Two flights leaving Mumbai for Delhi at almost the same time can take noticeably different paths through the sky.

One might fly higher to catch a tailwind. Another might route slightly west to avoid turbulence. One pilot may be asked to slow down because Delhi airport is crowded. Another might be given a clearance to land.

The flight times may vary slightly. But none of this is visible to the passenger.

And then both planes land, within minutes of each other, at the same terminal.

The paths were different. The destination was the same.

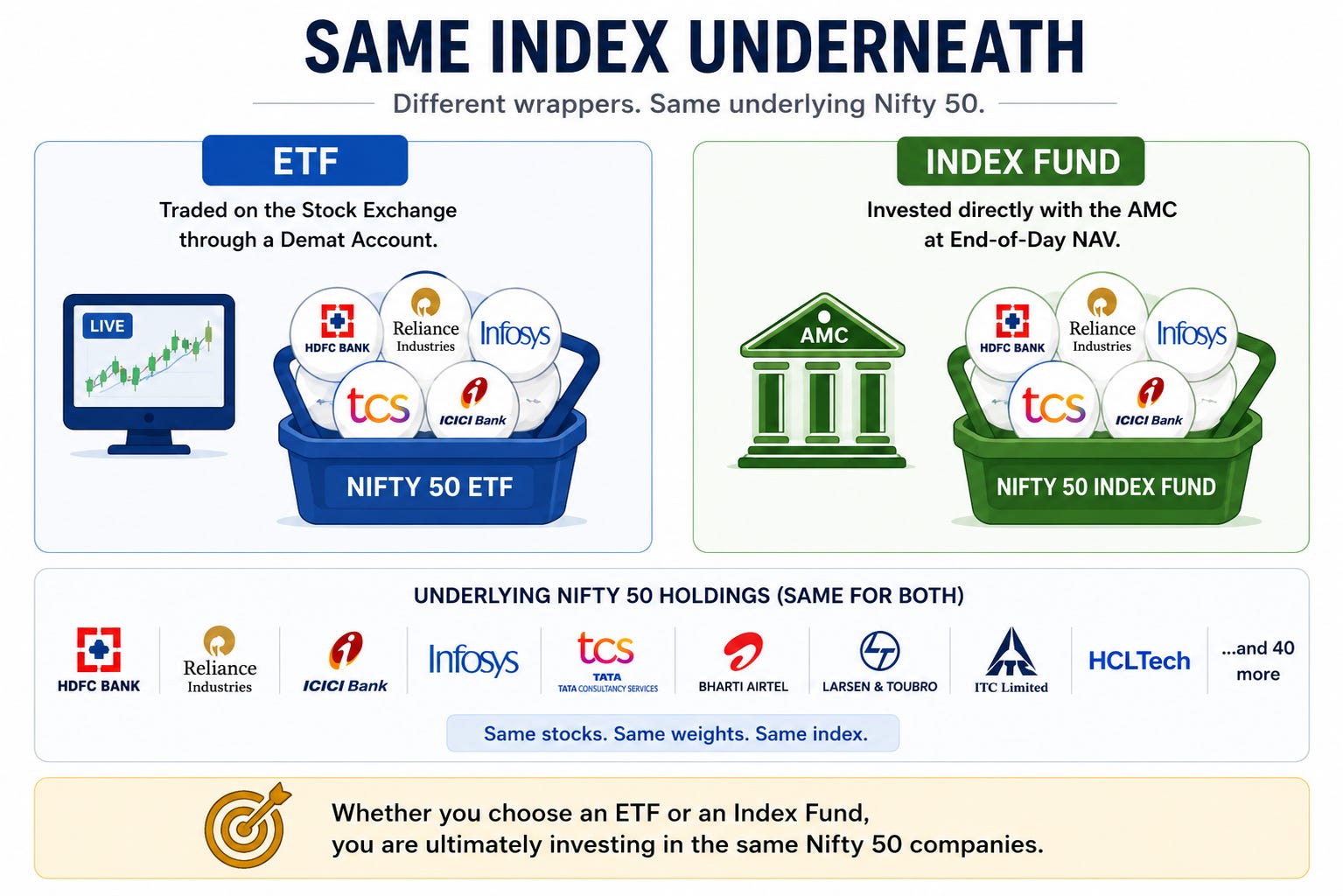

ETFs and index funds behave similarly.

Both are trying to do the exact same thing: track the Nifty 50.

But the path they take is slightly different.

