Sameer was a bright and smart kid, and why not, he cracked the IIT entrance exam and bagged a seat at the prestigious IIT Bombay.

He became a star alumnus at his school and coaching class, simultaneously inspiring awe and jealousy among his neighbours and relatives.

After all, getting into an IIT is ‘the’ big achievement in the social circle called ‘middle class’.

But as years passed by, things didn’t go as everyone expected it to.

Sameer’s academic radiance gradually faded and he failed multiple exams in college, he barely managed to clear his backlogs to get a degree.

The year he passed out, the college had a placement rate of 90%, which is impressive, but poor Sameer fell into the left out 10%.

There are many Sameers out there, telling us that near term achievement may not be a sign of long term success.

The same principle applies for investing as well.

Let’s take Nifty 50 for an example, the companies that enter this index command the highest rank in the Indian markets.

Almost every year, multiple stocks enter and exit the Nifty 50, which is the flagship index of NSE, and is also considered a barometer for the Indian economy.

Stocks entering this index attract a lot of investment and credibility.

So we tried testing a simple hypothesis.

What if we invested in every new company that entered the Nifty 50?

In short, we will invest in every Sameer who enters IIT — believing that a company that enters Nifty 50 would be doing something very right.

So we looked into the period between January 2015 to December 2024, almost 10 years.

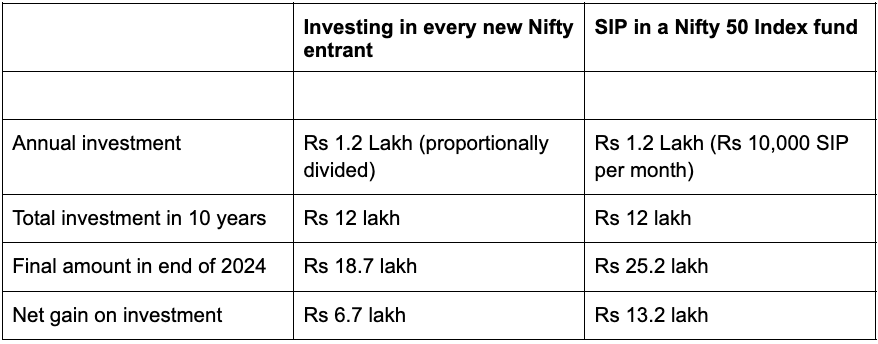

For each year, we proportionally invested Rs 1,20,000 in stocks entering the Nifty 50.

For example, if 4 stocks entered the Nifty during a year, we allocated Rs 30,000 (Rs 1,20,000 ÷ 4) in each of them.

If just one stock entered the index that year, the entire Rs 1.2 lakh went into it on the day of reconstitution.

Whichever stock we bought, we held it till the end of 2024.

We chose the amount of Rs 1,20,000 as we will be comparing this investment with a monthly SIP of Rs 10,000 in a Nifty 50 index fund during the same period, which will be Rs 1,20,000 annually.

Thus giving us a better idea of the overall investment performance.

By following this logic, a total of Rs 12 lakh was invested across 29 stocks in a 10 year period.

By the end of 2024, the investment value stood at Rs 18.7 Lakh, giving a net gain of Rs 6.7 lakh (Rs 18.7 lakh - Rs 12 lakh = Rs 6.7 lakh).

It looks fine, until you compare it with something simpler.

If one would have done a simple monthly SIP of Rs Rs 10,000 (Rs 1.2 lakh annually) in a Nifty 50 Index Fund, the investment value at the end of 2024 would have been Rs 25.2 lakh.

A net gain of Rs 13.2 lakh (Rs 25.2 lakh - Rs 12 lakh = Rs 13.2 lakh).

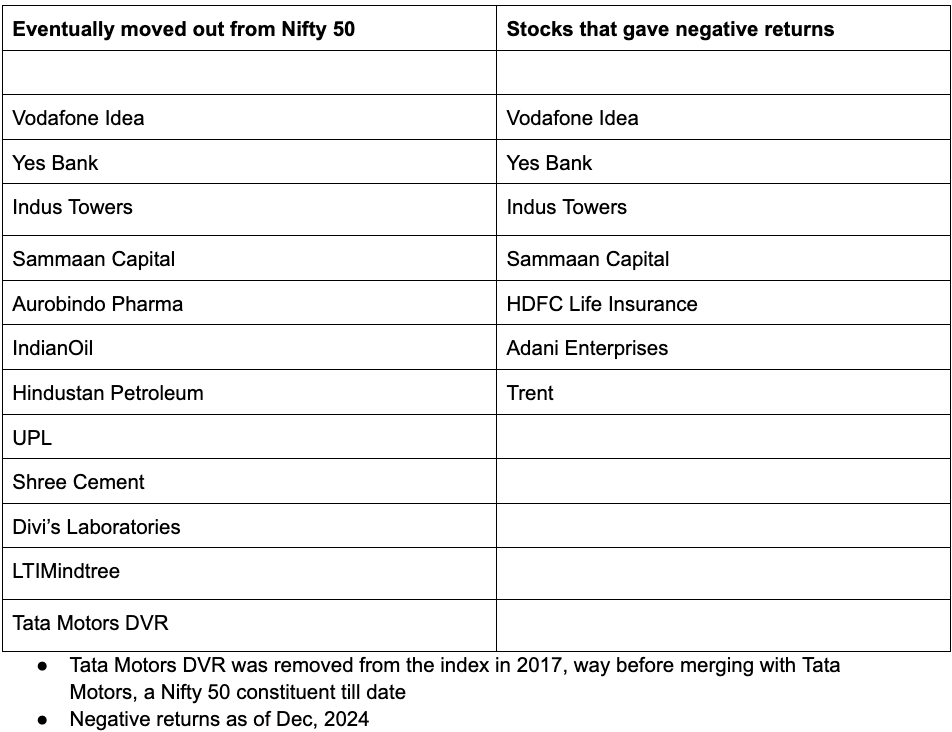

On top of it, 12 out of 29 stocks that entered Nifty 50 between 2015 and 2024 didn’t retain their position and eventually moved out of the index.

And 7 of these 29 stocks gave a net negative return since entering the index.

This makes us ponder over 2 things:

First, short-term achievers can’t really help us judge long-term winners

Second, a simple SIP in an index fund managed to effortlessly beat this complicated investment strategy

What do you think?

While this was just a playful attempt to understand a ‘What if’ scenario, let us know in the comments if you feel we missed out on something.

Note:

UTI Nifty 50 Mutual Fund Direct - Growth has been used to calculate the Nifty 50 index fund returns

Transaction costs (brokerage, GST, STT, etc) have not been accounted for the sake of simplicity

The stocks picked would have also given dividend, which has not been included in the total returns of the active stock investment

SIP investment started from Jan-2015, while the active stock investment began from March-2015, as the Nifty 50 reconstitution happens bi-yearly around March and September.

Though a few exemptions may exist due to reasons like delisting of an existing stock, etc.

Investment in Tata Motors DVR didn’t reach Dec-2024, as the stock got delisted in Aug-2024

If we rebalance for every six months, then what result we can expect? Illustration : First investment in Mar-2015, we invest Rs.60,000 and in next round we sold those stocks which invested previous round and reinvest including fresh Rs.60,000 in new entrants equally by dividing total corpus from total number of companies. Again in third round we sold all our stocks we hold and reinvest including fresh Rs. 60,000 in new entrants. This system will apply every six months. If there is no new entry of stock, then there is no sale and no new purchase. Then what will be the return?