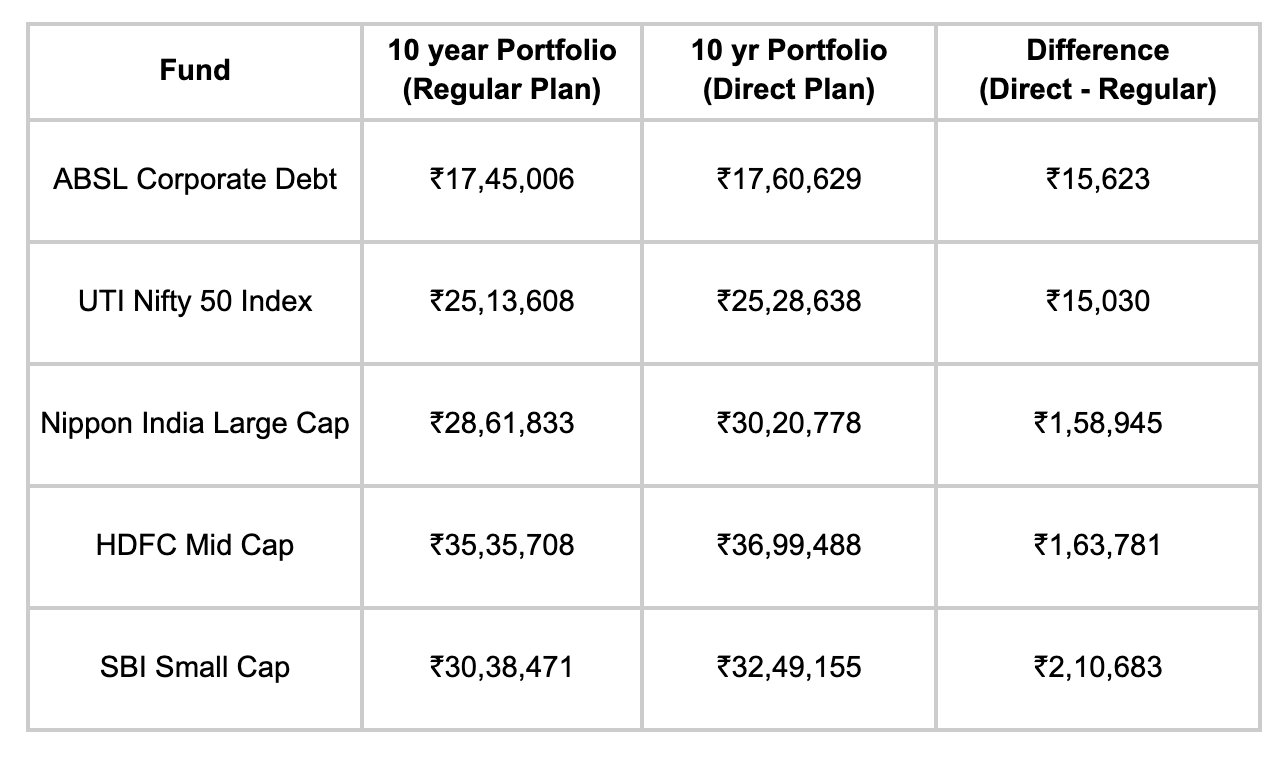

To test this, we selected a set of mutual funds across different categories and compared the performance of their direct and Regular Plans over a 10-year period. Each month an SIP of Rs 10,000 was made into the fund through both plans.

At the end of 10 years, the amount invested in each plan was Rs 12 lakh.

We were trying to answer two simple questions:

Is there a meaningful difference in returns between Direct and Regular Plans?

If there is, how does that difference develop over time?

To make the comparison broad-based, we selected funds from multiple categories:

UTI Nifty Index Fund

Nippon India Large Cap Fund

SBI Small Cap Fund

HDFC Mid-Cap Opportunities Fund

Aditya Birla Sun Life Bond Fund

For each fund, we compared the direct and regular versions of the same scheme. Since the underlying portfolio and fund manager remain identical, any difference in performance would come from the difference in costs between the two plans.