An ETF trades on the stock exchange in real time, which means its price keeps changing every second the market is open. When someone buys an ETF, they are buying it at the price the market is offering at that moment.

An index fund works differently. You place an order anytime before the cut-off time, usually around 3 PM, and after the market closes, the fund calculates the exact value of all the stocks it holds. Every investor who placed an order that day receives units at that same end-of-day price.

Even though both products are trying to track the same index, the way they function underneath is slightly different.

An ETF behaves more like a stock because it trades continuously on the exchange, while an index fund behaves more like a traditional mutual fund where transactions happen directly with the fund house.

But despite these differences, both are trying to mirror the performance of the Nifty 50

We decided to find out if the path taken actually makes a difference.

The Experiment

To make the comparison as fair as possible, we selected two passive investing setups where both the ETF and the index fund came from the same AMC.

The study covers September 2015 to May 2026, a period of approximately ten years and four months.

The pairs were:

SBI Nifty ETF vs SBI Nifty Index Fund

UTI Nifty ETF vs UTI Nifty Index Fund

This was important because we did not want differences in fund houses, fund management styles, or benchmark methodology affecting the results.

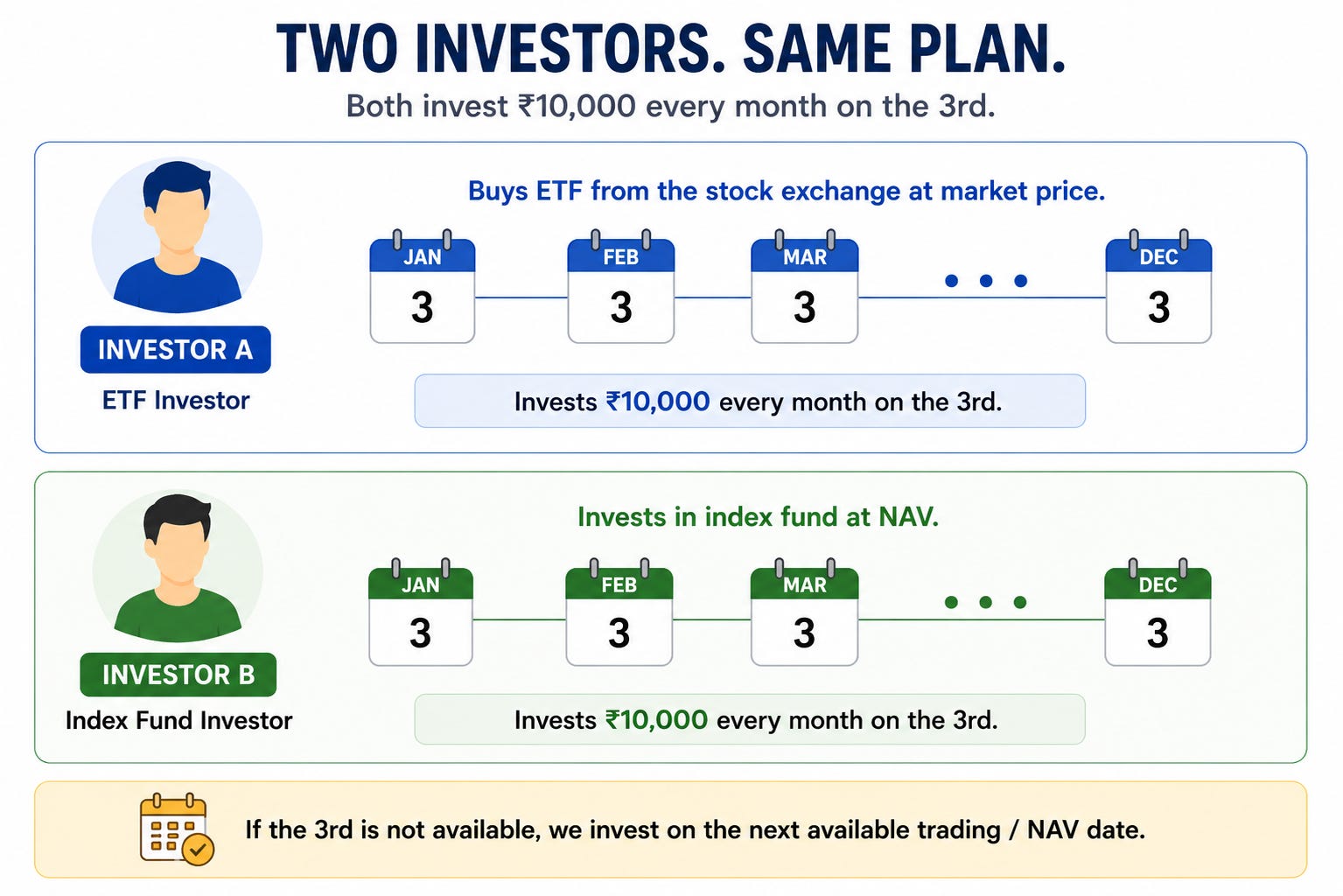

Then we simulated two investors.

