Volatility

What Happens Between Entry and Exit

By now, you have probably started noticing something. The returns we saw earlier — especially in small and mid-cap mutual funds — aren’t fixed. They don’t just depend on what fund you chose. They depend on when you invested. And that part can change everything.

Two people, same fund, same amount — completely different outcomes. One might have seen their money grow by 30%. Another would have just reached 5%. A third could’ve even lost money.

Because, volatility.

That’s the word for when markets are moving a lot. But let’s try to really understand what it is.

Volatility just means how much — and how quickly — prices go up and down. If they’re jumping up and down a lot in a short time, it’s called high volatility.

If they’re barely budging with minor variations, that’s low volatility.

Keep in mind that volatility doesn’t tell you how good or bad an investment is. It tells you what the journey felt like.

Volatility tends to show up more when the world around us is uncertain. If there’s an election coming up or a policy change or some global event no one saw coming.

When people don’t know what’s going to happen next, they start reacting to everything. That nervousness is what causes big movements on the charts.

Let’s say a company announces amazing profits beyond expectations. Investors get excited, and the price jumps overnight. But if the government suddenly announces a tax policy that’s going to hurt businesses? The same price might crash the very next morning.

This bumpiness matters because it dictates what we pick based on our style and our personality.

Small-cap and mid-cap funds go through swings sharper.

It’s because of the kind of companies these funds invest in. They’re more closely linked to how the economy is doing, what policies are changing, where interest rates are headed, and what elections might bring.

So when there’s good news, these companies benefit faster. But when there’s bad news, they also get hit harder and faster.