By looking across equity, index, and debt funds, we wanted to see whether the gap was consistent over time and over categories.

Results

Across all the categories, Direct Plans performed better than the Regular Plan counterparts.

This result is not particularly surprising. Since Direct Plans have lower expense ratios, a smaller portion of the portfolio is deducted as fees each year. While the difference may appear small initially, it compounds over time and gradually widens the gap in returns.

The gap in the returns varied significantly across categories.

For the debt and index funds, the difference was relatively modest, with the Direct Plan generating roughly Rs 15,000 more on a Rs 10 lakh portfolio over 10 years.

However, in actively managed equity funds, the gap was much larger, ranging from Rs 1.5 lakh to Rs 2 lakh over 10 years.

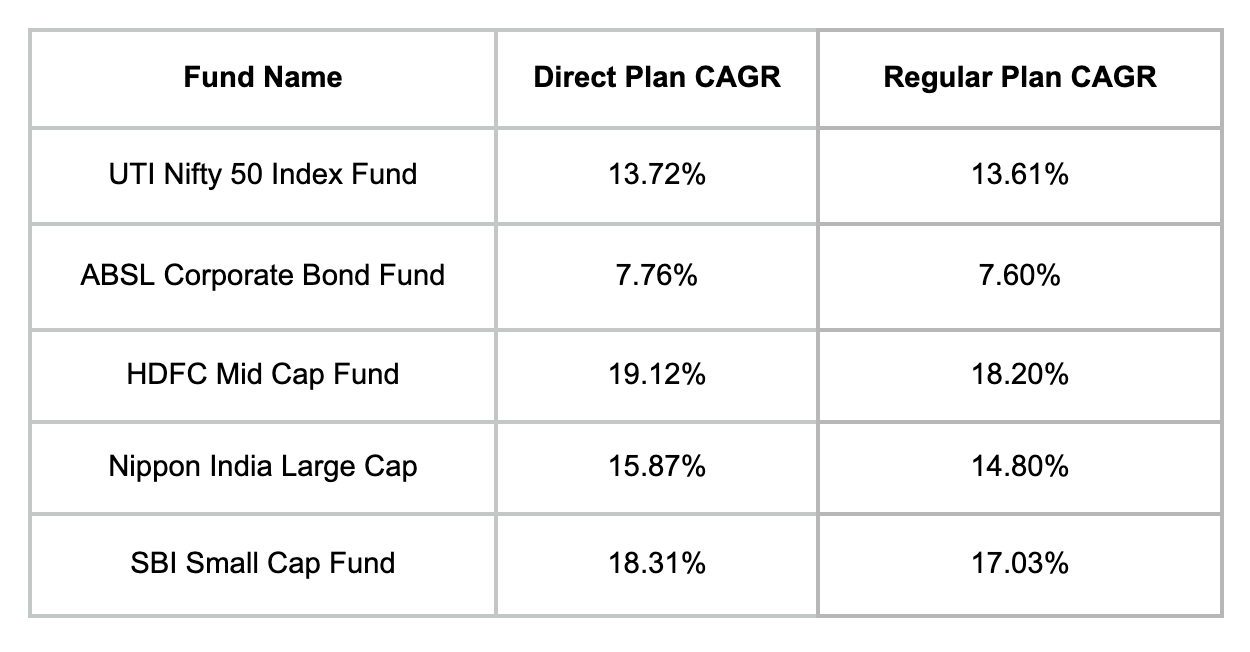

This difference can be seen by looking at the CAGR too.

The differences between Direct and Regular Plans may appear small on an annual basis often around 0.1% to 1.3% points but when compounded over a decade, they can translate into meaningful differences in final portfolio value.

