Elevators have existed for thousands of years.

Elevators (or lifts) were used for hoisting goods.

What’s peculiar about elevators is that despite being thousands of years old, they were almost never popular for transporting people.

The chances of ropes snapping were high. Goods falling to the ground and getting ruined is an acceptable risk.

The same is not acceptable for humans.

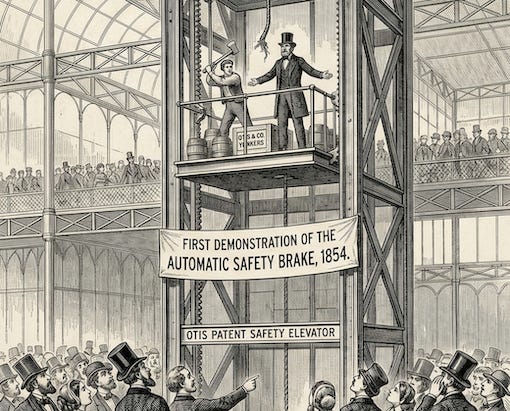

In 1954, Elisha Otis arranged for a stunt. He got into an elevator that went up a few floors. He then cut the rope. The elevator fell only a few inches before the safety brake kicked in.

This stunt left the audience absolutely stunned.

He repeated the stunt several times over the following months.

The demo finally changed the public perception of the elevator. Their use for transporting people finally became acceptable.

When buildings are built, the shaft is custom-made for the elevator in use. So once an elevator is installed, changing the elevator is hard.

Additionally, elevators require mandatory inspections and servicing by law.

Otis got an early head start because of their safety brake.

Since potential buyers loved the safety it offered, more buyers bought it. To help service these lifts easily, Otis was quick to expand their service network.

This had a reinforcing effect.

Many new buyers bought Otis lifts simply because their service network was better.

More lifts sold. More service centers opened. Therefore, increased ease of servicing. Therefore, more new customers prefer Otis lifts.

They just continued to grow big faster than all others — helped because they were the biggest already.

And thus, today, we don’t think twice before boarding an elevator.

Big Becomes Bigger

This effect is called the Matthew Effect.

The big continues to grow bigger. The winner keeps winning.

There’s an investment philosophy centered around this very idea. It’s called momentum investing.

The idea is as simple as it sounds. Stocks that have been going up will keep going up.

Obviously stocks do not keep going up all the time. So, the strategy involves switching. You buy stocks that are going up and sell the ones that have slowed or have started going down.

But how is the Otis case any different from regular investing? Isn’t that literally what investing is all about?

You analyse companies and the business behind them. You try to get an idea for how the future looks. And based on that future, you buy shares to gain from its good future.

That’s just plain investing.

Top 40 Charts

Globally, many radio programs and playlists have top songs’ lists.

It’ll be something like ‘Top 10 Best Songs of the Year’ or month or some version of that.

Many observed that once a song made it into the list, it tended to get more popular. And the more popular it got, the longer it stayed on the charts.

Similar to Otis’ success?

As in, were these songs staying in the charts because they were that good? Or were they simply there because being on such a list ensures greater visibility.

That would mean that a song is becoming more popular not because it is actually good.

It would mean the song is on the charts simply because more people are able to listen to it more often.

A few researchers from Columbia University decided to answer this question.

They created a website called MusicLab where songs could be downloaded from. They had about 14,000 listeners.

They divided this group in two parts.

One group could only listen to songs and vote which songs they liked. The list of top songs were made based on listeners’ listening habits. But the list of top songs was never shown publicly.

The other group could see the list of top songs. Which means, they could see the songs the others were liking too.

The results were sort of expected.

In the second group, a few songs emerged as the top choices and made massive leads compared to the others.

It appeared that more listeners had started enjoying the songs simply because others were listening to them too.

It wasn’t the songs themselves. It was that they were also liked by others.

Different parties concluded different theories.

But by and large, it was agreed that a song enters the charts because it is good. Its success is because of it being good, not popular.

But once a song has entered and climbed higher on the charts, the climb to the absolute top may just be merely because of its popularity.

Momentum Investing

Momentum investing sort of tries to take advantage of this.

It isn’t just about catching a good business early on. It is also about profiting from the hype around it.

Value investing is about buying stocks that are undervalued and sticking with them as they climb and succeed.

If a stock should cost ~Rs 300, they want to pay ~Rs 250 for it. And then they would hope the price rises from there. They would not want to pay ~Rs 350 for it (at that point in time).

Value investors dislike paying a high price. They are not comfortable buying overvalued stocks.

Momentum investors are more comfortable with overvalued prices — if they think the prices will go up even more, often because they feel the market hasn’t fully priced in the company’s growth yet.