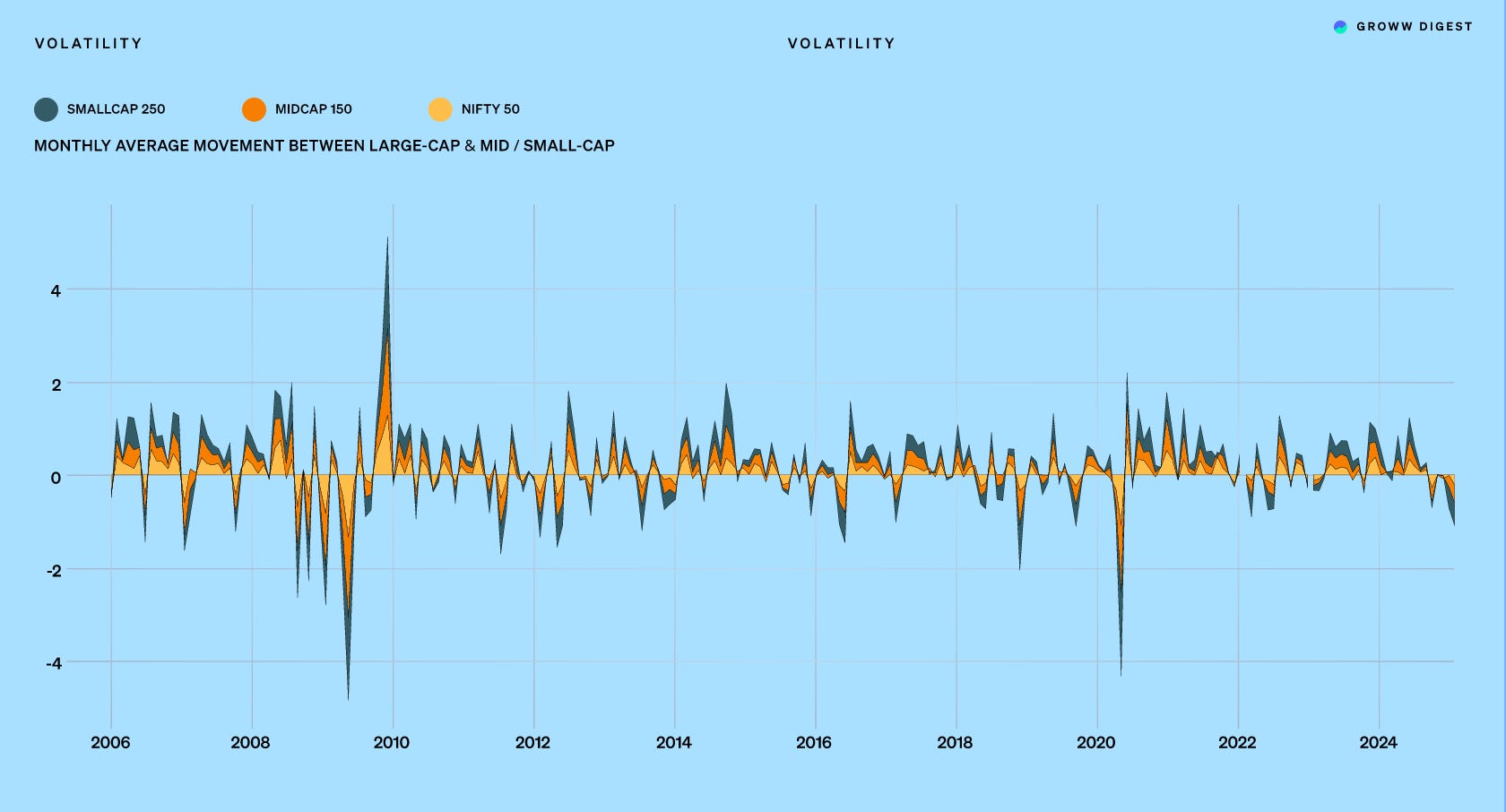

To show you what this actually looks like in data, we plotted the average monthly price movements of 3 indices: large-cap, mid-cap, and small-cap.

We took 20 years of data, because short-term trends can only show a tiny picture.

All three indices — whether it’s the big blue chip companies or the smaller companies — mostly move in the same direction.

If the market is up, they’re all up. If it’s down, they’re all down.

But the difference was in the intensity of those movements. The small-cap index stands out in this respect.

In good months, they spike higher than anyone else. In bad months, they drop further than anyone else.

Mid-caps come somewhere in between. Large-caps, on the other hand, are more stable. Their movements are milder both up and down.

What someone earns at the end isn’t just shaped by the market — it’s shaped by whether they could stay invested through all those ups and downs.

Some of those ups and downs aren't small at all.

They're big market crashes that wipe out years of gains in weeks. But how a fund recovers is even more important than how it falls.

Crash and Recovery

The category you hold decides how you experience a downturn

At this point, one might think, “okay, small-caps are volatile… but can I really handle the ride?”

That’s a fair question. Because so far, we’ve seen how small and mid-cap funds move around more than large-caps. We saw how they can swing higher in good times, and fall harder when things go south. And we also saw how just the timing of your investment can change your returns completely.

