What if you only invested in companies with high revenue growth?

The idea seems easy and simple; many investors might have toyed with.

What if I just pick companies that have shown strong revenue growth in the past?

If a company’s revenues have been growing fast for years, that should mean it’s doing well, right? So shouldn’t its stock’s price also keep rising over time?

We tried to find out exactly that in this short study.

We picked some large-cap companies that showed the highest revenue growth between 2010 and 2015, which were the top performers of that era.

Then, we simulated what would have happened if someone invested in these same companies at the end of 2015 and held them for the next 10 years, i.e., till 2025.

The question we wanted to answer was simple:

Did these “fast-growing” companies continue to grow, and did their share prices reflect that growth?

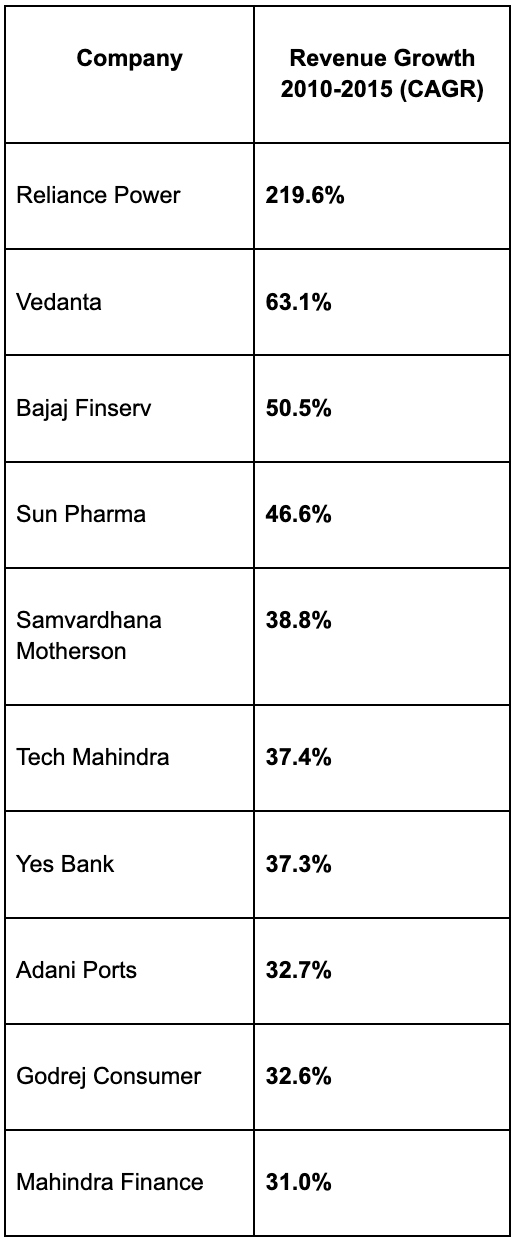

We found the below companies that has the maximum revenue growth in the 2010-2015 period:

Across the sample size, the average revenue growth between 2010-2015 was a massive ~59% CAGR.

