Leadership Rotates

Who Leads After a Crash — And Why It Matters

We’ve talked about recoveries before, but let’s zoom in on the most recent one to understand how each segment performed.

One of the strongest recovery rallies in recent history began in March 2020, after the COVID-19 crash. With stimulus packages rolled out across the world, markets bounced back fully by mid-2020 — just months after the steep fall due to the pandemic.

But the recovery wasn’t equal across all segments.

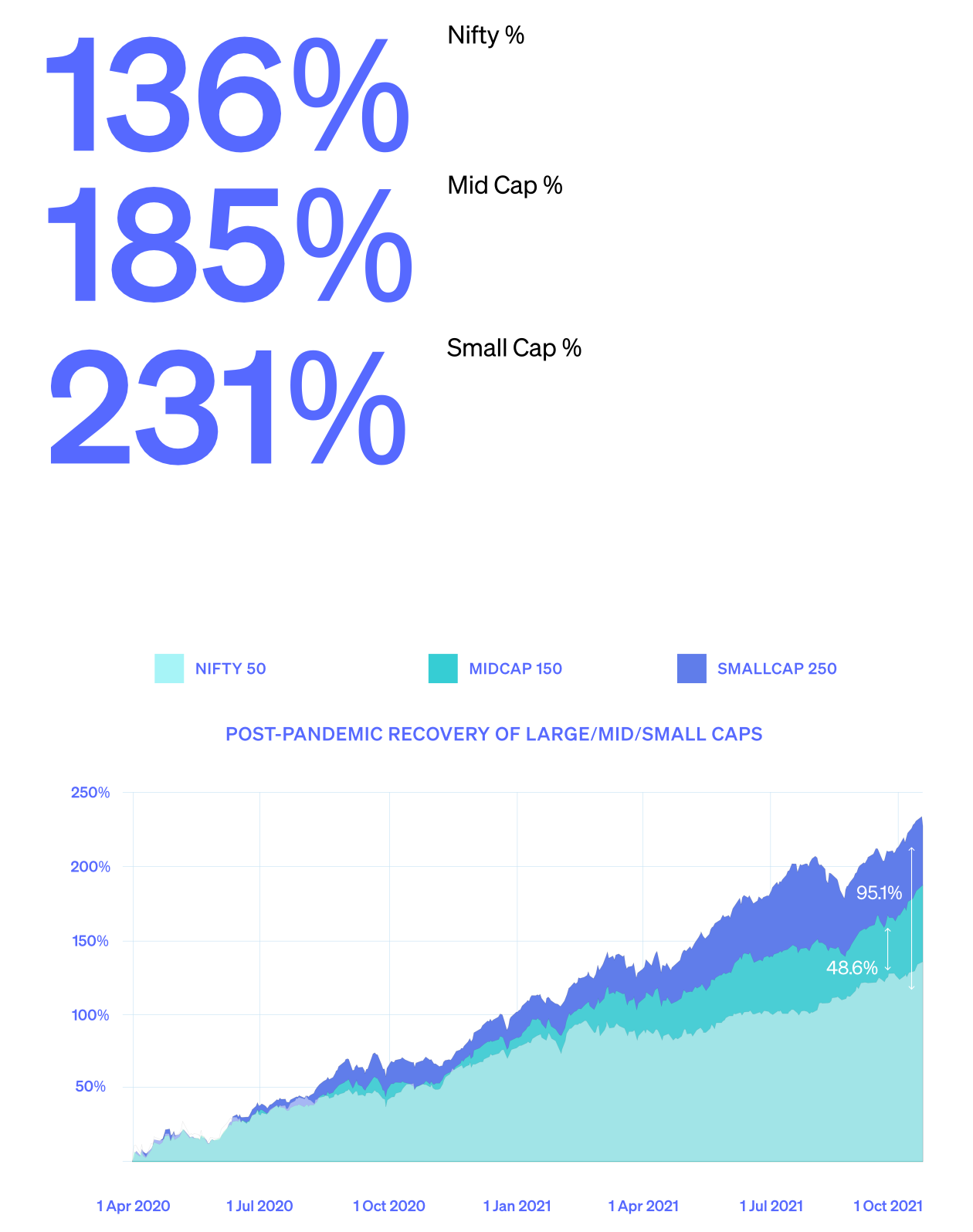

We tracked the performance of three key indices: Nifty 50 (representing large-cap stocks), Nifty Midcap 150, and Nifty Smallcap 250.