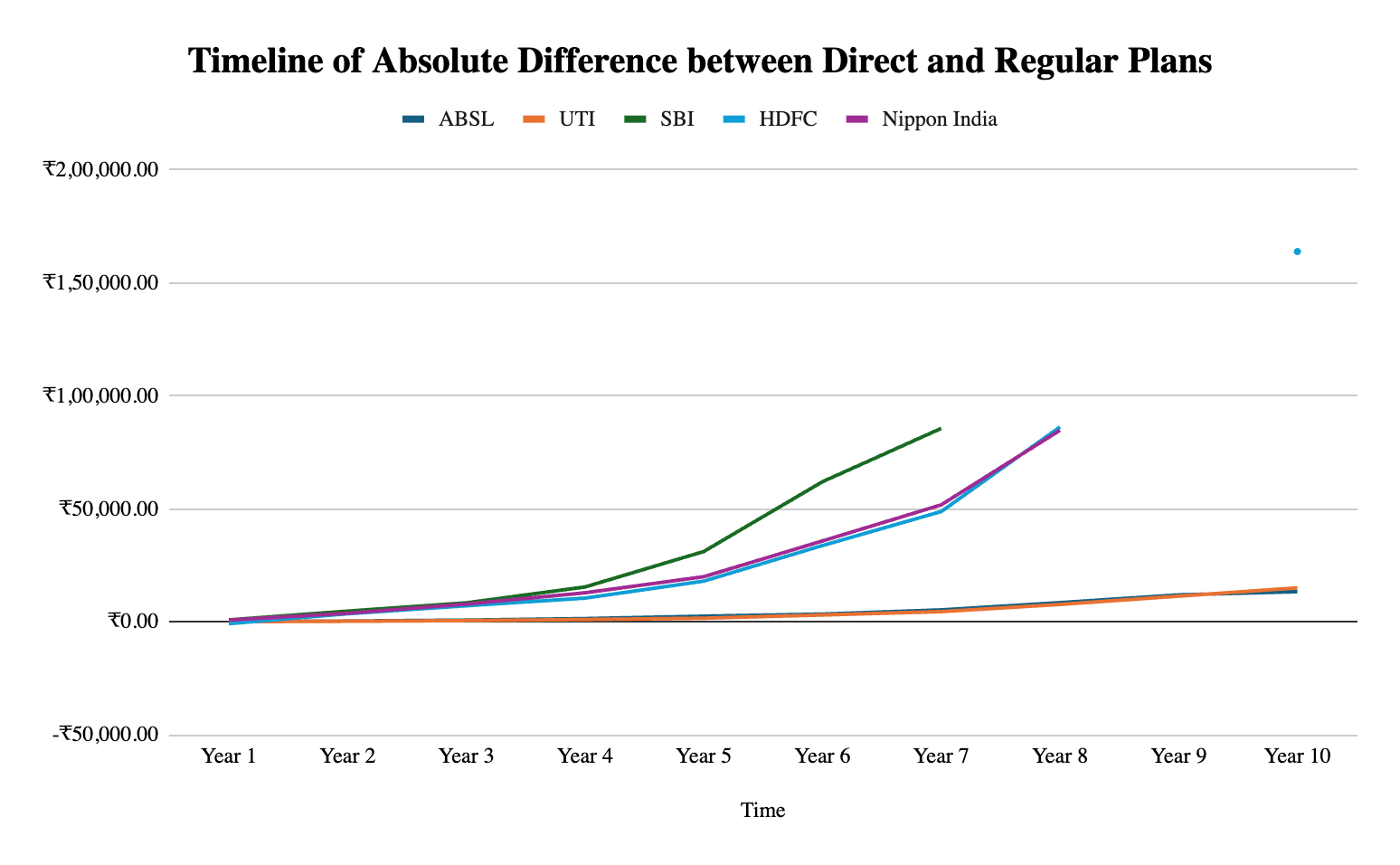

How does this difference accumulate?