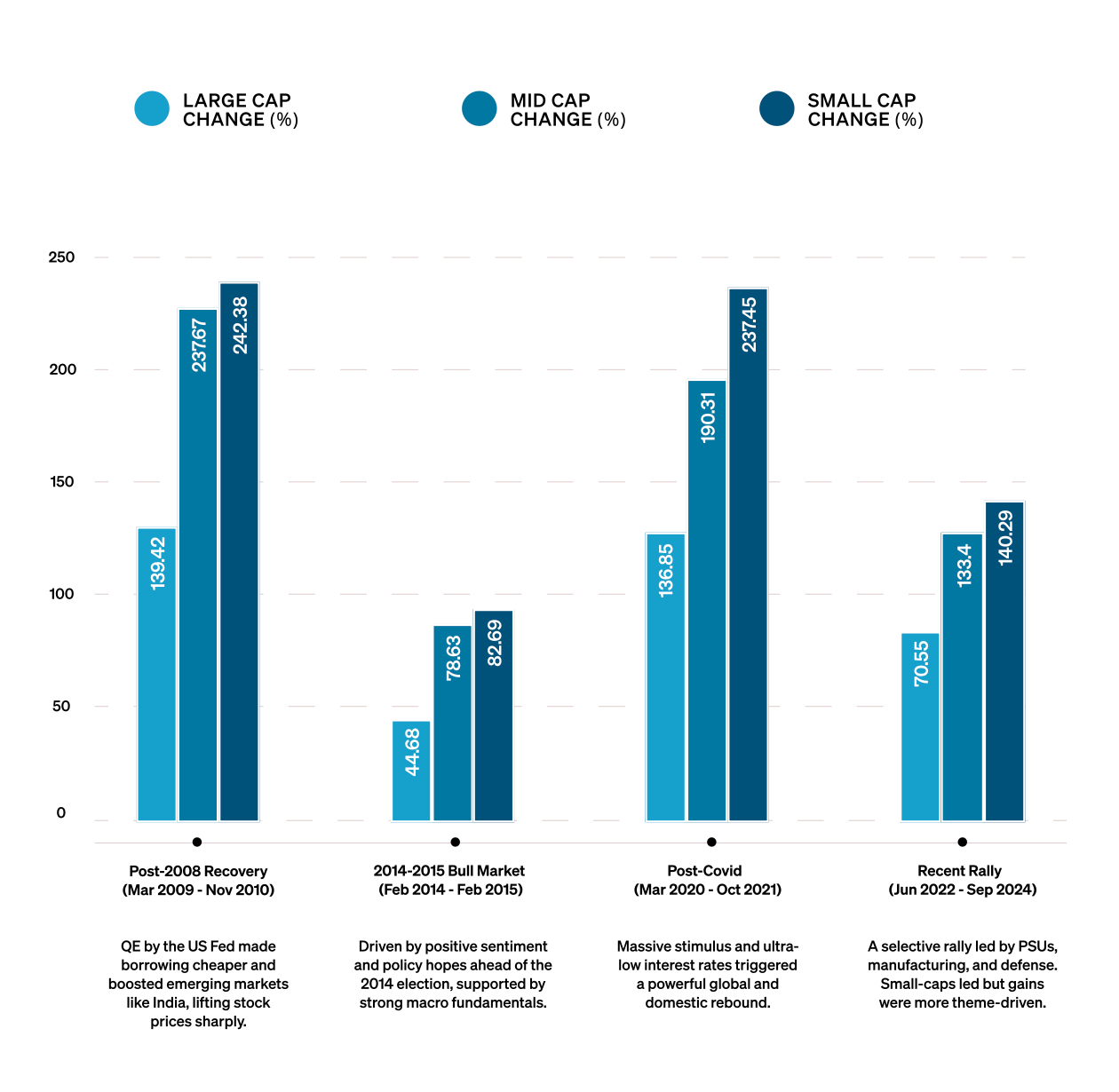

Big market crashes and the recoveries show the actual difference between large-cap, mid-cap, and small-cap funds. Because they don't only fall in different ways, they also bounce back differently.

Let’s start with the falls.

If you look at the chart on the right side of this section, you’ll see how each segment — large-cap, mid-cap, and small-cap — performed during 5 major market crashes.

Starting from the global financial crisis in 2008, and going all the way to the recent decline in 2024-2025.

Most times, large-cap funds fell the least. And every time, small-cap funds fell the most.

The reason for this must have become clear by now. Large-cap companies are big, stable businesses. They’ve been around for longer time. They have more reliable cash flows. Their fall is usually lesser.

Small-cap companies, on the other hand, are usually younger, smaller, and more affected by the ups and downs of the economy. So when fear spreads, they tend to get hit the hardest.

But here’s where it gets interesting.