When we compared how much each of these segments grew from the bottom of the crash in March 2020 to the end of 2021, we found something interesting.

The chart on the right gives visual proof of a trend we have been discussing so far and the extent to which we see the difference.

Large-cap stocks (Nifty 50) recovered by around 136%.

But mid-cap stocks jumped even more — and small-cap stocks rose the most, rising by 231% over the same period.

This tells us that when the market turns positive, small and mid-cap stocks usually rise a lot more than large-caps.

That’s the tradeoff — they have more growth potential, but also come with more ups and downs.

In fact, this kind of behavior isn’t new. It follows a pattern we talked about in an earlier chapter about during bull markets.

Small and mid-caps tend to lead the rally, because they react faster to positive sentiment.

Once fear of bear markets fade and investors feel optimistic again, these stocks become the center of attention. The reason these segments became optimistic after a crash was because of the stimulus.

After COVID, governments released a huge amount of money into the system to boost the economy.

This flood of money usually finds its way into smaller companies, especially in the small and mid-cap space, which are often B2B businesses. Because these companies are smaller and more sensitive to inflows, they tend to benefit more when money starts moving again.

After a crash, small and mid-cap stocks also become very cheap. As the market recovers, their valuations rise quickly even if earnings haven’t fully caught up.

This is exactly what makes small- and mid-cap stocks so attractive in the early phase of a recovery.

It is important to know that this time there were many new retail investors entering the market as well.

Many of them were first-timers and they were drawn to small and mid-cap stocks because they seem cheaper and have the potential to grow faster. This helped push those stocks even higher.

Basically it shows that market leadership changes with each phase.

In tough times, large-caps protect your money. In good times, small- and mid-caps can grow it faster.

Small-caps typically move first, then mid-caps follow, and sentiment plays an important role in this shift.

But what happens in between?

Because the truth is, not every market phase is dramatic. Sometimes, nothing major happens. There might be just a

long stretch of waiting.

Let us understand that in the next chapter.

“So typically what we have seen in past is small and mid cap companies always have high beta. So when the market crashes, they fall much more than the large caps. But when market recovers, usually we have seen the faster recovery also in them.”

-Mr. Tejas Sheth (Axis AMC, Fund Manager)

Sideways Markets

Investing is not just about highs and lows. It’s about staying put through the boring middle.

So far, we’ve seen that small and mid-cap stocks often steal the spotlight during strong rallies. They bounce back faster, rise more dramatically, and end up delivering higher returns in bull markets.

But what happens when that excitement fades?

What if the market isn’t rising sharply… but also isn’t crashing?

We saw earlier that small-caps show strength in some phases. But it’s important to remember — those sharp swings usually last for a short time. In reality, most of the time, markets are not in an extreme state of euphoria or panic. They’re somewhere in between.

So it is important to study this as well.

