Most people don’t have a massive pile of cash just sitting in the bank, ready to be invested or spent on a big purchase.

But we all dream about big goals — a car, a house, or just a financial cushion that gives peace of mind.

So how do ordinary investors go about achieving these goals?

Today, most investors rely on steady monthly SIPs, building wealth bit by bit.

Others choose to invest a large sum at once, letting it compound over time. This could be money they already have or a windfall, be it from inheritance, FD returns, or selling an asset that allows them to put a significant lumpsum to work and watch it grow.

But here’s the catch.

A lumpsum investment usually has a massive head start.

Since the entire amount is invested on day 1, every single rupee benefits from compounding for the full duration.

An SIP, by definition, starts small. While it reduces risk, your later installments simply have less time to grow.

So a lumpsum investment often gives higher returns than a SIP over the same period.

That’s because the money gets invested all at once, letting the entire amount grow together and take full advantage of compounding.

An SIP, on the other hand, spreads investments over months or years, reducing risk but also delaying the full benefit of compounding. Inflation and the decreasing value of money over time further widen the gap.

So, if you are a SIP investor, the question arises: how can you accumulate the same wealth that a lumpsum investment can generate?

Specifically, how much would your SIPs need to increase each year to match a lumpsum investment?

We ran an experiment to find that out.

The Experiment

We tracked the UTI Nifty 50 Index Fund from January 2016 to December 2025, a period of 120 months. We compared two investors starting at the exact same time.

The Lumpsum Investor: Invests Rs 10 lakh on day 1.

The SIP Investor: Invests Rs 10,000 every month.

After a 10 year period, these were the results

Even though the SIP investor put in Rs 2 Lakhs more of their own money, they ended up with Rs 10.87 lakhs less than the lumpsum investor.

Why?

This is because the lumpsum investor bought all their units when the NAV was very low, in Jan 2016. The SIP investor had to buy units as the NAV value climbed up slowly, almost 4x times the original NAV.

This means to generate the same wealth as the lumpsum investor, the SIP investor has to step up the money invested.

Closing the Wealth Gap

This can be done in 2 ways.

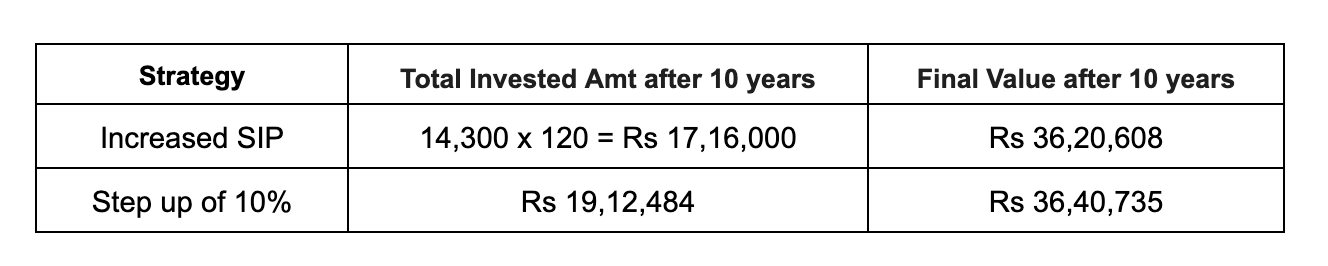

The Increased SIP: Start with a higher SIP amount of Rs 14,300 and keep it constant over the 10 years.

The Step-Up SIP: This is the more practical option. Start with an SIP of Rs 10,000 and increase the amount by 10% every year as your income grows.

The increased SIP of Rs 14,300 or a 10% step up every year will eventually match or even beat the Rs 10 Lakh lumpsum investment.

But notice the profit made. To get the same wealth of Rs 36 lakhs, you ended up paying nearly Rs 7 lakhs to Rs 9 lakhs more than the lumpsum investor.

Instead of 10 lakh, you end up paying a lot more.

Conclusion

Why do you pay more to reach the same level of wealth?

This is because your money starts ‘working’ later.

For the lumpsum investor every rupee compounds for the full 10 years.

Time does the heavy lifting, so less capital is needed to reach the same wealth. But, this comes with risk: any major falls in the market, and the entire corpus would take a hit.

Most of us don’t have Rs 10 lakhs ready to invest today, but we do have a future salary.

This is where the SIP wins: the feasibility. The SIP investor spreads investments over 120 months, which reduces the risk too.

Later contributions have less time to compound, which is why more total capital is required to reach the same wealth.

The Step-up SIP shows how gradually increasing contributions can close the gap over time, letting SIP portfolios nearly match lumpsum outcomes while keeping risk spread out — and helping long-term financial goals stay within reach.

Limitations of the Experiment

Historical Data: This experiment is based on past market performance (2016-2025) where the market has risen. Markets may behave differently in the future.

Market Risk: There’s always risk in investing. A market drop could change the outcome.

Money invested later in a SIP has less value than money invested earlier because of inflation.

Discipline: Any type of SIP requires consistent contributions over many years, which may be hard to maintain.

Taxes: for this experiment, we have not taken into account taxes or any other costs that would affect the portfolio.

Comparison is flawed, the better would be to start in both the cases with same amount and the amount still available with SIP in a fixed income instrument like FD, then only it would be comparable. For example, the last 10,000 installment almost remain available for 10 years which could be invested in FD and likewise, a calculation can be made for all installment.

Better suggestion