Investor A: The ETF Investor

Every month, Investor A buys ETF units directly from the stock exchange at market price.

The closing market price on the SIP date was used as the purchase price for all ETF transactions.

Brokerage and STT costs on ETF purchases have not been factored into this study. Including these would widen the gap slightly further in favour of the index fund.

Investor B: The Index Fund Investor

Investor B invests in the matching index fund and receives units at NAV.

Both investors:

invested Rs 10,000 every month

followed a SIP on the 3rd of every month

stayed invested through the full study period

The Results

The gap turned out to be much smaller than most people would expect.

Both ETFs and index funds tracked the same Nifty index. And after ten years of monthly investing, the final outcomes were almost identical.

But not perfectly identical.

Similar to the two flights that took different routes and landed within minutes of each other.

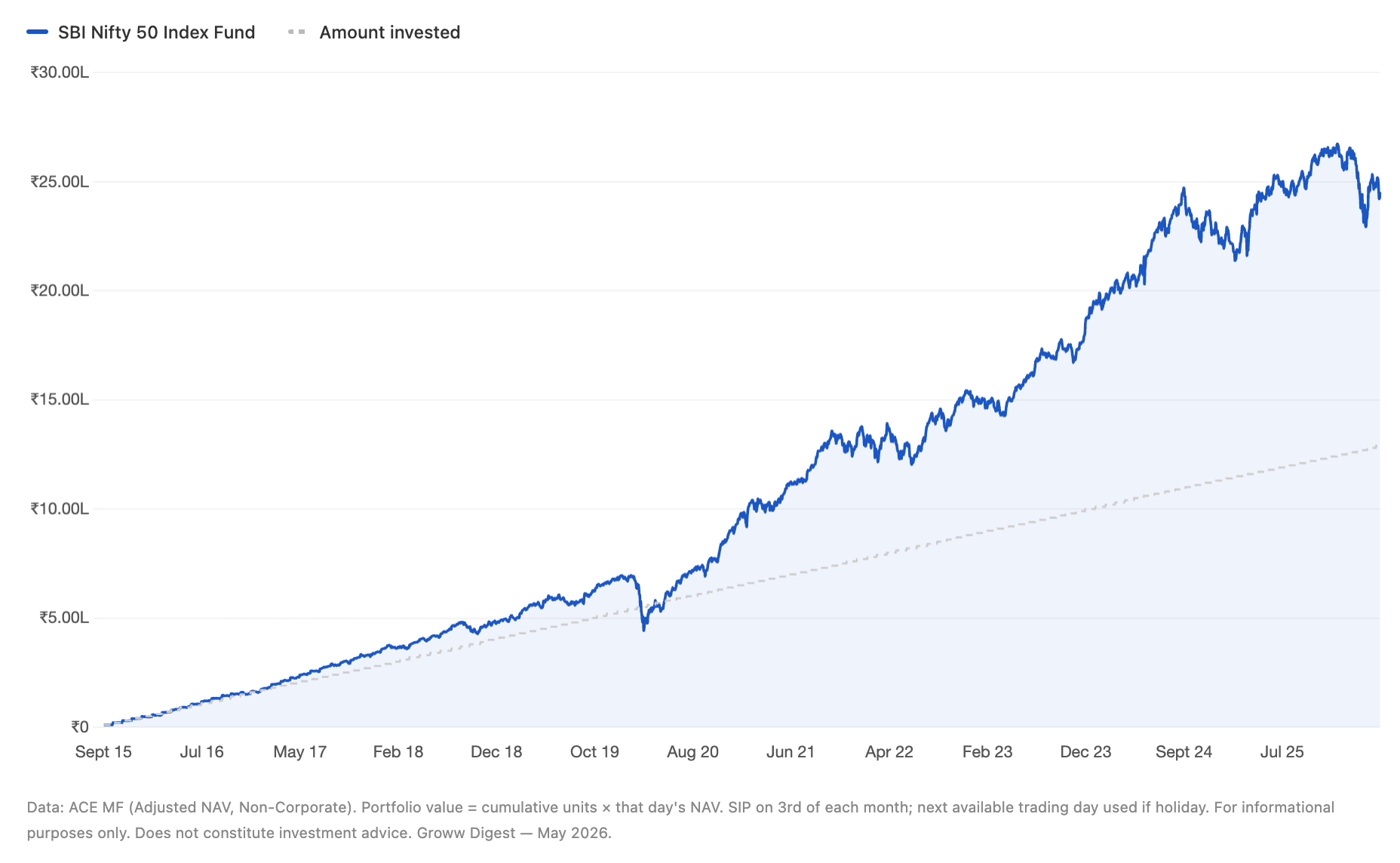

SBI: ETF vs Index Fund

Both investors started investing Rs 10,000 every month. One bought the SBI Nifty ETF from the stock exchange at market price. The other invested in the SBI Nifty Index Fund at NAV.

Over the full study period:

The index fund finished ahead by roughly Rs 21,000.

Not a huge difference.

But still enough to show that even when both products track the same index, the investor outcome was not perfectly identical.