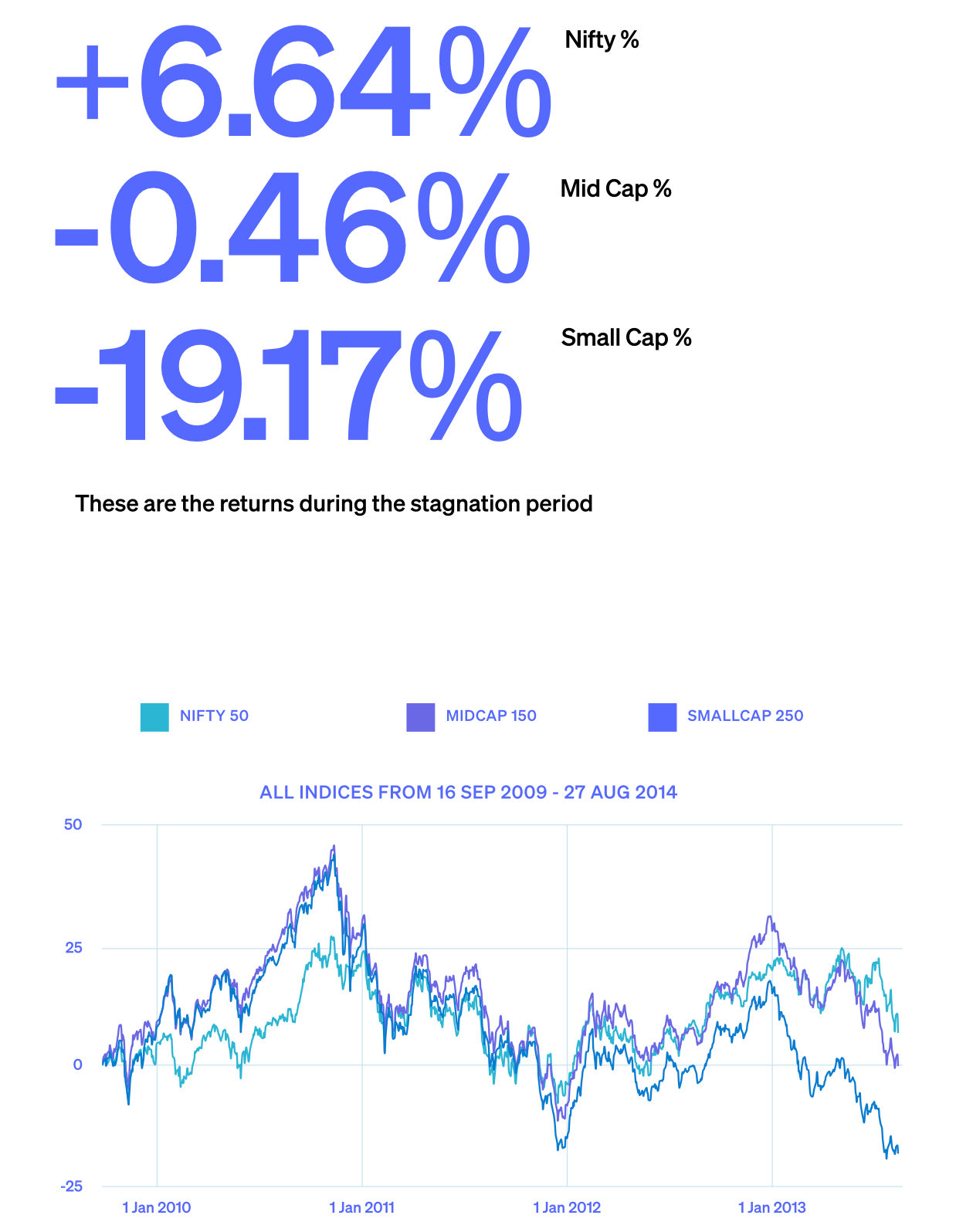

There are two periods that help us understand this phase better—when mid-cap stocks remained largely flat for years.

The first one was from September 2009 to August 2014

The second was from early 2017 to early 2020

In both cases, we wanted to see: what happens when small and mid-cap stocks stop performing?

After a solid recovery from the 2008 crash, mid-cap and small-cap stocks peaked in late 2010 and then, for the next several years, these segments went almost nowhere.

They entered what’s called a consolidation phase — basically, moving ahead with no meaningful growth.

Small-cap stocks actually went negative during this time — falling over 19%. Mid-caps held steady, near zero returns. But, large-cap stocks (Nifty 50) rose around 6.6% over the same period.

Which might not seem like a big deal, but look at it in comparison to how other segments performed, and it stands out. It wasn’t a big growth, but it was steady progress, while other segments of the market stayed stuck or declined.

The same pattern showed up between 2017 and early 2020.

The small-cap 250 index fell by nearly 30%. Mid-caps dropped around 4.5%. And yet, during that same time, the Nifty 50 managed to gain around 20%.

These cases show us something important:

Large-caps don’t always deliver the highest returns, but they often hold their ground when other segments in the market slow down.

They tend to be more stable, more consistent, and less affected by extreme market swings. Over long periods, that consistency adds up.

So while small and mid-caps may be thrilling in good times, large-caps often carry the story forward in quieter stretches.

“So typically whenever we see that a peak of the interest rate cycle is where small cap and mid cap have outperformed large cap significantly. So if we see if 2020 to 2024 period in a very high hyperinflation environment and even in high interest rate environment, small caps kind of outperform because they get more opportunity to grow and they get more value for the productivity they generate.”

- Mr. Tejas Sheth (Axis AMC, Fund Manager)

“If you go back in January 2020, 10 year return of mid and small was not way higher than large. Actually I always highlight one point is, at that point in time, 10 year return for gold was similar to the large cap category. So that's where the starting valuations matter.”

- Shreyash Devalkar (Axis AMC, Fund Manager)