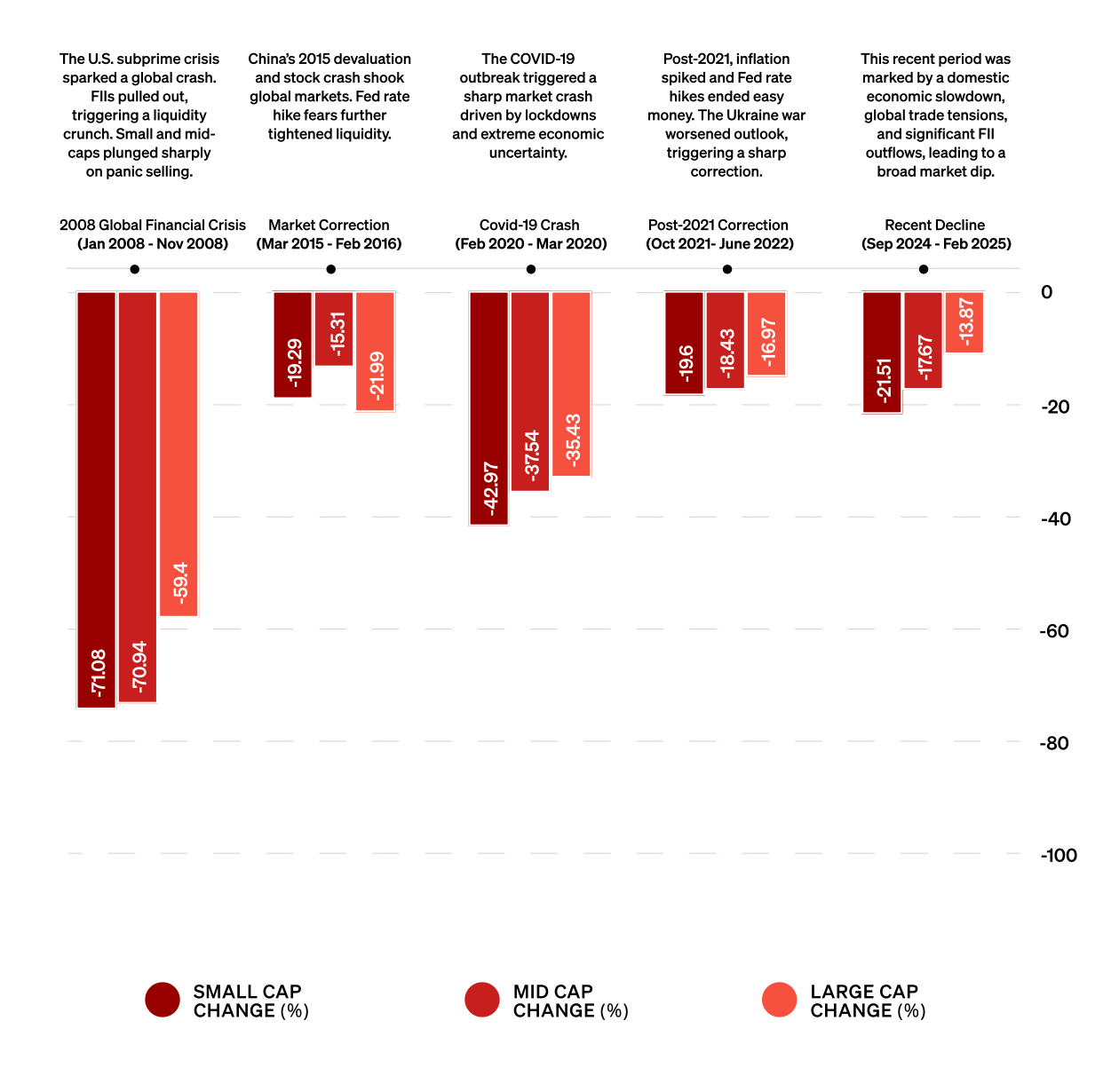

Once the crash is behind us, the whole thing flips.

If you look at the chart below this paragraph, you’ll see what happens during the recovery period after each crash.

Here, small-cap funds lead every market rebound. In almost every case, they bounce back faster and stronger than the others.

Small-caps fall more when the market crashes. But they also rise more when things start to improve. They react faster. They’re more sensitive — both to fear and to opportunity.

Mid-caps fall somewhere in the middle. Not as deep as small-caps, but not as steady as large-caps either. And large-caps recover more slowly, more steadily.

This difference between how much each category falls and how much it recovers shapes how people behave as investors.

Some investors are drawn to this. They want the big comeback. They’re okay with the fall because they’re confident about the recovery and they start pumping in money.

Others prefer something smoother — something with fewer ups and downs. So they stay with large-caps. It depends on investment style, goals, and tolerance for volatility.

And that brings us to the next chapter.