The graph below shows how the difference between the Direct and Regular plans forms over time. The gap does not grow in a straight line.

In the initial years, the difference is barely noticeable. For most funds, the gap is only a few hundred or a few thousand Rupees. This is insignificant, compared to the amount invested.

However, as time passes, the gap begins to widen at an accelerating pace. This happens because the money saved through lower expenses in a Direct Plan remains invested and earns returns of its own. Those additional returns then generate further returns, creating a compounding effect.

This is especially visible in the equity funds. What starts as a relatively small difference in the early years gradually rises into a significant gap by the end of the decade.

The debt and index funds follow the same pattern, although the graphs are less dramatic because their return profiles and expense differences are lower.

The key takeaway is that costs compound just like returns do. A seemingly small annual expense difference may not feel important in year one, but over long investment horizons it can create a meaningful difference in final wealth.

Why do investors invest through Regular Plans?

Given that Direct Plans generated higher returns across every category we tested, one might assume that everyone in India is flocking to them. However, the reality of the Indian mutual fund industry is more nuanced.

India has a population of over 1.4 billion, but according to data from AMFI, there are currently only about 5 crore unique mutual fund investors.

That means only about 3.5% to 4% of the Indian population currently invests in mutual funds.

Despite the rapid growth of the industry, mutual fund penetration in India remains relatively low compared to developed markets. For many people, investing is still seen as a complex and intimidating process.

This helps explain why Regular Plans continue to dominate the industry, accounting for roughly 60% of total mutual fund assets under management.

For many first-time investors, selecting funds, understanding risk, completing KYC requirements, and making decisions can be overwhelming or simply inaccessible.

This is where distributors, advisors, and banks play an important role.

They help investors get started, recommend funds, handle paperwork, and provide guidance during periods of market uncertainty.

It is also worth remembering that Direct Plans are a relatively recent addition to the Indian mutual fund landscape. They were introduced by SEBI only in 2013.

For decades before that, distributors and advisors were the primary channel through which investors accessed mutual funds, playing a key role in expanding the industry’s reach across the country.

Conclusion

Ultimately, choosing between a Direct and Regular mutual fund comes back to the food delivery analogy.

Regular Plans charge a higher expense ratio because part of that cost goes towards distributors, advisors, and the services they provide. For many investors, especially those who are new to investing or prefer professional guidance, that additional cost may be well worth paying.

Direct Plans, on the other hand, are designed for investors who are comfortable making their own investment decisions and managing their portfolios independently.

As our 10-year experiment shows, this small difference in expenses can compound into a gap in wealth over the long term.

However, costs are only one part of the equation. Staying invested through market cycles proves to be more important than saving a fraction of a percent in fees.

Ultimately, it comes down to the investor’s experience, confidence, and ability to manage investments independently.

The right choice is not necessarily the one with the lowest cost, but the one that works best for the investor and helps them stay invested for the long term.

Limitations of the Experiment

Past performance is not a guarantee of future returns: The results are based on the last 10 years. The gap between Direct and Regular Plans may be different in the future.

Expense ratios can change: Fund houses regularly revise their expense ratios. As a result, the difference between Direct and Regular Plans may widen or narrow over time.

Investor behaviour matters: This analysis assumes both investors stay invested for the entire period. In reality, an advisor may help an investor avoid panic-selling or stay disciplined during market downturns.

Switching plans may have costs: Investors moving from a Regular Plan to a Direct Plan could face taxes or exit loads, which are not included in this analysis.

Limited history: Direct Plans were introduced only in 2013, so it is not possible to compare their performance across older market cycles.

Great research !!

People often overlook a 1% difference in expense ratios, but when compounded over 15–20 years, it eats away a massive chunk of the final wealth. Direct funds are a game-changer for long-term compounding.

I m mutual fund distributor, Clint commit lotnof mistake in choosing the fund for right risk period