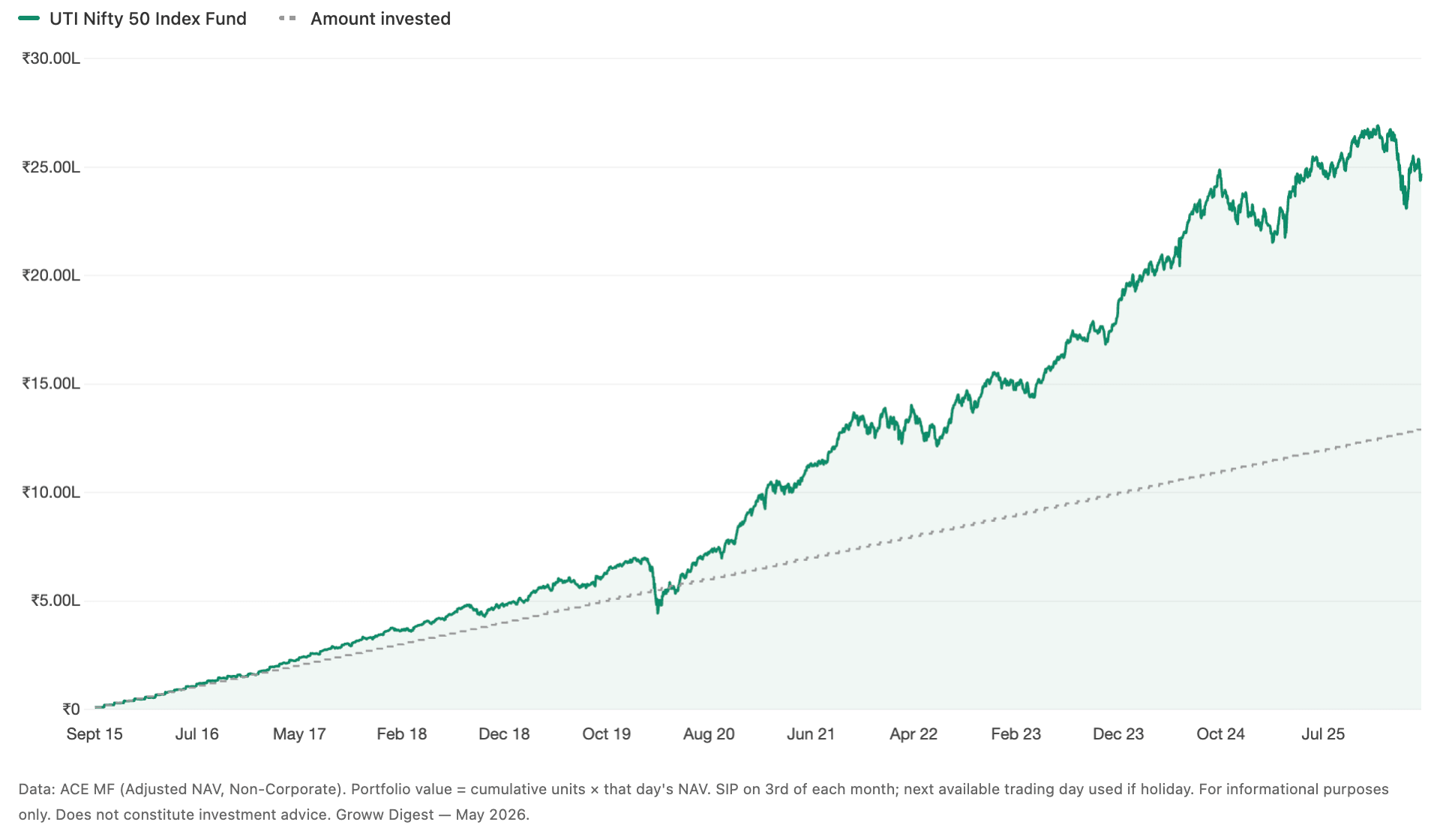

UTI: ETF vs Index Fund

Then we repeated the exact same experiment using UTI products.

And once again, the results were extremely close.

The index fund again finished slightly ahead.

This time by around Rs 15,000.

Which is interesting. Because it suggests the SBI result was not a one-off. In a different AMC, with a different set of SIP execution dates, the same broad pattern appeared again.

Why did the index funds slightly outperform?

The study does not suggest ETFs are bad investments.

In fact, the more interesting takeaway is probably the opposite.

Despite operating through slightly different systems for many years, both the ETF and index fund portfolios ended up remarkably close to each other. That itself says a lot about how efficient passive investing has become in India.

But the study did reveal something subtle.

Two products tracking the exact same index are still not perfectly identical in real-world investing.

Because investment returns are influenced not only by what you own, but also how you access it.

An index fund investor deals directly with the fund house. At the end of the day, the AMC calculates the exact value of all the underlying stocks and gives every investor units at that same NAV.

An ETF investor, meanwhile, interacts with the stock market itself. The ETF trades live during market hours, and its price depends on ongoing buying and selling activity in the market.

That introduces very small inefficiencies along the way.

Sometimes the ETF may trade slightly above its actual value. Sometimes slightly below. Sometimes there may not be enough trading activity at the exact moment an SIP order gets executed. Sometimes the buying price and selling price in the market may not perfectly match.

Individually, these differences are tiny and almost invisible on any single day.

But SIP investing works through repetition.

When something repeats every month for ten years, even tiny differences slowly start compounding.

Enough to create small differences in the final portfolio value.

It is also worth noting that the specific funds chosen may have had slightly different tracking efficiencies relative to the Nifty 50 during this period.

This study does not claim that index funds as a category always outperform ETFs. It only tells that in these two specific fund pairs, over this specific period, the outcomes differed slightly.

So who should choose ETFs?

The study did not find ETFs to be meaningfully worse. The gap was small, but it did reveal where friction tends to accumulate, which helps clarify who each product naturally suits.

