What if you invest in the worst performing mutual fund every year? How will it affect your returns?

It is normal for an investor to spend some time looking for the best mutual fund to invest in.

Investors compare past returns, check ratings, read recommendations, and usually avoid funds that have recently performed poorly.

That instinct feels reasonable.

After all, if a fund has not given good returns in recent times, why would anyone want to put money into it?

But what if an investor ended up investing in a poorly performing fund?

Would that decision seriously damage long-term wealth?

We decided to put this to the test.

Instead of picking winners, we built a strategy that does the opposite. Every year, it invests in the lowest-performing large-cap mutual fund from the previous year.

In a way, this represents the unluckiest investor. Someone who consistently ends up in the weakest fund on the list, year after year.

What happens to their wealth over time?

The Experiment

We established a clear set of rules.

The universe was limited to Large Cap mutual funds that had existed for at least 10 years.

On 1st January of every year, the investor would:

Identify the lowest performing large cap fund from the previous calendar year

Invest Rs 1 lakh into that fund

Repeat the same process every year for the next 10 years

For example, after identifying the lowest performing fund of 2015, the investor will invest in it in 2016. In 2017, the investor will invest in the lowest performing fund of 2016, and so on…

Also, throughout the 10 years, no selling will take place. If the lowest performing fund changed the next year, the earlier investment would remain untouched. A fresh Rs 1 lakh would simply go into the newly identified lowest performer.

This avoided taxes, exit loads, and unnecessary churn.

We ran the experiment starting from Jan 2016 to Dec 2025, a period of 10 calendar years.

Finally, as a benchmark, we compared this strategy against an index fund investor who put Rs 1 lakh into the UTI Nifty Index Fund on the same days.

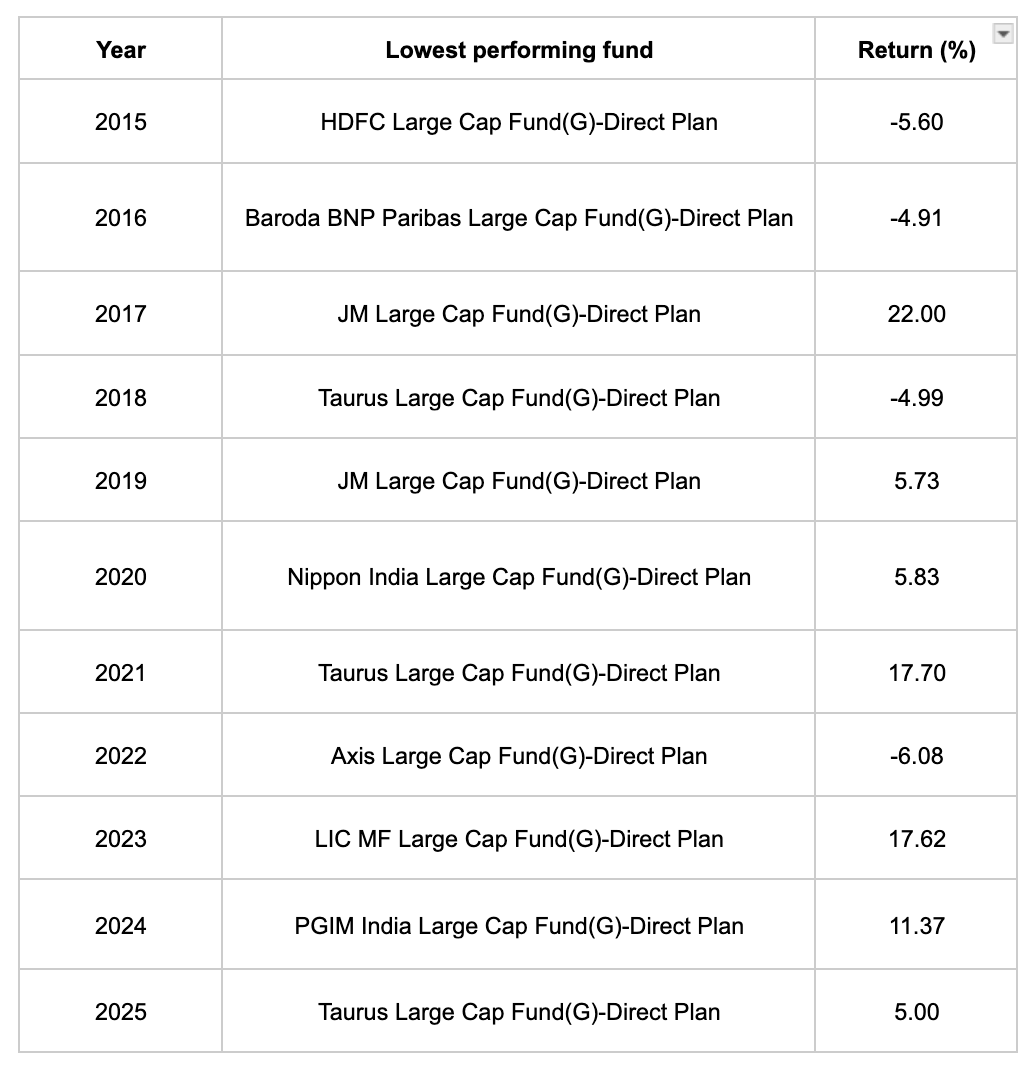

Lowest Performing Funds Each Year

One thing becomes obvious immediately. No single fund stays at the bottom forever.