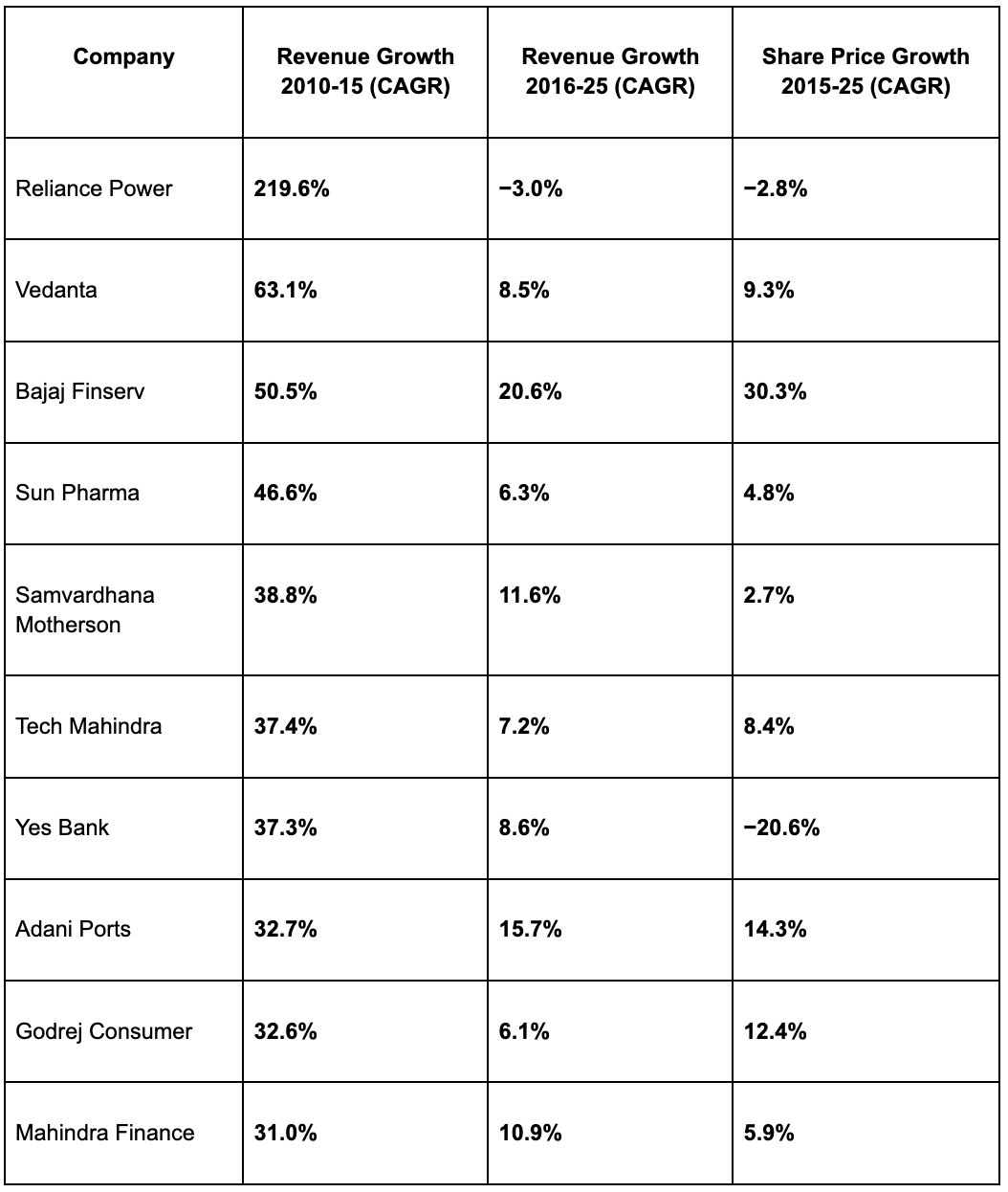

But during the next decade (2016-2025), that number fell sharply to ~9% CAGR. The average share price growth during the same period came to just ~6.5% CAGR.

This means most companies that once grew very fast eventually slowed down drastically.

Here are the full results:

Let us look at some examples:

Reliance Power: Had a whopping 219% CAGR revenue growth from 2010 to 2015 but saw its revenues fall and share price decline later.

Bajaj Finserv: More moderate growth of around 50% CAGR earlier, but managed to sustain healthy growth ahead, resulting in a 30% CAGR in share price from 2015 to 2025.

Yes Bank: High revenue growth in early years, but a slowdown in both fundamentals and share value later (-20% CAGR).

The pattern is clear: consistent growth mattered more than just past high growth.

There is no pattern to be seen in revenue growth alone.

Here are some brief pointers to keep in mind:

High past growth doesn’t guarantee future success: Once companies mature or hit saturation, their growth naturally slows.

Valuations catch up: Markets often value companies highly early on, which means there’s less room for their stock prices to grow significantly later.

Consistency beats speed: Companies that maintained moderate but steady growth ended up rewarding investors more over time.

So, should you chase past growth?

Not really.

It’s really tempting to look at a 5-year growth chart and assume the trend will continue. But this study shows that past growth often fades, and what matters more is sustained profitability and competitive advantage.

If you had simply picked companies based on their 2010 to 2015 revenue growth, your portfolio’s returns over the next decade would likely have underperformed those that focused on quality and steady performers, or simply below the Nifty 50 index.

There’s nothing wrong with liking fast-growing businesses — but history alone can’t predict the future.