Since ETFs trade like stocks, they offer a level of flexibility that traditional index funds cannot.

An ETF investor can buy during market hours, place limit orders at specific prices, react instantly during sharp market falls, or move money quickly between different asset classes.

For investors who actively manage allocations or prefer more control over execution, these features can genuinely be useful.

Index funds, however, may suit a very different type of investor.

They work especially well for people who primarily invest through SIPs, prefer simplicity, and do not want to think about market prices, trading windows, liquidity, or execution timing every month.

You simply invest the money and receive units at the day’s NAV directly from the fund house. The process is automatic, predictable and operationally simple.

The study suggests that operational simplicity can matter alongside expense ratios.

Because long-term investing is not only about finding the theoretically perfect product.

It is also about finding the system that works most smoothly for the investor using it month after month for many years.

The Real Takeaway

Both investors still ended up in almost the same place after ten years.

For long-term passive investing, the structure matters far less than simply staying invested consistently for many years.

The ETF investor and the index fund investor both captured the same thing in the end. That is long-term growth of the Indian equity market.

They just travelled through slightly different systems to get there.

Note:

This study uses closing ETF closing market prices for SIP purchases. In real life, investors may buy at slightly different prices during the trading day.

Brokerage, STT, and demat-related costs on ETF transactions were not included. Depending on the platform used, these costs could slightly reduce ETF returns further.

The study compares only two AMC pairs (SBI and UTI) because they had the longest available historical data. Results may differ for other ETFs, index funds, or different time periods.

Some part of the return difference may also come from how efficiently each individual fund tracked the Nifty 50, not just from the ETF vs index fund structure itself.

The study period runs from September 2015 to May 2026, which includes major market phases like the COVID crash and recovery. Results during other market periods may differ.

Comnsidering the taxes and brokerage charges, which is better at the end while we are withdrawing funds