Some names appear multiple times, but the rankings constantly change depending on market cycles, portfolio decisions, etc.

It is also interesting to note that the lowest returns vary drastically depending on how the broader market performed that year. During strong bull market years like 2021 and 2023, even the lowest-performing large-cap funds still delivered double-digit returns (~17%).

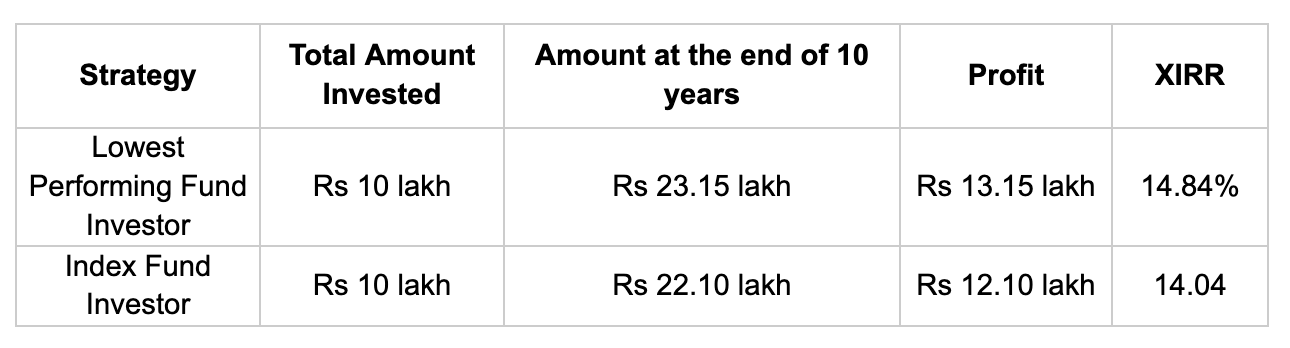

Results

The result was surprising.

The strategy of investing in the previous year’s lowest performing large cap fund actually ended up outperforming the index fund over the 10-year period.

It was not significant.

But enough to challenge the assumption that the lowest performer automatically means that it is a bad investment.

Why Did This Happen?

In mutual funds, short-term underperformance does not always mean the fund is weak.

A fund can underperform simply because it did not own the stocks that were driving the market during that period. It may have held different sectors, avoided overheated stocks, or maintained cash while others stayed fully invested.

As the market experiences changes, the performance of the fund undergoes changes too.

This experiment also shows something important about large cap funds. Even the lowest performing fund in the category is mostly invested in large, established companies. It may lag behind other funds, but it is not taking extreme bets or investing in weak businesses.

Because of this, poor short-term performance does not automatically translate into long-term damage.

Also, remember that we have not considered any costs in this experiment. And while the fund’s expense ratio is already factored into the returns we calculated, other charges (if applicable) could slightly alter the exact final numbers.

Conclusion

Ultimately, this experiment reveals a highly comforting truth for everyday investors: a period of underperformance in your portfolio will not permanently destroy your wealth.

Even if you happen to invest in a fund that goes through a rough patch, it does not mean your returns are doomed. Because of market cycles (and in this case, the safety of established large-cap companies), today’s underperformers may often bounce back in the future.

The key to the strategy’s success was simple: the investor stayed in the market.

The anxiety we often feel about picking the ‘perfect’ mutual fund is largely misplaced.

We saw here that even if you possessed the worst luck imaginable, where you blindly picked the absolute bottom-ranked large-cap fund every single year for a decade, the compounding power of the broader Indian stock market still more than doubled your money. It even outperformed the index fund by a small margin.

To be clear, the takeaway isn’t that you should actively seek out poorly performing funds.

You should always do your due diligence before investing. It is just that an underperforming fund may not necessarily be a wealth destroyer, as long as you stay invested.

At the end of the day, consistently investing and staying in the market matters far more than perfectly timing or picking the absolute best fund.

Limitations of the Experiment

The study is limited to large cap mutual funds, which are relatively stable and diversified. Results may not hold in small cap or sector funds where volatility is much higher.

It uses a simplified selection rule of picking the previous year’s worst performing fund, without analysing why it underperformed or whether conditions were temporary or structural.

The strategy assumes no selling at all, which removes real-world behaviour like profit booking, rebalancing, or exiting underperforming funds.

It ignores taxes, exit loads, and transaction costs, which would reduce actual investor returns in practice.

It is based on historical hindsight data, meaning the selection is easier in hindsight than it would be in real-time decision making.

The holding period assumes long-term patience every time, which may not match how most investors actually behave during underperformance periods.

It does not account for fund closures, mergers, or category changes, which can affect real-world portfolio continuity.

The experiment uses a Rs 1 lakh lump sum at the start of every year, which makes timing very sensitive. In reality, SIPs spread investments over the year, reducing timing impact.

Overall, the strategy used here is a controlled thought experiment, not a practical investing strategy.

What if you can replicate this experiment for mid cap funds. By logic the funds may hold midcap names which are yet to rise and may show potential in future. It will be interesting to see the results of both purely midcap and small cap funds

I liked the experiment. Expected to see such innovative articles in the future