If they feel the stock price will reach Rs 400 soon, they’d rather pay Rs 350 rather than wait for the price to fall before Rs 300.

Momentum Strategies

Great, so the idea behind momentum investing as a concept is somewhat understood. But how does it look in actual investing?

It starts with a simple strategy. And gets more and more complex. The specific strategy being used would depend on what the investor feels is right.

Many advanced investors (and traders) develop their own way of using this strategy which can be extremely complicated and even proprietary.

Simplest:

The simplest would be time series momentum.

Invest in Nifty 50 if it has been up over the last 12 months. Sell if it is negative over the last 12 months.

Individual investors might have different versions of this.

Next level:

Another strategy is to use the strongest in a group. This is called relative momentum.

So take a group (could be an index, or a sector). Then define the top in that. Top 3 pharma stocks. Top 10 Nifty 50 companies. So on.

Invest on only those. Sell the ones that exit the top criteria and buy the new top criteria.

Another level higher:

Combine the two. Buy only if the group (sector, index, etc) is moving up. And then choose only the top from that group.

Further:

A more complicated version would depend on a moving average instead of using an absolute price point. So instead of defining a criteria like “has the index moved up in the 12 months”, the investor would craft a condition based on the moving average of that index or sector.

Further:

Sector based. The investor defines a particular number of sectors. Say, top 3 sectors.

Then, among all sectors available, he/she invests in only the top 3 best performing sectors.

Similarly more conditions may be added to this.

More complicated strategies would involve going in greater depth. So, instead of price, they would use conditions like revenue, earnings, earnings growth, etc to decide when to buy/sell.

We can go on and on. The strategies are endless.

When It Works; When It Doesn’t

Well, momentum sounds perfect.

Why are more folks not talking about it?

They are, sort of. But yes, not enough folks.

And there’s a good reason behind it.

Momentum as a strategy works well during certain seasons in the markets. And it tends to perform poorly in others.

In 2000, the legendary Warren Buffett was addressing Berkshire Hathaway’s shareholders through the annual letter.

What he spoke about has now become very popular as the ‘Cinderella Ball’.

He was not talking about momentum investing. He was talking about the dotcom bubble.

But what he described perfectly explains a situation when momentum strategy fails often.

He talks about the separation between investing and pure speculation. The line between where investing ends and speculation starts is very blurry. There is no clear point where it stops being an investment and becomes only speculation.

Speculation is not about the underlying business or the revenues or profits. It’s about gaining from others’ behaviour.

Warren is famous for preaching not to take part in speculation.

Dotcom stocks or tech stocks had caused the share prices to balloon to astronomical levels. Those share prices were not justifiable given the revenues they were earning.

He says nobody likes to leave a party while it is fun. But nobody wants to stay after the party has ended.

Everyone wants to leave before midnight (when the party ends). But the clock in the room has no hands. So nobody can tell the time.

He is trying to highlight that when a share price goes up due to speculation only, it is a bubble. And nobody knows when the bubble will burst. But it will burst for sure.

This applies to momentum as well.

It works well when things are going up and up.

It performs poorly when there is a reversal.

When a falling market turns around. Or, when a rising market crashes.

Proponents of momentum argue that over a long period of time, despite those reversals, momentum as a strategy has given higher returns over some very long periods of time.

But the volatility — the ups and downs during reversals — is not for the faint of heart.

Hence, if someone does plan to use momentum strategy, nerves of steel are a mandatory requirement.

🔢 Quick Takes

+ India and New Zealand have signed a Free Trade Agreement to boost trade by reducing tariffs and improving market access.

+ India’s industrial output rose 4.1% year-on-year in March (vs 5.2% in Feb).

+ The RBI issued final norms on asset classification, provisioning, and income recognition for banks, introducing a new Expected Credit Loss (ECL) framework, effective April 2027. The new rules require banks to set aside money in advance for loans that might go bad in the future, instead of waiting for defaults to happen.

+ The United Arab Emirates has announced it will leave OPEC (Organization of the Petroleum Exporting Countries) effective 1 May 2026, which would cause a major shift in oil markets.

+ The US Fed kept the interest rate unchanged in the 3.5% to 3.75% range for the third consecutive time.

+ India’s forex reserves fell by $4.82 billion to Rs 698.49 billion in the week that ended on 24 April.

+ India’s gross GST collections rose 8.7% year-on-year to Rs 2.43 lakh crore in April. Net collections rose 7.3% to Rs 2.11 lakh crore.

+ The commercial LPG prices in India have been raised for the third time since February, with a hike of around Rs 993: as per media sources

The information contained in this Groww Digest is purely for knowledge. This Groww Digest does not contain any recommendations or advice.

Team Groww Digest